AvigatorPhotographer

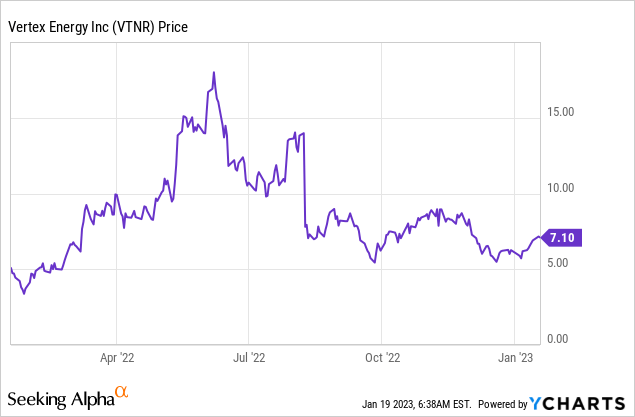

In a few weeks, Vertex Energy (NASDAQ:VTNR) is going to release its Q4’22 results, when the company was finally unhedged and had full market exposure to the high crack spreads. Meanwhile, the renewable diesel project is progressing and is expected to enter into production in Q2’23. At the same time, short-interest is climbing, potentially paving the way for a massive short squeeze if management delivers. Taking a sum-of-the parts valuation approach to Vertex’s business, I estimate that the share price could double in 2023.

Challenging 2022

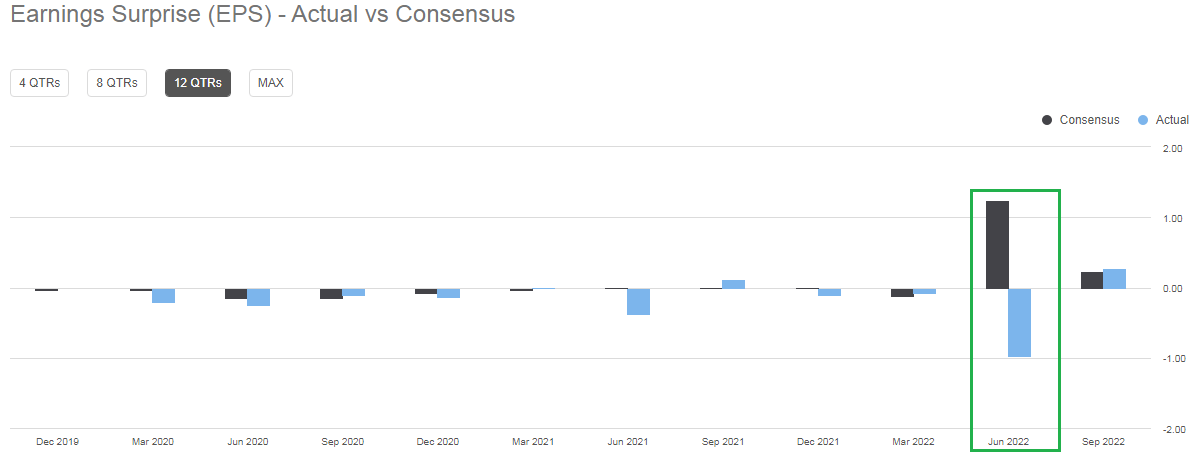

2022 was shaping as a great year for Vertex Energy, following the acquisition of Shell’s (SHEL) Mobile refinery in Alabama. The elevated crack spread environment and the lifted management guidance about 2022 and 2023 have attracted investors and as a result the share price skyrocketed. The consensus amongst analysist was for a very strong Q2’22 with EPS of US$1.24. When the actual results came in, there was a loss of US$0.98/share.

Earnings surprise (Seeking Alpha)

It turned out that Vertex’s management decided to hedge the crack spreads, but completely messed up. Why there was no update of the previously issued very positive guidance, prior to the release of the Q2 results, remains a mystery. In the following two days, the share price cratered 46% and investor’s confidence in management eroded.

Fortunately, the hedges expired on 30 Sept, and Vertex should have enjoyed full exposure to the favorable crack spread environment in Q4’22, with expectations for elevated crack-spread levels to be maintained in 2023. The renewable diesel project is progressing on time and on budget, according to a recent release and is expected to begin operations in Q2’22 with a target production rate of 8-10kboe/day for 2022 with the option of further expansion to 14kboe/day.

Valuation

I’ll approach the valuation of Vertex by valuing each of the three segments – the used motor oil and re-refining business (legacy business), the Mobile refinery and the prospective renewable diesel business.

Legacy business

The used motor oil and re-refining business of Vertex was for sale in 2021 in anticipation of funding needs related to the Mobile refinery, which was being acquired at the time. An agreement was reached with Clean Harbors (CLH), under which Vertex would’ve received US$140M for its used motor oil and re-refining segment. However, later on Verter pulled out of the deal, while the CEO – Ben Cowart has justified the decision by saying that in the changed market environment he didn’t feel that the deal was at the best interest of Vertex’s shareholders, implying that the assets are worth more. But for valuation purposes I’ll stick with the US$140M that were agreed upon.

