Instants/iStock via Getty Images

Introduction

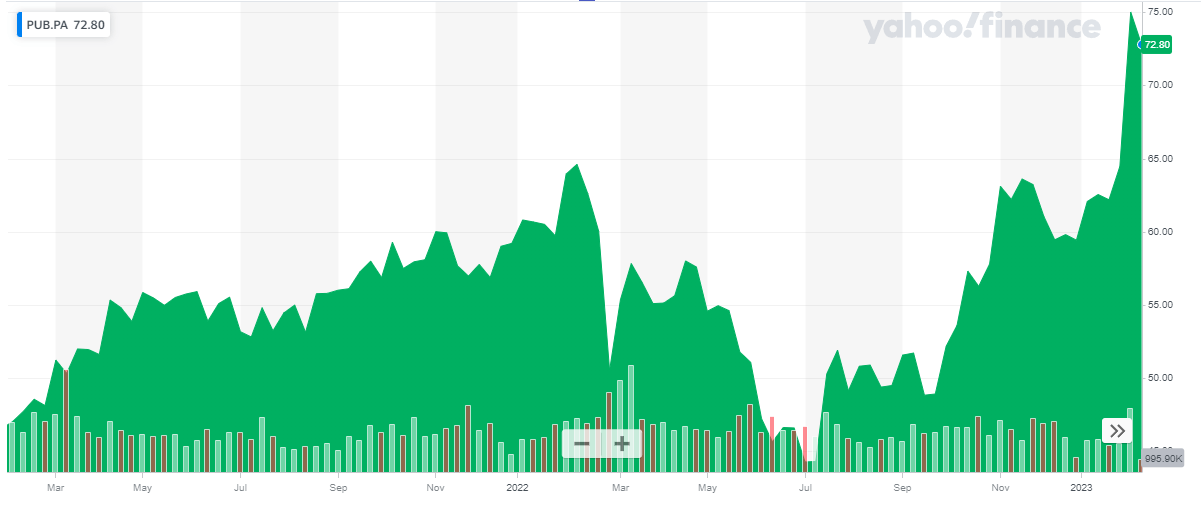

The share price of Publicis (OTCQX:PGPEF) (OTCQX:PUBGY) is finally showing some strength and the stock is now trading about 150% higher than the 28.99 EUR it was trading at when I pounded the table in August 2020. I argued the dividend reduction was just temporary and the underlying operational performance offered by Publicis remained strong. I repeated this bullish view in a July 2022 article. The stock already had almost doubled in the preceding two years, but Publicis still appeared cheap as it was trading with a 12% free cash flow yield.

Yahoo Finance

As a reminder, one share of PUBGY represents 0.25 shares of Publicis. Meanwhile a share of PGPEF represents one underlying share of Publicis. I will discuss the results of Publicis in Euro as the main listing of the company is on Euronext Paris where it’s trading with PUB as its ticker symbol. The average daily volume in Paris exceeds 600,000 shares per day so it makes sense to refer to the primary listing. As of the end of December, the share count increased to 252M shares, resulting in a current market capitalization of approximately 18.3B EUR.

The FY 2022 results are in – and they are even better than I expected

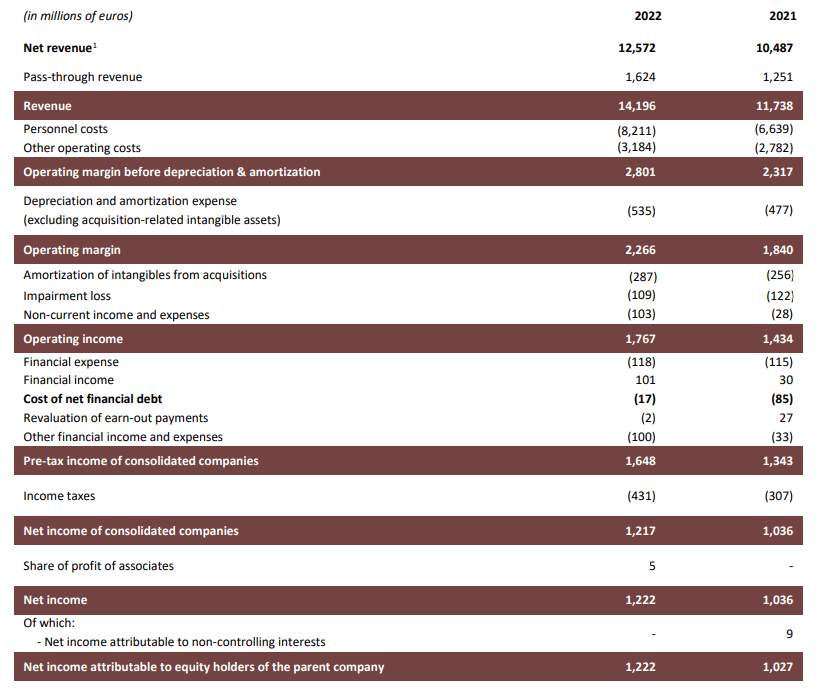

2022 was a great year for Publicis. While it wasn’t very difficult to do better than in 2021 (as there still were COVID issues that had to be dealt with during the year), seeing a total revenue increase of 20% including an organic revenue growth of in excess of 10% is spectacular. Additionally, Publicis’ margins expanded as well. The operating margin increased from 17.5% to 18% resulting in an operating profit of almost 2.3B EUR while the FY 2022 EBITDA came in at 2.8B EUR, a 21% jump compared to the result in 2021.

