benedek

Earnings of Valley National Bancorp (NASDAQ:VLY) will most probably surge this year on the back of acquired and organic loan growth. Further, expansion of the net interest margin amid a rising rate environment will lift earnings. Overall, I’m expecting Valley National to report earnings of $1.25 per share for 2022, up 11% year-over-year. Compared to my last report on the company, I’ve only slightly increased my earnings estimate. For 2023, I’m expecting earnings to grow by 24% to $1.55 per share. The year-end target price suggests a high upside from the current market price. Therefore, I’m maintaining a buy rating on Valley National Bancorp.

Organic Loan Growth to Decelerate

Valley National Bancorp’s loan book jumped by 23% in the second quarter, or 93% annualized, partly due to the acquisition of Bank Leumi USA. Additionally, organic loan growth was exceptionally strong at around 26% annualized for the quarter, as mentioned in the earnings release. Organic growth will most probably decline sharply in the second half of the year as the second quarter’s level was unsustainable. It was elevated because borrowers tried to lock in rates before interest rates could increase further. This preemptive or preponed borrowing has sucked out credit demand from the next few quarters. High borrowing costs will especially damage the residential mortgage segment, which makes up around 12% of total loans.

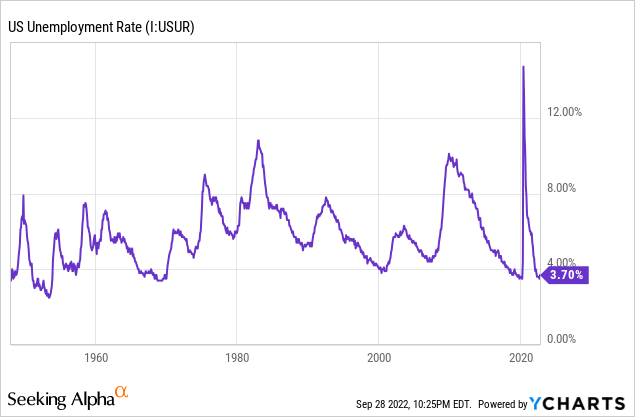

On the other hand, commercial loan growth will likely be satisfactory as the management mentioned in the conference call that the pipeline for commercial loans remained strong. Additionally, strong job markets bode well for loan growth. Valley National Bancorp’s operations are well diversified geographically. The company is present across New Jersey, New York, Florida, and Alabama. Therefore, the national average is appropriate to gauge the credit demand in Valley National’s markets. As shown below, the unemployment rate is currently near multi-decade lows.

The management mentioned in the conference call that it expects 8% to 10% annualized loan growth for the second half of 2022. Considering the factors given above, I’m expecting actual loan growth to miss the management’s target. I’m expecting the loan portfolio to grow by 1.5%, or 6% annualized, every quarter till the end of 2023. In my last report on Valley National, I estimated full-year loan growth of 21% for 2022. I’m now expecting a loan growth of 31% for this year. I haven’t changed my loan growth estimate for the second half of the year. However, my full-year estimate for 2022 is now higher than before because Valley National’s organic loan growth surprised me in the second quarter.

Meanwhile, I’m expecting deposits to grow in line with loans. The following table shows my balance sheet estimates.

| FY18 | FY19 | FY20 | FY21 | FY22E | FY23E | |||||

| Financial Position | ||||||||||

| Net Loans | 24,884 | 29,537 | 31,877 | 33,794 | 44,394 | 47,119 | ||||

| Growth of Net Loans | 36.6% | 18.7% | 7.9% | 6.0% | 31.4% | 6.1% | ||||

| Other Earning Assets | 4,030 | 4,199 | 4,913 | 5,855 | 6,110 | 6,233 | ||||

| Deposits | 24,453 | 29,186 | 31,936 | 35,632 | 45,207 | 47,981 | ||||

| Borrowings and Sub-Debt | 3,773 | 3,271 | 3,500 | 2,136 | 3,043 | 3,105 | ||||

| Common equity | 3,141 | 4,174 | 4,382 | 4,874 | 6,275 | 6,817 | ||||

| Book Value Per Share ($) | 9.4 | 12.3 | 10.8 | 11.8 | 12.3 | 13.4 | ||||

| Tangible BVPS ($) | 5.9 | 8.0 | 7.2 | 8.1 | 8.2 | 9.3 | ||||

|

Source: SEC Filings, Author’s Estimates (In USD million unless otherwise specified) |

||||||||||

Deposit Costs have Become Stickier than Before

Valley National Bancorp’s deposit cost is somewhat sticky due to the presence of non-interest-bearing deposits, which make up 36.8% of total deposits. Although it’s still not entirely enviable, the deposit mix has improved substantially over the first half of this year. Non-interest-bearing deposits increased to 36.8% at the end of June 2022 from 32.8% at the end of December 2021.

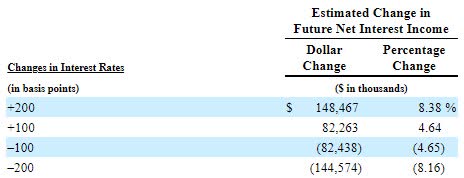

Partly due to the low deposit beta, Valley National Bancorp’s margin is moderately rate-sensitive. According to the results of the management’s interest-rate sensitivity analysis given in the 10-Q filing, a 200-basis points hike in interest rates could boost the net interest income by 8.38% over twelve months.

2Q 2022 10-Q Filing

As mentioned in the earnings presentation, Valley National originated new loans during the second quarter at a higher rate than the average portfolio rate. Therefore, loan additions in the remainder of the year are very likely to lift the average earning-asset yield, and consequently the margin.

Considering these factors, I’m expecting the margin to grow by 40 basis points in the second half of 2022 and a further 10 basis points in 2023. Compared to my last report on Valley National, I’ve raised my margin estimate because the ongoing up-rate cycle is more extreme than I previously expected.

Provisioning Likely to Remain Above Average

Valley National’s provisions expenses for loan losses surged in the second quarter due to the acquisition of Bank Leumi USA. Following the acquisition, non-accrual loans were 0.72% of total loans while allowances were 1.13% of total loans at the end of June 2022. As the economic outlook has worsened over the last three months, the provisioning for expected loan losses will likely see an uptick. Further, loan additions will require provisioning for expected loan losses.

Overall, I’m expecting the net provision expense to be above average through the end of 2023. I’m expecting the net provision expense to make up 0.11% of total loans every quarter on an annualized basis. In comparison, the net provision expense averaged 0.09% from 2017 to 2019. In my last report on Valley National, I estimated a net provision expense of $36 million for 2022. I’ve now almost doubled my estimate for the full year to $74 million because the acquisition-driven provision expense jump in the second quarter was higher than I expected.

Expecting Earnings to Grow by 11%

Earnings will likely surge this year due to the acquired and organic loan growth. Further, margin expansion will support the bottom line. On the other hand, higher provisioning will restrict earnings growth. Overall, I’m expecting Valley National to report earnings of $1.25 per share for 2022, up 11% year-over-year. For 2023, I’m expecting earnings to grow by 24% to $1.55 per share. The following table shows my income statement estimates.

| FY18 | FY19 | FY20 | FY21 | FY22E | FY23E | |||||

| Financial Summary | ||||||||||

| Net interest income | 857 | 898 | 1,119 | 1,210 | 1,776 | 2,069 | ||||

| Provision for loan losses | 33 | 24 | 126 | 33 | 74 | 52 | ||||

| Non-interest income | 134 | 215 | 183 | 155 | 209 | 207 | ||||

| Non-interest expense | 629 | 632 | 646 | 692 | 1,064 | 1,142 | ||||

| Net income – Common Sh. | 249 | 297 | 378 | 461 | 614 | 788 | ||||

| EPS – Diluted ($) | 0.75 | 0.87 | 0.93 | 1.12 | 1.25 | 1.55 | ||||

|

Source: SEC Filings, Author’s Estimates (In USD million unless otherwise specified) |

||||||||||

In my last report on Valley National, I estimated earnings of $1.21 per share for 2022. My updated earnings estimate is barely changed because the upward revisions in loan growth and margin estimates cancel out the upward revisions in provision expenses and operating expenses.

Actual earnings may differ materially from estimates because of the risks and uncertainties related to inflation, and consequently the timing and magnitude of interest rate hikes. Further, a stronger or longer-than-anticipated recession can increase the provisioning for expected loan losses beyond my estimates.

High Price Upside Warrants a Buy Rating

Valley National is offering a dividend yield of 4.0% at the current quarterly dividend rate of $0.11 per share. The earnings and dividend estimates suggest a payout ratio of 31% for 2022, which is much below the five-year average of 59%. Nevertheless, I’m not expecting an increase in the dividend level because Valley National does not change its dividend level frequently. The company has maintained its quarterly dividend at $0.11 per share since the last quarter of 2013.

I’m using the historical price-to-tangible book (“P/TB”) and price-to-earnings (“P/E”) multiples to value Valley National Bancorp. The stock has traded at an average P/TB ratio of 1.53 in the past, as shown below.

| FY18 | FY19 | FY20 | FY21 | Average | ||

| T. Book Value per Share ($) | 5.9 | 8.0 | 7.2 | 8.1 | ||

| Average Market Price ($) | 11.8 | 10.7 | 8.4 | 13.2 | ||

| Historical P/TB | 1.99x | 1.34x | 1.16x | 1.64x | 1.53x | |

| Source: Company Financials, Yahoo Finance, Author’s Estimates | ||||||

Multiplying the average P/TB multiple with the forecast tangible book value per share of $8.23 gives a target price of $12.6 for the end of 2022. This price target implies a 13.2% upside from the September 28 closing price. The following table shows the sensitivity of the target price to the P/TB ratio.

| P/TB Multiple | 1.33x | 1.43x | 1.53x | 1.63x | 1.73x |

| TBVPS – Dec 2022 ($) | 8.23 | 8.23 | 8.23 | 8.23 | 8.23 |

| Target Price ($) | 10.9 | 11.8 | 12.6 | 13.4 | 14.2 |

| Market Price ($) | 11.1 | 11.1 | 11.1 | 11.1 | 11.1 |

| Upside/(Downside) | (1.6)% | 5.8% | 13.2% | 20.6% | 28.0% |

| Source: Author’s Estimates |

The stock has traded at an average P/E ratio of around 11.9x in the past, as shown below.

| FY18 | FY19 | FY20 | FY21 | Average | ||

| Earnings per Share ($) | 0.75 | 0.87 | 0.93 | 1.25 | ||

| Average Market Price ($) | 11.8 | 10.7 | 8.4 | 13.2 | ||

| Historical P/E | 15.8x | 12.2x | 9.0x | 10.5x | 11.9x | |

| Source: Company Financials, Yahoo Finance, Author’s Estimates | ||||||

Multiplying the average P/E multiple with the forecast earnings per share of $1.25 gives a target price of $14.9 for the end of 2022. This price target implies a 33.9% upside from the September 28 closing price. The following table shows the sensitivity of the target price to the P/E ratio.

| P/E Multiple | 9.9x | 10.9x | 11.9x | 12.9x | 13.9x |

| EPS 2022 ($) | 1.25 | 1.25 | 1.25 | 1.25 | 1.25 |

| Target Price ($) | 12.4 | 13.6 | 14.9 | 16.1 | 17.4 |

| Market Price ($) | 11.1 | 11.1 | 11.1 | 11.1 | 11.1 |

| Upside/(Downside) | 11.4% | 22.6% | 33.9% | 45.2% | 56.4% |

| Source: Author’s Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $13.7, which implies a 23.6% upside from the current market price. Adding the forward dividend yield gives a total expected return of 27.5%. Hence, I’m maintaining a buy rating on Valley National Bancorp.

Be the first to comment