SrdjanPav/E+ via Getty Images

What an incredible snapback for growth stocks off the March 14 low. To be fair, the SPDR S&P 500 Growth ETF (SPYG) actually hit a nadir just above $58 back on February 24. The ETF managed to successfully test that level twice in March before surging higher. It closed above $68 on March 29.

Value Loses Relative Favor

Value stocks, as measured by the SPDR S&P 500 Value ETF (SPYV), have not recovered nearly as dramatically. But their rebound could be seen as more notable considering SPYV is within 1% of closing at a fresh all-time high. Value equities were favored toward the end of last year and through the Russia invasion saga. As geopolitical tensions have eased and as traders re-orient their attention toward the Fed, value stocks are suddenly less favored. Still, Vanguard Value ETF (VTV) notched fresh all-time highs on March 29 (total return).

Global Growth Slowdown: Good for Growth Shares?

Some are calling for a return to a low-growth scenario which often benefits growth stocks. In a world of slower GDP expansion, pockets of high-growth stocks are scarce, and thus, even more valuable. That is part of the narrative that drove the massive outperformance of a handful of large-cap growth names in the 2010s. As GDP growth accelerated in 2020 and 2021, investors could easily find stocks enjoying huge EPS gains, so value stocks outperformed much of that time.

But where do we go from here? Growth companies, thought to suffer when interest rates rise sharply, have been the clear winners since the middle of the month—all while short-term interest rates have surged. Is the value play over? Were a few short months of alpha all they could muster? We think not. Particularly looking at the sector skews of value vs growth.

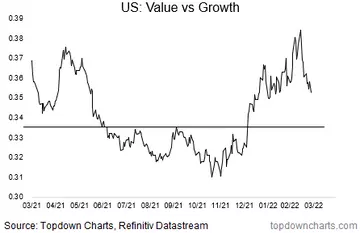

Featured Chart: Value Stocks in a Relative Retreat vs Growth

Topdown Charts, Refinitiv Datastream

A Corrective Phase Within a Broader Rally

Value vs growth established a rounded-bottom pattern during the back half of 2021. A breakout took place right around the turn of the year. Steadily rising interest rates and higher commodity prices no doubt favored some of the cyclical sectors. Big cap tech was also sold off heavily to start 2022.

The Nasdaq 100 hit bear market territory off its November peak—important since SPYG is 44% weighted to the Tech sector. By contrast, SPYV is more spread out with its biggest sector weight being Health Care and Financials at 16% each. The pair’s largest single-stock positions perhaps tell the story: Apple makes up 14% of SPYG while Berkshire Hathaway is 3.4% of SPYV.

Bottom Line: We remain bullish on value vs growth. Investors should consider that our timeframe on this outlook is relatively far out at 3-5 years and our conviction is low (pending tactical confirmation). The technical picture and, of course, macro drivers are considered.

Be the first to comment