Mobile refinery

Using the Q4’22 guidance as a starting point, I assume 95% utilization rate of the full 75kboe/day capacity. OPEX is assumed at US$4/barrel as guided, while I estimate G&A at US$40M per year. Also assuming some mean reversion of the 2-1-1 crack spread at US$25/barrel and 52% capture rate. To the resulting EBITDA I applied a x5 multiple which is quite conservative in a normalized environment.

| unit | ||

| Production capacity | kboe/day | 75 |

| utilisation rate | % | 95% |

| effective production | kboe/day | 71.25 |

| 2-1-1 crack spread | US$/barrel | 25 |

| capture rate | % | 52% |

| OPEX/barrel | US$/barrel | 4 |

| Gross profit | US$M | 234 |

| G&A | US$M | 40 |

| EBITDA | US$M | 194 |

| EBITDA multiple | 5 | |

| EV | US$M | 970 |

* Author’s own assumptions

Renewable diesel business

I’ll value the renewable diesel segment using the similar transaction method. In the beginning of 2022, Chevron (CVX) acquired Renewable Energy Group (REGI) – a renewable diesel producer at an EV of US2.75B. According to a release, REGI’s 2021 full year production came at 480M gallons, which translates into 31.3kboe of daily production rate. Taking into account the midpoint of the 8-10kboe/day guidance of Vertex for its renewable diesel project, this equates to about 3.5x less than REGI’s capacity. Using the Chevron’s deal as reference, Vertex’s renewable diesel business should be worth US$785M. But REGI was an established player back then, whereas Vertex is yet to begin renewable diesel production. The market environment is also a bit different as in the beginning of 2022 equity multiples were higher. Because of that and to stay on the conservative side, I’ll apply a 50% to the estimated number and value the renewable diesel business of Vertex at US$392.5M.

Fair value estimate

Before calculating the FV of Vertex, there’s one more issue that it has to be addressed – the convertible bond. Initially it was US$155M in principal with a conversion factor of 169.9235 shares/US$1000 principal. As of Q3’22, a portion of it was already converted and the remaining principal is US$95.2M. Since the conversion price is approximately US$5.89/share, I’ll assume that all of it gets converted. This will increase the share count of Vertex Energy by 16.2M shares to 91.9M. In turn, the company won’t have to repay US$95.2M of debt.

| unit | ||

| Legacy business | US$M | 140 |

| Mobile refinery | US$M | 970 |

| renewable diesel | US$M | 392.5 |

| implied EV | US$M | 1502.5 |

| Net debt, assuming conversion | US$M | 168.5 |

| Equity value | US$M | 1334 |

| share count | M | 91.9 |

| FV/share | US$ | 14.52 |

* Author’s own estimates

The estimated fair value implies 107% upside to the current share price of around US$7.00.

The potential short squeeze and upside triggers

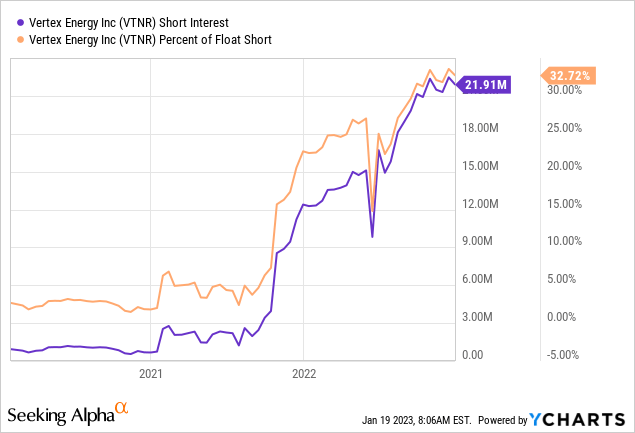

Looking at the short interest in Vertex, it has been climbing. On one hand, the substantial short interest is logical to an extent, given the outstanding convertible bond issue. It’s quite likely that some if not the majority of bondholders decided to hedge their positions and shorted the stock. This theory will also explain the drop in short interest towards the middle of 2022 as some of the bonds were converted. But as of now, there are 21.9M shares shorted, while the whole outstanding bond issue could be hedges with 16.2M shares, so there’s clearly a substantial amount of short interest outside any hedging. This could turn out to be a fuel for a strong upward move if there are positive news about the company. In that regard, I identified two potential upside triggers:

- Strong Q4 results – Free of hedges, Vertex should report very strong Q4’22 results. But given the recent unpleasant and unexpected surprise in Q2’22, some investors likely will want to see the Q4’22 results in the filling, before jumping to conclusions. The report is expected somewhere in March.

- Completion of the renewable diesel project – Successful and timely completion of the renewable diesel project is also a major milestone for the company as it will give it one more operating and cash flow producing segment. Management has indicated that the completion should be done by the end of March.

- Sale of the legacy business – While management has terminated the previously agreed deal, I think that the legacy business may end up being a distraction, especially after the renewable diesel segment is up and running. So if a lucrative deal could be achieved and the used motor oil and re-refining business is sold, I think that it will be a net positive for the company.

Risks

The main risk for a refinery naturally would be a decline in crack spreads. However, as oil refining is considered a “dirty” business and the political environment is quite hostile towards refiners, the last high capacity refinery was built in 1977, while only a few smaller ones were built in the 21st century. Because of that, the refining capacity in the US is pretty much flat. At the same time, people are still using diesel and gasoline as mass EV adoption looks far away.

On the other hand, a repeat of the management’s failure in Q2’22 is a company specific risk for Vertex. Here only increase in transparency and delivering on the guidance could help restore investors’ confidence.

Conclusion

After a challenging 2022 and management’s hedging disaster, Vertex Energy is about to demonstrate the capabilities of the Mobile refinery when exposed to the elevated crack spread market environment. The renewable diesel project is also progressing as indicated. By employing sum-of-the-parts valuation I estimate the FV of Vertex at US$14.52/share – more than double the current share price. The high short-interest on the stock may end up squeezed if management delivers in 2023.

Be the first to comment