Kevin Dietsch/Getty Images News

Just imagine

The title is a reference to the John Lennon’s Imagine “you can say I’m a dreamer, but I not the only one”. It illustrates wishful thinking, hope and utopia.

So, try to imagine a world where the Fed can deeply invert the yield curve to fight the inflationary shock, without causing a recession. That’s exactly the FOMC forecast for 2023.

Now, try to imagine a “world where people live their lives in peace”.

The Fed’s forecast for 2023

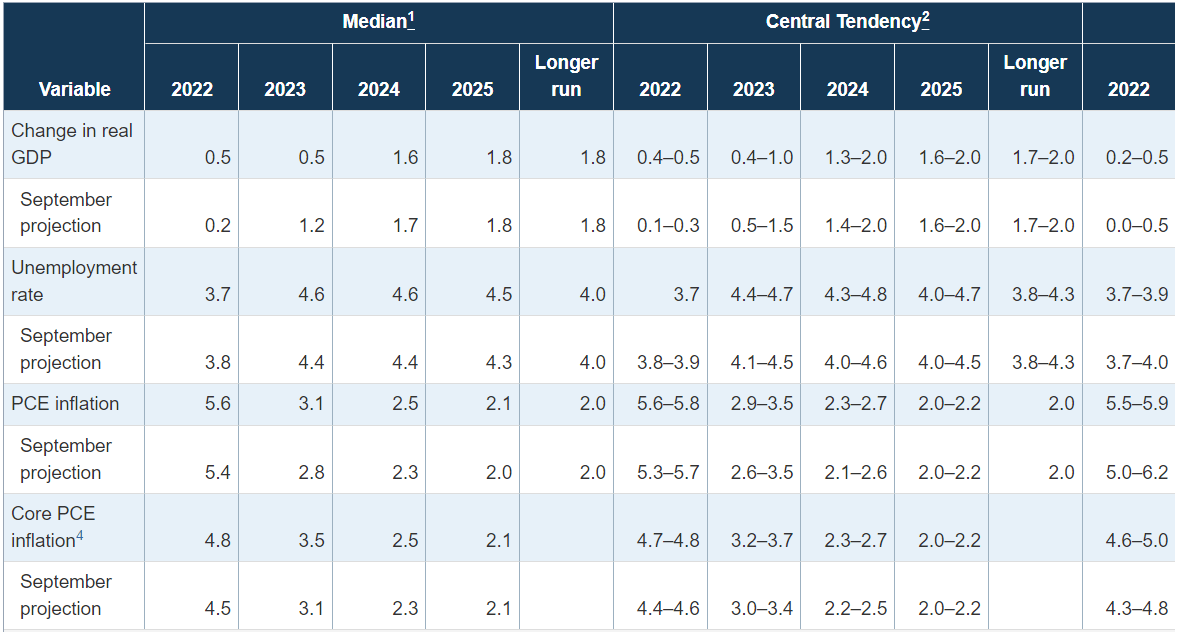

The Fed held the last FOMC meeting for 2023 on Dec 13-14th, and, as previously signaled, increased the Federal Funds rate by 50bpt to 4-1/4 to 4-1/2 percent.

The Fed also released the Summary of Economic Projections for 2023, and beyond, with the projected appropriate policy path.

- The GDP projection: In September of 2023, the Fed projected a very weak GDP growth of 0.2%, and relatively strong rebound in 2023 to 1.2% GDP growth. Now, the Fed projects somewhat higher GDP growth for 2022 at 0.5%, and the same low 0.5% GDP growth for 2023, which is a significant downgrade from the September projections. The GDP growth rebound to 1.6% is pushed to 2024.

- The unemployment rate projection: In September, the Fed projected a 4.4% unemployment rate for 2023 and 2024, an increase from 3.7% in 2022. Now, the Fed projects even higher increase in the unemployment rate to 4.6% for 2023 and 2024.

- The inflation projection: In September, the Fed projected the PCE inflation at 2.8% and core PCE at 3.1% for 2023. Now, the Fed projects even higher inflation for 2023 with the PCE inflation at 3.1% and the core PCE at 3.5%.

- Projected appropriate policy path: In September the Fed projected the Federal Funds rate at 4.6% in 2023, which is just above the current level. Now, the Fed projects even higher Federal Funds rate for 2023 at 5.1%, or another 75bpt from the current level.

So, when compared to its’ September meeting projections, the Fed now projects a significant economic slowdown in 2023, with higher unemployment rate and higher inflation. Here is the Fed’s December 2023 Summary of Economic Projections:

FOMC FOMC

The big picture – the Fed lost its credibility

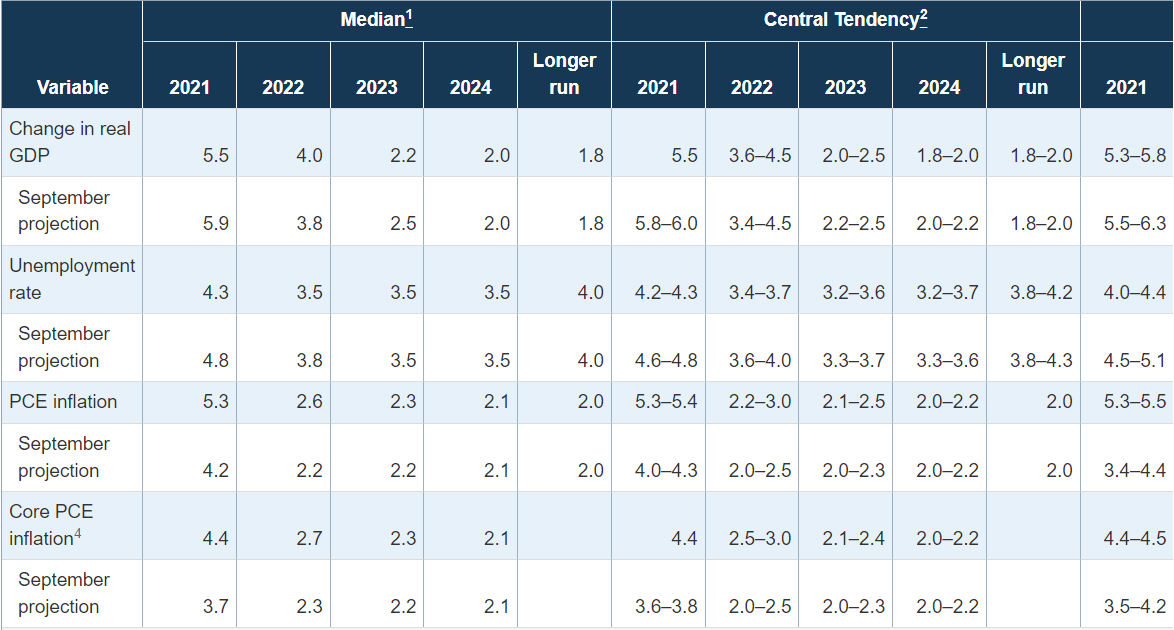

But let’s look at the Fed’s Summary of Economic Projections from December 2021, exactly 12 months ago.

The Fed projected in December 2021 a 4% GDP growth for 2022, with the 2.6% PCE inflation, 2.7 core PCE inflation, and 0.9% Federal Funds rate. As of December 2022, the PCE inflation is 6%, core PCE inflation is 5%, the real GDP is essentially flat for the year, and the Federal Funds rate is at 4.37%. What a miss! Here is the Table with projections for 2022.

FOMC FOMC

Obviously, the Fed made the major error in December 2021 by predicting that the post-covid inflation would be transitory, and that inflation would fall back near the 2% quickly in 2022.

You could try to justify this error as just the timing issue, since the covid-related supply-chain bottlenecks took just a little longer to resolve. Also, the Fed could not had predicted the inflationary pressures due to the Russian invasion of Ukraine.

However, the Fed was well aware of the more persistent inflationary pressures from the workers-jobs gap, given the US aging demographics, the anti-immigration policies, and the logical implication that the soaring stock market, real estate and cryptocurrencies would allow many to retire prematurely.

Yet, the Fed continued with the Quantitative Easing program until March of 2022, pouring more fuel on fire. Given the Fed’s recent errors, why would anybody take their 2023 predictions seriously?

What’s wrong with the Fed’s 2023 projections?

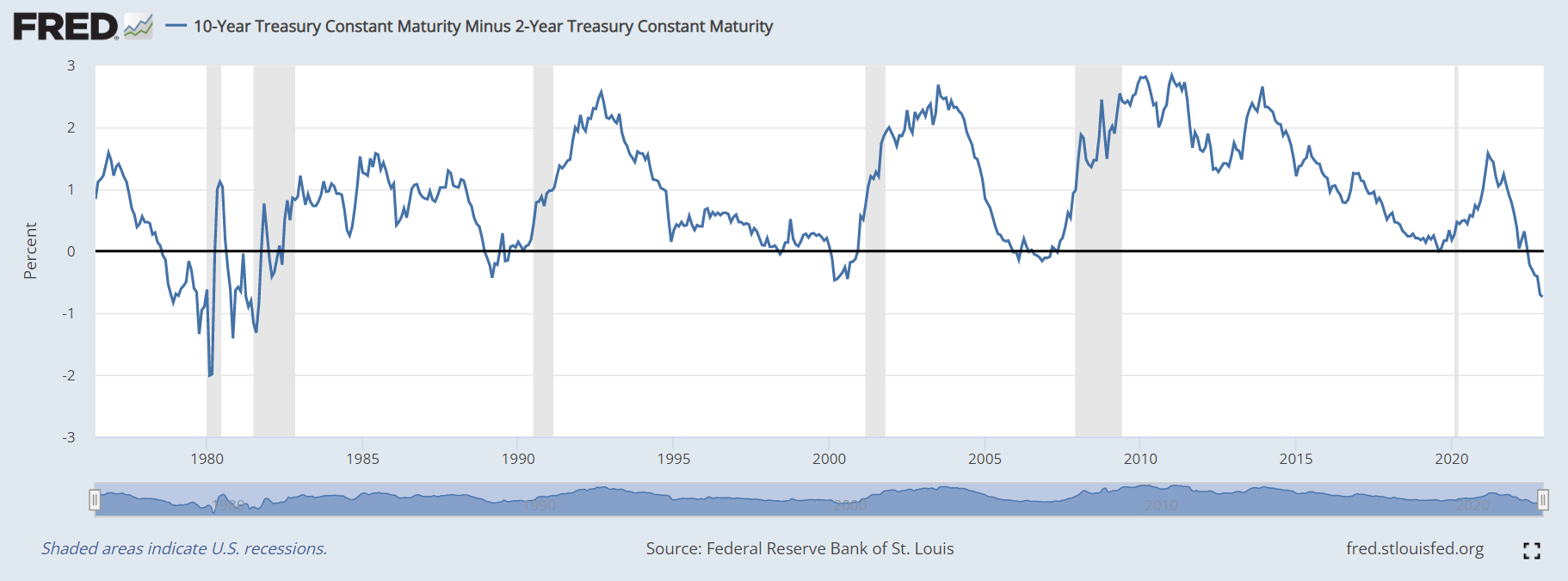

Upon realizing the major error, the Fed rushed to catch up with inflation, hiking the interest rates in 2022 aggressively – and in-process deeply inverted the yield curve. The 10Y-2Y yield curve spread has been inverted for most of the 2022 with the highest level of inversion since the inflationary spike of 1981.

FRED

The 10Y-3mo spread has just recently inverted, and the level of inversion is the highest on record (there is no data for late 1970s).

FRED

Here is the fact – the inverted yield curve leads to a recession within 12 months of initial inversion. This has been tested and retested using many different models. In fact, just observe the graphs above, the recession (shaded area) follows the yield curve inversion (the yield curve spread turns negative).

In fact, the Ney York Fed uses the 10Y-3mo spread as the sole variable to estimate the recession probability, and given the current level of inversion, a recession in 2023 is a virtual certainty.

Yet, the FOMC projects a 0.5% GDP growth for 2023. Very unlikely. The current level of yield curve inversion indicates a deep recession in 2023.

The question is what happens with inflation in 2023, even with a recession? The Russia-Ukraine war has no clear end in sight. The unfolding US-China economic decoupling trend can only accelerate. The anti-immigration policies in the US are unlikely to be changed going into the 2024 election. All this is inflationary. De-globalization is inflationary.

Market implications

The Fed Chair Powell was possibly hoping that the inflationary shock would be transitory, and now he’s hoping for a softish landing in 2023. The market participants are also hoping for a softish landing in 2023.

The broad stock market, as proxied by S&P 500 ETF (NYSEARCA:VOO), is overvalued and not priced for a recession. The VOO ttm PE ratio is above 19, and the forward PE ratio is near 18.

The PE ratio is a proxy for the earnings growth, so a relatively high multiple can be justified when the market expects a robust earnings growth. Alternatively, a high PE ratio can be justified when interest rates are very low.

The interest rates have considerably increased recently, and we are facing a recession where earnings could actually fall by 20%, which is typical for a recession. Even more importantly, the corporate credit spreads are likely to significantly rise as the recession hits, putting more pressure on stocks.

Market participants can only hope that the Fed would make a dovish pivot as the first signs of the recessions arrive and boost the stock market. But, they forget that de-globalization is inflationary, and the Fed might not be able to help as long as inflation is above the 2% target. Thus, don’t expect the Fed put in 2023.

Another hope is that the Fed would completely abandon the 2% inflation target (and also the World peace).

Be the first to comment