The total revenue was a pretty impressive 14.2B EUR (and 12.6B EUR excluding the pass-through revenue) and as mentioned before, the EBITDA was approximately 2.8B EUR. As you can see below the operating income was a very respectable 1.77B EUR despite the almost 400M EUR in amortization of intangible assets and impairment losses.

Publicis Investor Relations

The net finance expenses were just 17M EUR as Publicis has rapidly reduced its debt, and the bottom line shows a net income of 1.22B EUR which represents an EPS of 4.87 EUR. While that’s a good result (and a nice increase from the 4.13 EUR per share in FY 2021), keep in mind the bottom line is still heavily impacted by the aforementioned amortization and impairment charges. The sustaining capex is generally substantially lower as these impairments and intangible amortizations are generally related to previous acquisitions whereby Publicis amortizes some of the intangibles on a straight line basis after the acquisition.

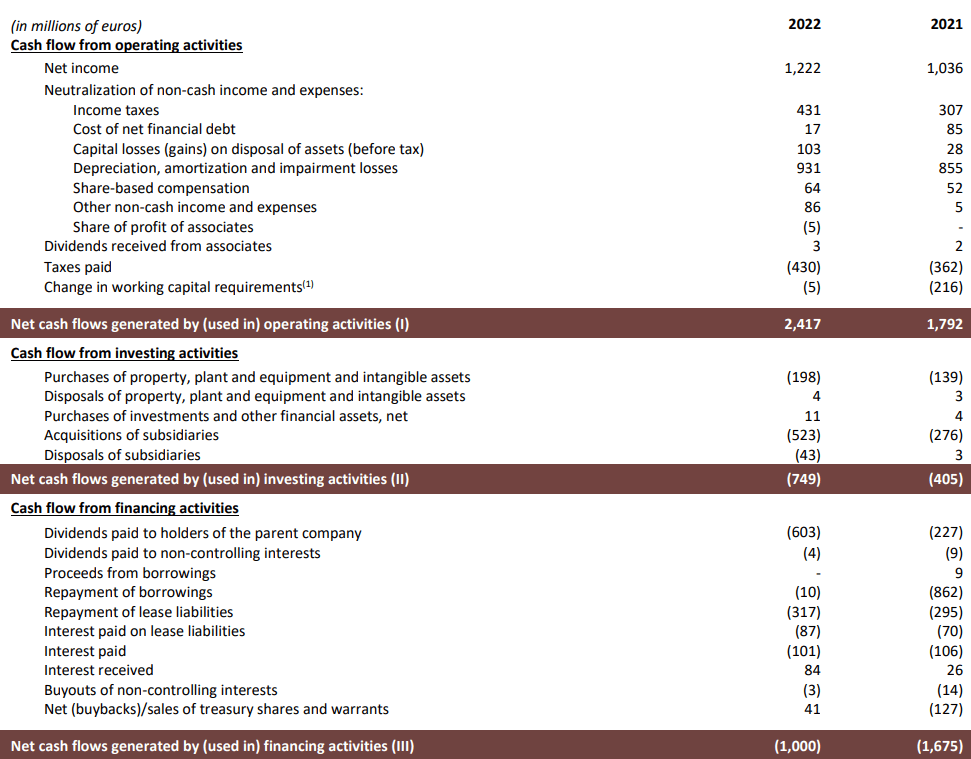

In all my previous articles on Publicis I recommended to look at the cash flow result and that still is the best approach here. While the impairment charges and the amortization of intangibles are weighing on the net income, they are non-cash elements and have no impact on the company’s cash flow performance.

In 2022, Publicis generated about 2.42B EUR in operating cash flow. E still need to deduct the 17M EUR in net interest payments on the financial debt, the 87M EUR in lease interest payments as well as the 317M EUR in lease payments.

Publicis Investor Relations

This means the underlying and adjusted operating cash flow is approximately 2B EUR. We also see the total capex was 198M EUR which indicates the underlying adjusted free cash flow result was approximately 1.8B EUR or 7.14 EUR per share.

Not only is that a massive beat vs. the updated guidance after H1 (Publicis called for a 1.5B EUR free cash flow result), and even better than my expectations. I anticipated Publicis was trading at a 12% FCF yield back in July but it turned out to be in excess of 14%.

