Torsten Asmus

In 2022, bonds underwent their worst year of performance since the early 1930s (late 1920s at least, in the case of treasuries). Looking all the way back to the Great Depression of nearly 100 years ago, the 24-month accumulated loss of 21.5% in 10-year government bonds that was witnessed in 2021 and 2022 topped the second-worst string of returns by a whopping 15 percentage points.

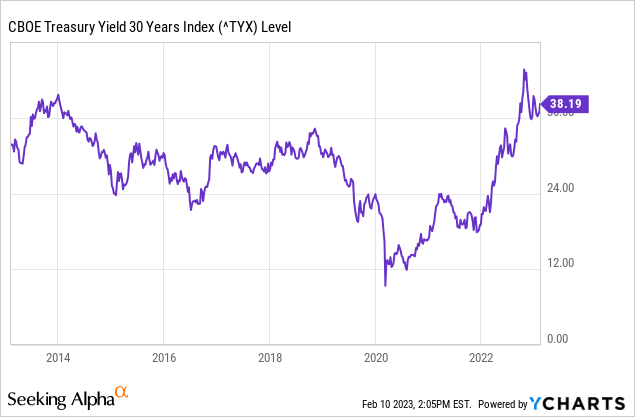

With the 30-year treasury yield now hovering close to 4% (see chart below), near a 10-year high, and well off the sub-1% all-time low of March 2020, I believe that bonds are a great buy-the-dip opportunity. This is true not only for income-seeking investors, who are the typical buyers of these instruments but also for:

- Diversified investors: Balancing the more aggressive parts of a portfolio with defensive holdings has historically produced better risk-adjusted returns. The Sharpe ratio of a monthly-rebalanced, 50/50 stocks-and-bonds portfolio over the past 40 years or so has been 0.64, better than the S&P 500’s 0.52.

- Speculators: There is a reasonable case to be made for recession risks building up in 2023. Last month, EPB Macro Research’s Eric Basmajian reminded readers that the leading economic indicators generally point at a recession in the US that unfolds as early as the first half of this year, made worse by a weakening housing market.

Government-like quality with a boost

While U.S. treasuries and treasury funds are perhaps the most pure-play approach to investing in high-quality fixed income, the Vanguard Long-Term Corporate Bond ETF (NASDAQ:VCLT) has also caught my attention.

This ETF allocates capital to nearly 2,700 different investment-grade bonds issued by some of the best-known corporations in the world, ensuring virtually zero company-specific risk – not to be confused with systematic or market-wide risk, which is low but certainly not negligible in this case. The charts below show the composition of the VCLT portfolio.

Notice how nearly half of the capital is invested in BBB-rated bonds, with the other half allocated across instruments of even higher quality. The exposure to industrials, a traditionally cyclical sector, is very high at nearly 70%. This is not a surprise, however, as mature industrial companies that are capital-intensive tend to be the biggest corporate issuers of debt.

Vanguard

What makes VCLT particularly compelling compared to its sister long-term government bond fund, the Vanguard Long-Term Treasury ETF (VGLT), are the yields. Despite holding instruments of high quality, VCLT’s yield to maturity of 5.6% is a respectable 150 basis points higher than VGLT’s. Today’s high inflation environment makes the percentage and a half in extra expected return (the yield of high-quality fixed income instruments is a good proxy for long-term annual gains) even more interesting.

For the sake of building a balanced portfolio, keep in mind that high-quality corporate bonds have behaved largely as a blend of treasuries and stocks. The chart below shows the performance of VCLT since inception (blue line) against a combination of 90% long-term treasuries and 10% S&P 500 (red line). The very similar annual returns and volatility are evident.

Portfolio Visualizer

Modest income with some upside potential

To be fair, a 5.6% yield that suggests something similar for annual expected returns, in the long run, is not what many would consider exhilarating. But given VCLT’s diversification benefits and the higher risks associated with owning more aggressive, beta-heavy positions in a year of economic deceleration (if not contraction), I like what I see.

Be aware that long-term bonds (VCLT’s average effective maturity and duration are 22.9 and 13 years, respectively) pose the risk and the opportunity of large capital losses and gains, despite the high credit quality. Just think about last year’s decline of 26% in VCLT’s market value to understand that this is far from a low-risk investment. In the current environment, however, I think that the upside potential here far outweighs the probability of another round of sizable losses in 2023.

Be the first to comment