David Ramos

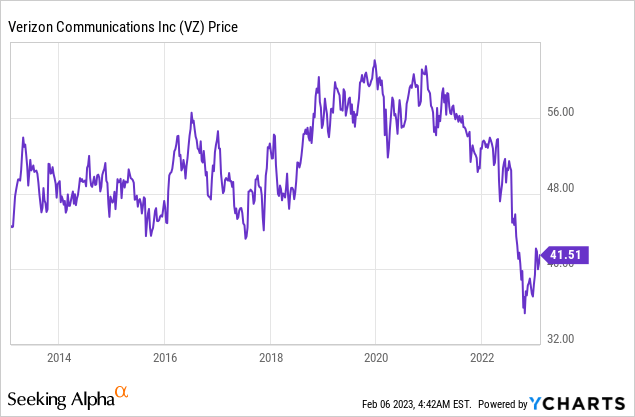

Investor sentiment around Verizon (NYSE:VZ) is near record low levels as the company’s share price hit rock bottom in 2022 and now trades near its 10-year lows.

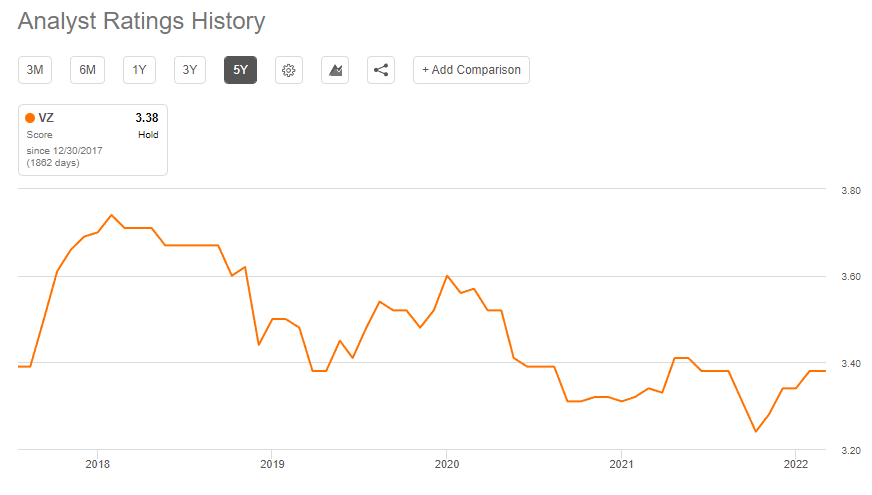

The company was shunned by retail investors, Wall Street Analysts (see below) and perhaps most importantly, by one of its largest shareholders up until recently – Berkshire Hathaway (BRK.B) (BRK.A).

Seeking Alpha

Although analysts’ ratings are rarely indicative of long-term success, the full disposal of Verizon stake by The Oracle of Omaha was a big hit on perceptions around the company’s long-term success. It also prompted me go back and reexamine my initial investment thesis.

As a long-term investor myself, I do take into account rapid shifts in positioning by key shareholders, however, I am not blindly following other people’s investment strategies even if this happens to be Warren Buffet. As an example, a few years ago Berkshire Hathaway sold all of its holdings in a company that I was seriously considering of making one of the largest positions in my personal portfolio. Broader investor sentiment around this particular stock was also near record lows, but all that did not prevent me from taking a long position and sticking to it. Fast forward to today, and this company is now among the best-performers within my personal portfolio and The Roundabout Investor Portfolio, which my subscribers have access to.

What Is Currently Priced In?

In a nutshell, subscriber issues and waning outlook for 2023 were among the major red flags for shareholders over the past year. As Verizon’s competitive positioning became questioned, its share price plunged and the dividend yield is now at its highest levels ever.

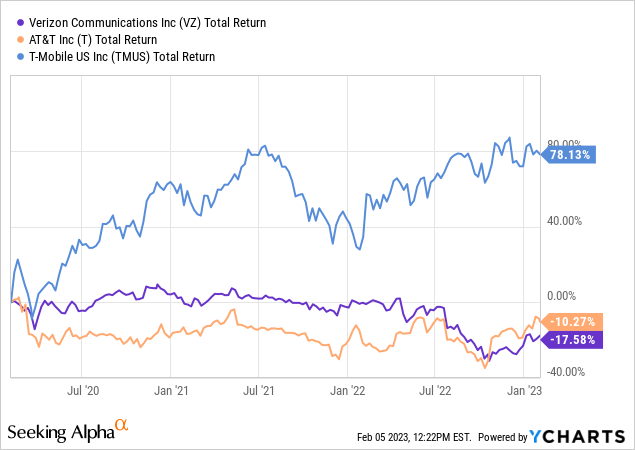

Verizon’s share price performance was even worse than that of the troubled AT&T (T), which has been heavily criticized for major shareholder value destruction through its mega deals for DirecTV and Time Warner. In the meantime, T-Mobile (TMUS) continued to make new highs and widen the performance gap.

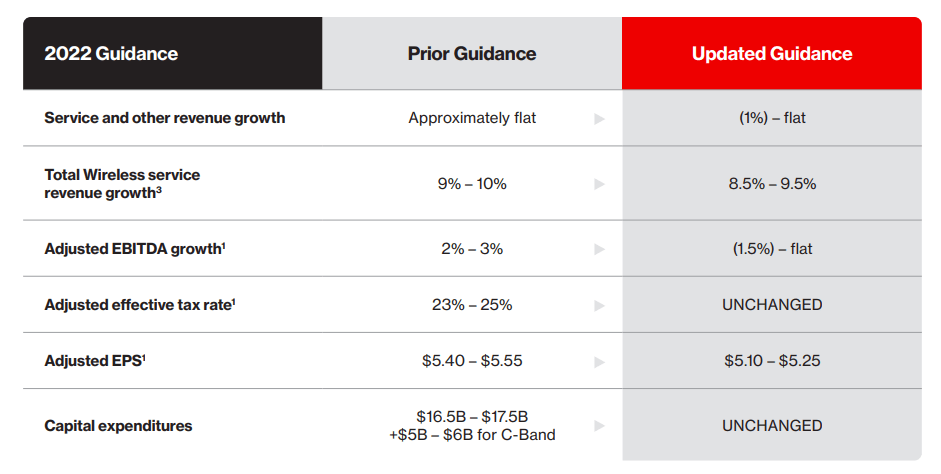

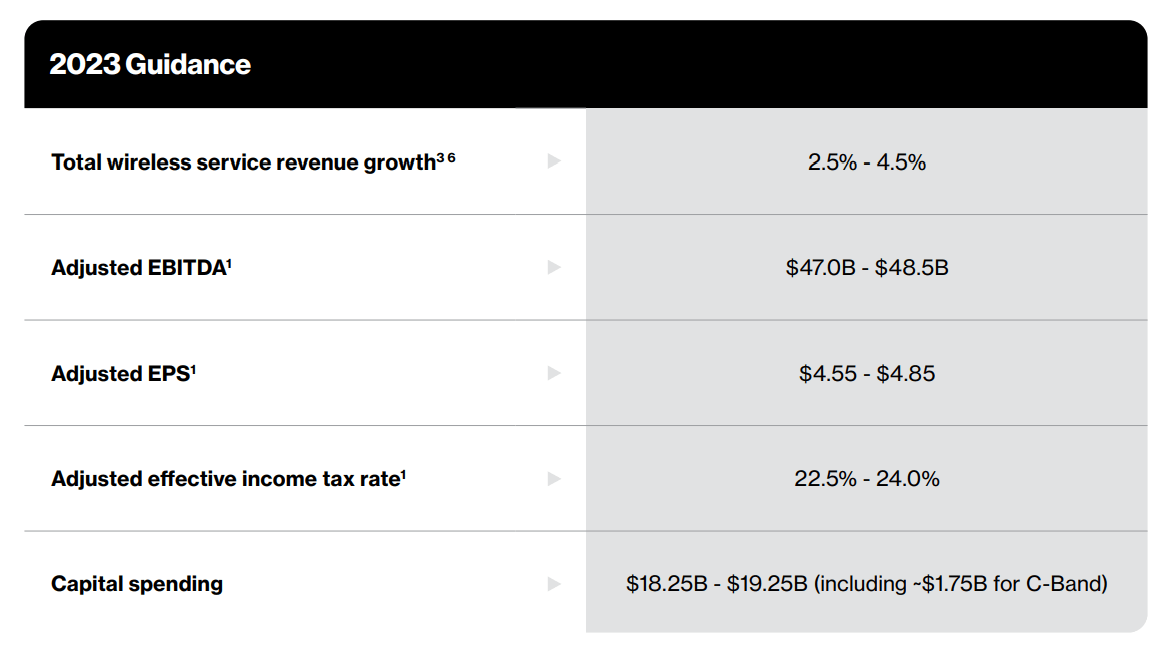

The performance came as a result of reduced guidance for fiscal year 2022 during the same year and much lower revenue growth and total EPS for fiscal year 2023.

Verizon Investor Presentation

With adjusted EBITDA for 2022 standing at $47.9bn, the current range for 2023 points to relatively flat operating profitability over the course of this year. In terms of adjusted Earnings Per Share, however, expectations for this year are much lower than the $5.18 EPS reported for 2022.

Verizon Investor Presentation

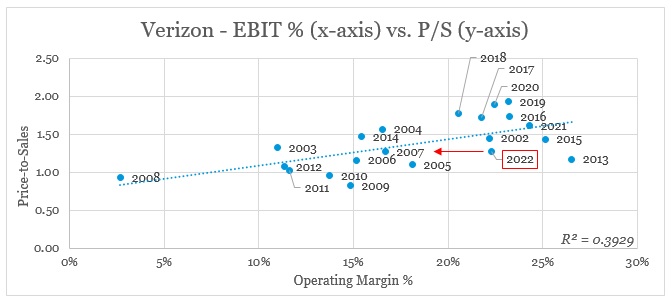

Based on these numbers, Verizon currently trades at 8.6 to 9.1 times its forward earnings, depending on the range provided above.

For comparison, a year earlier on January 25, 2022, when the company reported its Q4 2021 results and provided the initial guidance for fiscal year 2022, Verizon was trading at $52.90 per share or between 9.5 and 9.8 its forward earnings for the same year.

Obviously, there was a significant deterioration not only in the company’s expected earnings, but the market is now pricing Verizon at even lower multiples than before.

While lower expected growth is most often quoted as a major reason for that, profitability is far more important over the long run. In that regard, VZ trades at a significant discount on its current margins and it seems that a large drop in profitability is being priced-in.

prepared by the author, using data from SEC Filings and Seeking Alpha

Is It All That Bad?

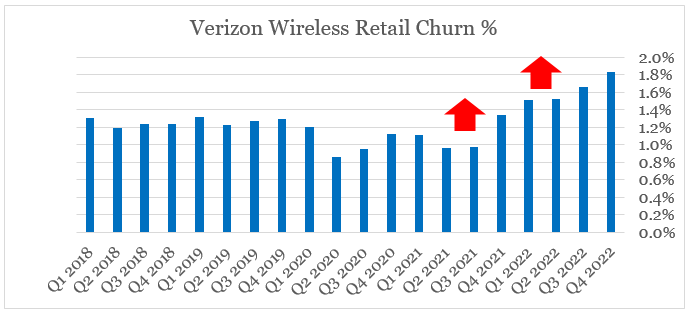

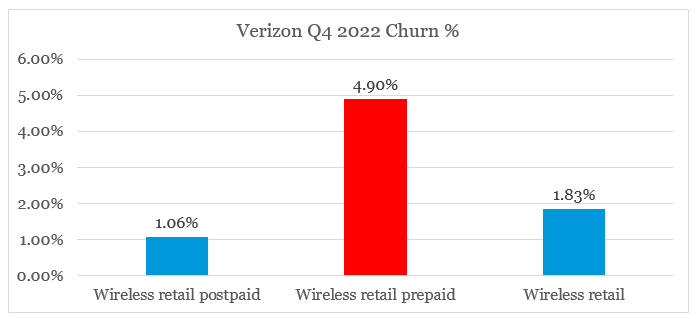

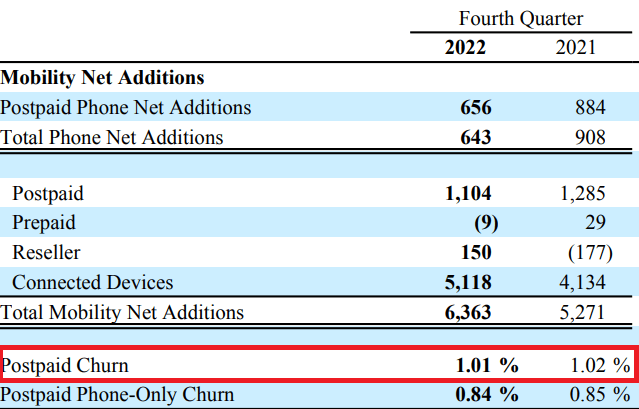

On the surface, it appears that Verizon is bleeding customers at a significantly higher rate than it used to even prior to the pandemic. The reason why I am saying that is because many retail investors and market commentators seem to look at total wireless churn rates and make their conclusions accordingly.

prepared by the author, using data from SEC Filings

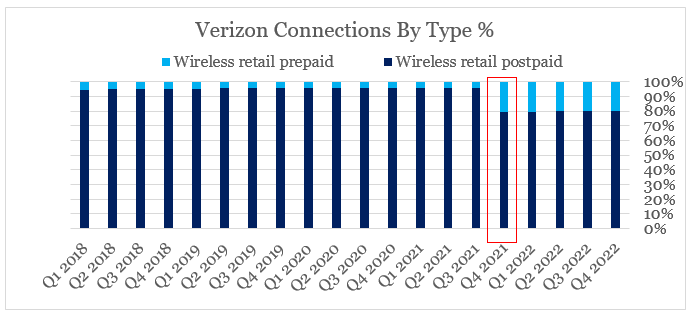

However, during the last quarter of 2021 Verizon integrated its recent acquisition of TracFone, a company with predominantly prepaid customers.

prepared by the author, using data from SEC Filings

Consequently, the share of Verizon’s prepaid connections increased dramatically (see above) and given the prepaid segment’s significantly higher churn rates, the company’s total churn increased to roughly 1.4% in the last quarter of 2021.

prepared by the author, using data from SEC Filings

The $7bn deal for TracFone gave Verizon access to around 20m subscribers or roughly $350 per subscriber, thus positioning the company as a leader in prepaid.

And in November, we completed our strategic acquisition of TracFone, positioning Verizon as the number one provider within the value segment. This opportunity enables us to deepen our relationship with new customers while delivering more enhanced services.

TracFone is being rapidly integrated into our operation. The acquisition added 20 million customers to our prepaid model and cements Verizon as a leading prepaid vendor at Walmart and Best Buy forming a strong foundation of our retail efforts.

Source: Verizon Q4 2021 Earnings Transcript

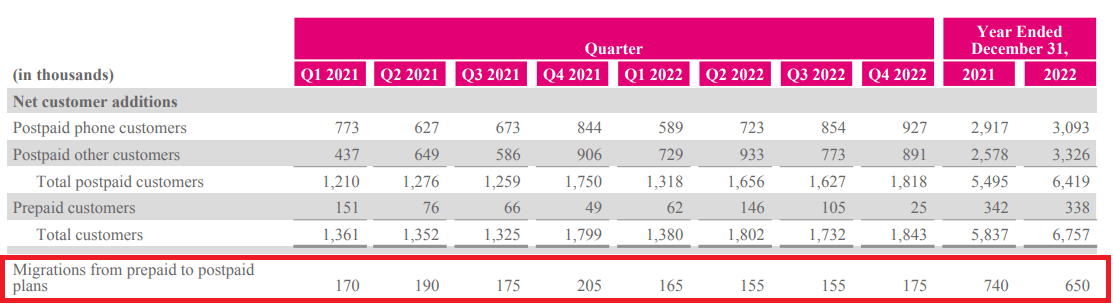

The deal makes sense given the significant synergies due to TracFone being an MVNO relying on Verizon’s network. More importantly, however, there has been a significant migration from prepaid to postpaid in recent years (see the extract from T-Mobile below) and Verizon’s recent investments in its network position it well to capitalize on these trends.