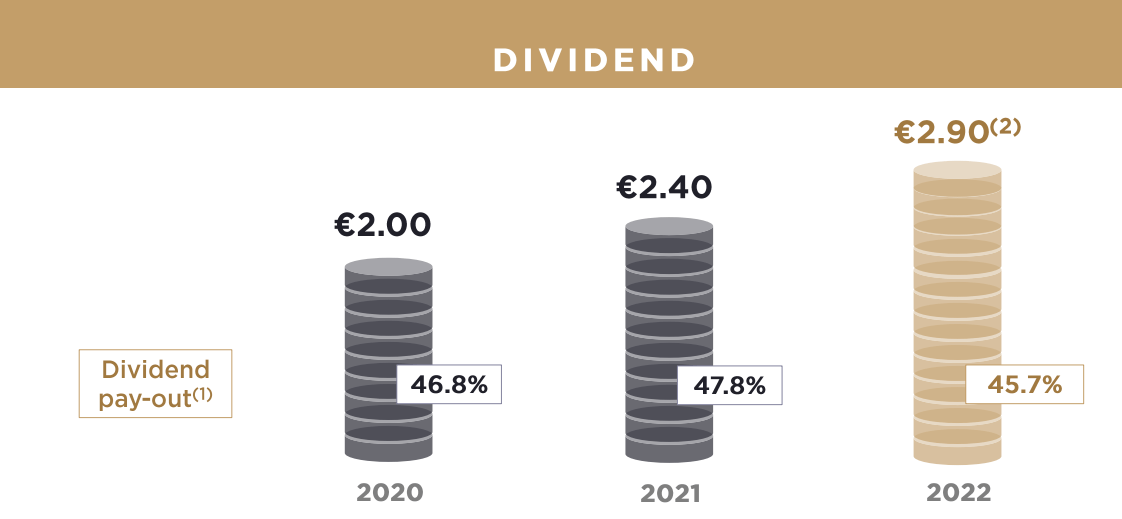

Shareholders will participate in the strong result as Publicis plans to increase the dividend by almost 21% to 2.90 EUR per share. This still represents a payout ratio of just around 40% as Publicis continues to invest in M&A as well.

Publicis Investor Relations

Publicis also sounds upbeat for 2023

While 2022 was a great year, it wasn’t a once in a lifetime performance. Publicis also published its outlook for 2023. The company expects an organic revenue growth of 3%-5% while the operating margin will remain stable between 17.5%-18%.

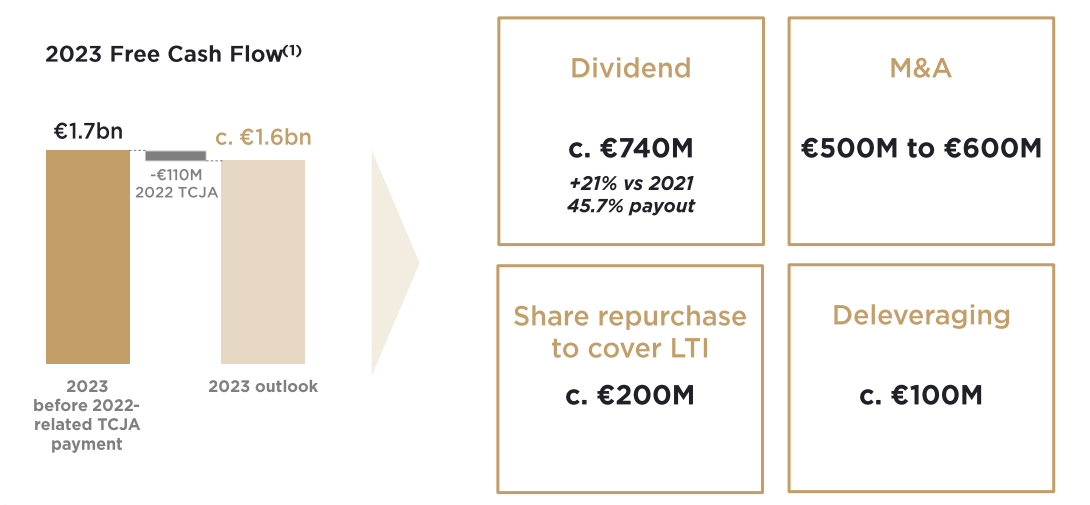

Publicis also mentioned it expects the free cash flow to come in at around 1.6B EUR (just over 6 EUR per share). While this is lower than in 2022 and lower than one would expect from a company guiding for a 3%-5% growth rate, it includes a 200M EUR payment related to the new application of the US Tax Cuts and Jobs Act on R&D capitalization. 110M EUR of that amount was related to FY 2022 but was settled in January. The remaining 90M EUR is based on the 2023 payments and will be paid in installments throughout the year. Excluding these two payments, the underlying free cash flow would be 1.8B EUR, in line with the 2022 performance.

Publicis Investor Relations

Investment thesis

It’s great to see the share price finally move as Publicis has been performing pretty strong with continuously improving results since the outbreak of the COVID-19 pandemic. This seemed to have gone unnoticed at first, but it looks like the market has finally noticed.

While Publicis still isn’t expensive (trading at a normalized FCF yield of approximately 10%), I’m getting a little bit more cautious. I obtained a (relatively small) long position in Publicis after some put options I had written ended up in the money but I sold my shares earlier today. The stock is up over 150% while the 2020 and 2021 dividends added an additional double digit percent return, pushing the total return to almost 200% since the summer of 2020.

I still like the company and wouldn’t mind getting back in at a lower share price, but as the main markets are a bit shaky I wanted to increase my cash position.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment