tsingha25

Varonis Systems, Inc. (NASDAQ:VRNS) has shown it can increase revenue on a consistent basis, as well as ARR, but it hasn’t been able to do so at a profit, and as headwinds look to be stronger heading into 2023, it looks like grow momentum could be slowing down over the next year of so.

As a result of economic uncertainty, top management at companies have been prioritizing spend, which has resulted in decreasing closes. Varonis Systems’ federal business has failed to meet expectations in what is usually its strongest quarter, which based upon further degradation of the global economy will likely continue at least into the first half of 2023, and possibly longer if the economy slows down further.

With EMEA already weak and expected to spill over into the U.S. market, interest rates continuing to rise, and the U.S. dollar remains strong. There aren’t any near-term catalysts I can see that will stop Varonis Systems, Inc. from underperforming in the next couple of quarters at least, and possibly longer.

In this article we’ll look at some of the numbers, ongoing headwinds, and why its Data Security Platform will put downward pressure on earnings in the quarters ahead.

Some of the numbers

Revenue in the third quarter was $123 million, up $23 million from the $100 million in revenue generated in the third period of 2021. Revenue in the first nine months of 2022 was $331 million, up from the $263.5 million in revenue generated in the first nine months of 2021.

Subscription revenues in the third quarter of 2022 came in at $96.1 million, up 37 percent from subscription revenue of $70.4 million in the third quarter of 2021.

Maintenance and services revenue in the reporting period was $27.3 million, down from the $30 million in maintenance and service revenue from the third quarter of 2021.

Investor Presentation

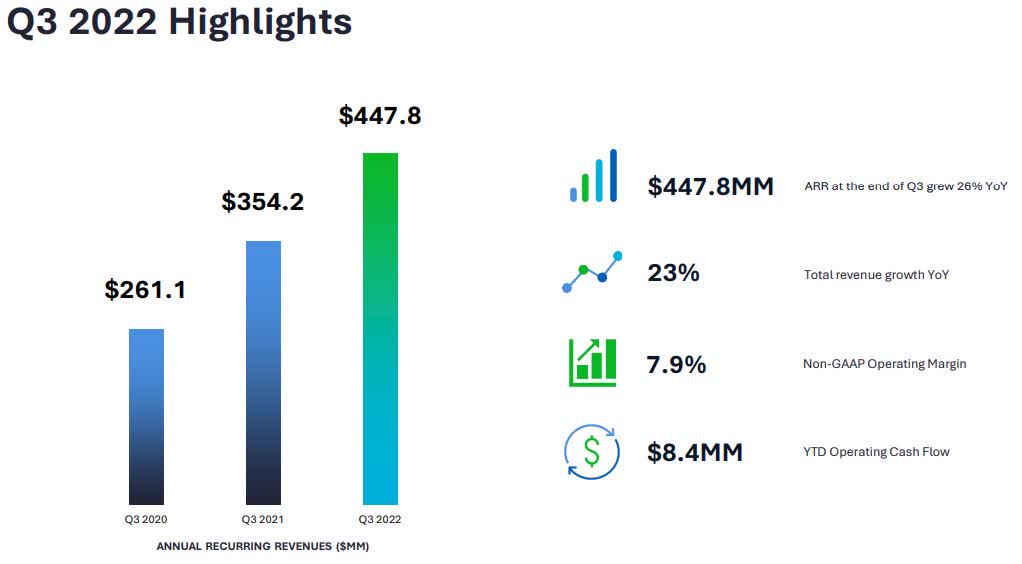

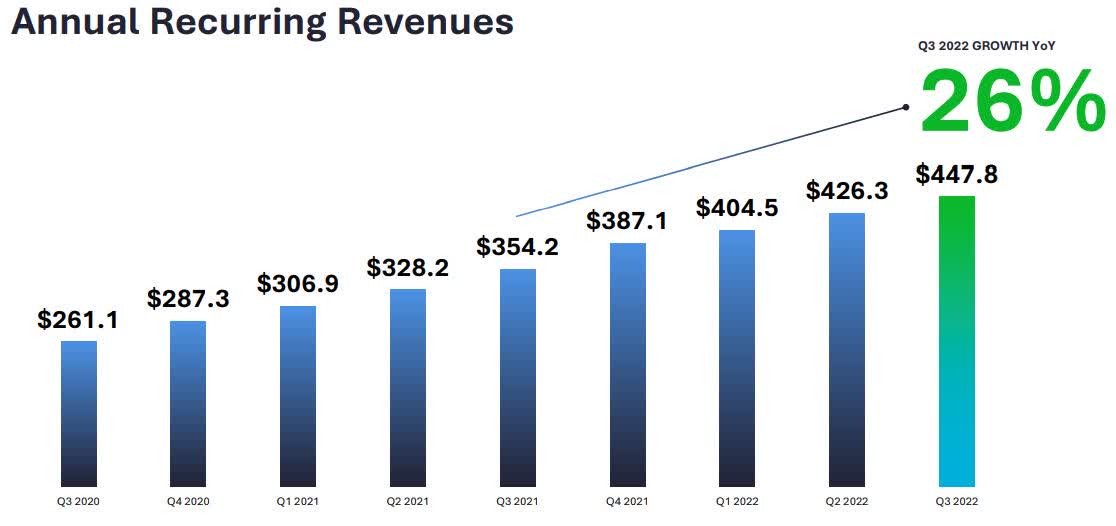

Annual recurring revenues (ARR) were $447.8 million at the end of the third quarter, up 26 percent year-over-year.

TradingView

Operating expenses in the reporting period climbed from $105 million in the third quarter of 2021 to $132 million in the third quarter of 2022. Operating expenses for the first nine months of 2022 were $389 million compared to operating expenses of $302 million in the first nine months of 2021.

Net loss in the third quarter was $28.7 million, or $0.26 per share, compared to a net loss of $23.3 million or $0.22 per share in the third quarter of 2021. Net loss in the first nine months of 2022 was $113.7 million or $1.04 per share, compared to a net loss of $91.8 million or $0.88 per share in the first nine months of 2021.

In response to worsening macro-conditions, management has taken measures to reduce costs, including reducing headcount by 5 percent, from which the company expects to save approximately $7 million in the fourth quarter.

Cash and cash equivalents at the end of the third quarter of 2022 was $754 million, down by approximately $51 million from the end of calendar 2021.

Performance by geography

The North American market continued to do well on revenue growth, ending the third quarter of 2022 at $98 million, up 30 percent year-over-year, and accounting for 79 percent of total revenue.

In its U.S. federal business, close rates fell by about $4 to $5 million below company expectations.

EMEA showed signs of weakness, with revenue dropping to $22.1 million, down 3 percent from the third quarter of 2021 and now accounting for 18 percent of total revenues.

A concern about Europe was even with the FX headwind organic sales failed to meet company expectations, primarily from economic uncertainty causing top management to tighten up on spend. From management commentary, it appears they underestimated the impact of the economic weakness on Europe.

For Rest of World, revenues were $3.2 million, up 63 percent year-over-year, and representing three percent of total revenue.

Probably the biggest concern for the performance of VRNS going forward is going to be what level its North American business will decline if there is a modest spillover from the decline in Europe, as management believes there could be. With that market accounting for almost 80 percent of its total, it would put a lot of downward pressure on the company if EMEA worsens and North America underperforms, even if it is at a modest level.

Data Security Platform

The introduction of its flagship Data Security Platform as a SaaS provided a couple of insights that are important for how investors model the company in the short term.

First, with the company investing over $100 million into developing the platform, it has played a significant role in CapEx, which has resulted in quarter-after-quarter of losses. So the company has a lot of capital, sweat and time invested in the platform, and it’s crucial in my view that it succeeds.

Without doing a deep dive into the platform, what it essentially does is “transform the features of our on-prem subscription offering into SaaS offering.”

Even with the introduction of the new platform the company will continue to sell its DA Cloud products alongside the new platform. It’ll be offered as a premium subscription licenses or as a SaaS.

Management believes the new platform will be a key part of reaching its goal of having $1 billion in more ARR in the future.

As for how the company’s going to roll it out, it says it’ll start with smaller, new customers, and as VRNS gains confidence it’ll eventually offer it to its existing customers.

The downside to rolling it out is, because of upfront costs in particular, it’ll put downward pressure on gross margins and operating margins, which will of course have a negative impact on net income and earnings per share. Taking into consideration the current economic and market environment the company is competing in, it will result in challenging numbers in the quarters ahead, the level to which will depend on how quickly it is adopted by its initial customer base.

On the other hand, if it is successfully transitioned to its larger, current customers, it should be a solid tailwind in the years ahead. Management said it could take from four to six years before it makes a strong impact on the performance of the company.

Conclusion

Over the last couple of years, the share price of VRNS has reached a double top of approximately $73.00 per share and has recently plunged to its 52-week low of $15.61, before bouncing off it to trade at $23.42 as I write.

TradingView

Although it’s tempting to think the bottom is in and the company has found support, I’m not totally convinced that everything is priced in. We know the company downwardly revised some of its near-term guidance, but with cutting its workforce and lowering some expenses, it seems like it’s preparing for things to get worse before they get better. I think that’s how it’s going to play out, not only from economic and geopolitical headwinds, but also as a result of recent organic underperformance.

Combine that with added costs of the rollout of its new Data Security Platform, deteriorating economic conditions in EMEA, and the strong probability North America is going to get at least moderately affected by the global economy in relationship to VRNS, and it’s not a recipe for a good performance heading into 2023.

Over time, data security is going to remain a growing trend, but for now it looks like it’s going to take a breather. As a result, the performance of Varonis Systems, Inc. is going to suffer in the near term.

Varonis Systems, Inc. is a stock I would be cautious with until there is more clarity over the next couple of quarters. On the positive side, for investors that like VRNS stock and believe in the long-term growth trajectory of the sector, it could represent a good entry point if the share price of Varonis Systems, Inc. pulls back further, which it has a good chance of doing.

Be the first to comment