T-Mobile Investor Factbook

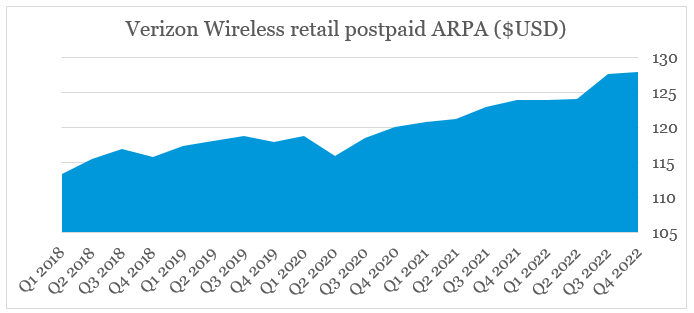

As a result of these investments, average revenue per account (ARPA) in the postpaid segment of Verizon has been steadily increasing in recent years.

prepared by the author, using data from SEC Filings

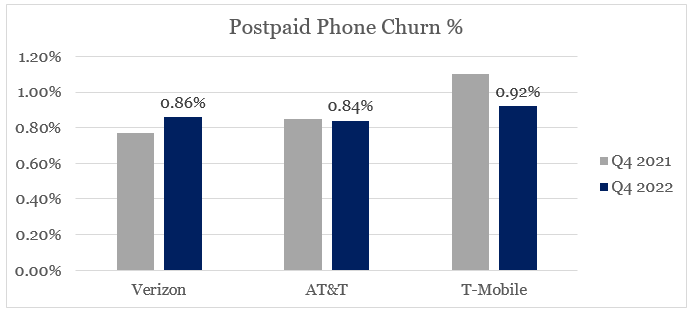

Lastly, Verizon’s churn rate in its postpaid segment is not materially different from that of its major peer – AT&T.

AT&T Earnings Release

The most comparable metric in the postpaid segment that is also reported by all three major peers also does not show any meaningful differences.

prepared by the author, using data from SEC Filings and Earnings Releases

Overall, Verizon does not seem to be in such a bad position relative to peers and as we saw in the previous section, its valuation multiples are already pricing-in a significant deterioration in profitability.

What About Verizon’s Dividend?

Given the size of Verizon and the nature of the industry, investing in the company with the expectations of high growth isn’t a reasonable strategy. The high dividend yield in combination with high return on capital and relatively low risk is the main reason why most people would consider adding VZ to their portfolios.

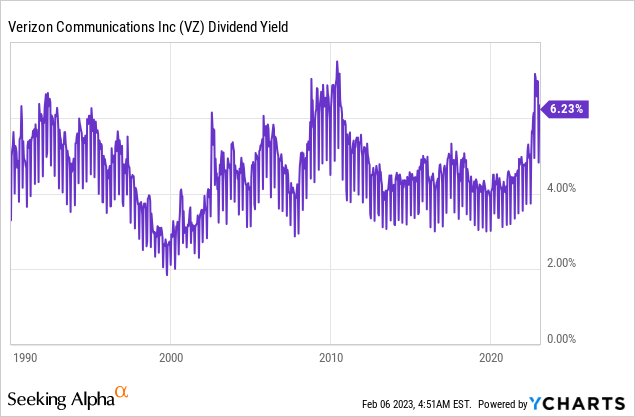

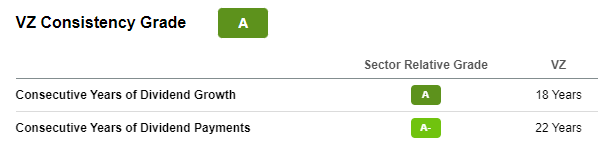

As far as yield is concerned, with a forward dividend yield of 6.3% Verizon is now among the highest yielding stocks within the S&P 500. At the same time, the company has a long-history of consistent dividend growth.

Seeking Alpha

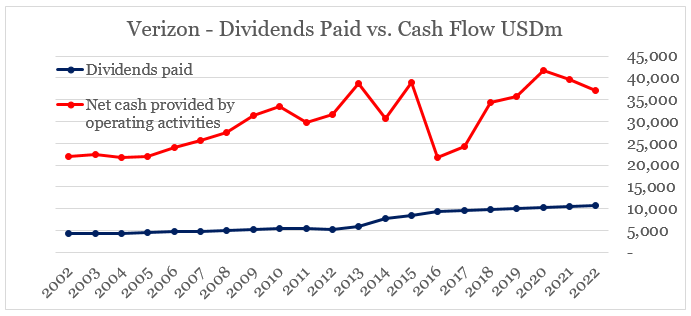

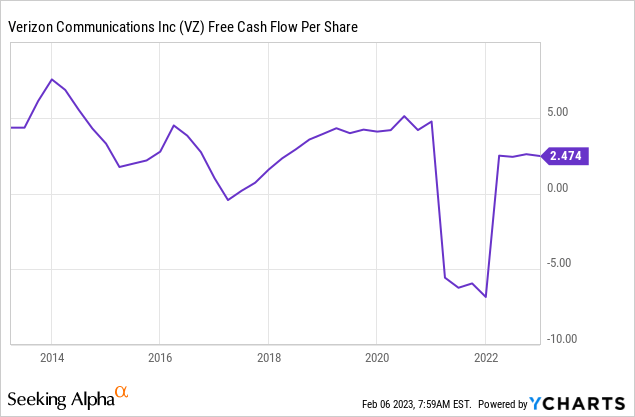

Indeed, recent headwinds and high business reinvestment rates would likely put dividend increases in the near future on hold, however, the dividend remains well-covered from a cash flow point of view.

prepared by the author, using data from SEC Filings

As we saw above, the currently expected EPS for 2023 stands within the range of $4.55 to $4.85, which is nearly twice as much the company’s annual dividend payment per share of $2.61.

Free cash flow per share is slightly lower than the annual dividend paid, however, we should keep in mind that capital expenditure will be drastically lower in the coming years.

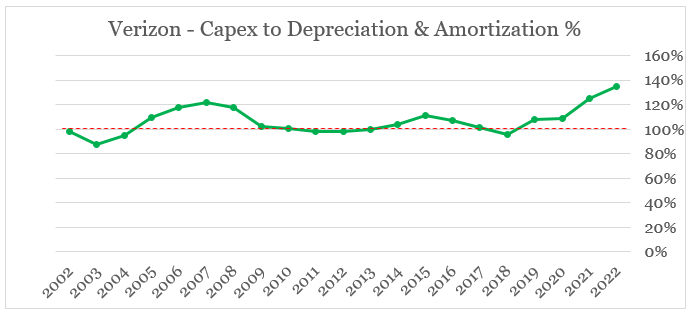

By excluding acquisitions of wireless licenses from Verizon’s Capex, the company has spent a record high amount on capex relative to depreciation and amortization expense in 2022.

prepared by the author, using data from SEC Filings

This number should come down in the coming years as the current investment cycle has already peaked.

(…) we expect our capital spending to reduce significantly in 2023 as we reach the end of our incremental C-band spending, which will be a tailwind for free cash flow.

Source: Verizon Q4 2022 Earnings Transcript

From $23.1bn spent on capex over the course of 2022, Verizon’s management currently expects to spend only $17bn next year or 26% lower.

And as you know, we’re doing all of this as our capital spending budget is expected to decline from $23.1 billion in 2022 to under $19 billion at the midpoint of our guidance range this year, a reduction of nearly 20% year-over-year. In 2024, we expect our CapEx to be around $17 billion, which we expect to represent the lowest capital intensity in over a decade and among the lowest in the industry.

Source: Verizon Q4 2022 Earnings Transcript

Conclusion

Verizon’s share price has been under significant pressure in recent years as operational performance came below initial expectations and the company continued its ambitious reinvestment program. Selling pressure from Berkshire Hathaway and the halo effect of its stake disposal on Verizon share price also contributed to investor sentiment reaching record lows.

Having said that, however, I see no reason to amend my initial investment thesis and I still hold Verizon within my personal portfolio. Moreover, with the share price already pricing-in what is in my view an extremely negative scenario, Verizon has become an attractive dividend play.

Be the first to comment