Justin Sullivan/Getty Images News

Introduction

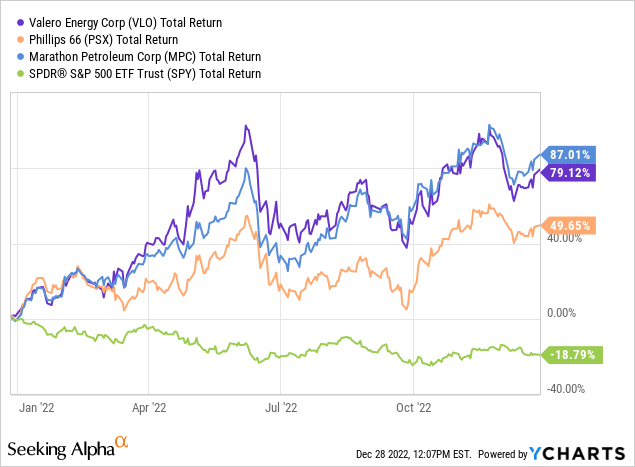

2022 was an incredibly exciting year. While it wasn’t fun for stocks, in general, we got to discuss a wide range of important and fascinating macroeconomic topics. Some of these were great for energy companies. Rebounding post-pandemic demand, tight supplies, and the war in Ukraine were great tailwinds for refinery stocks. One of them is Valero Energy Corporation (NYSE:VLO), which added more than 68% to its market cap, outperforming the market by a mile. Only its peer Marathon Petroleum (MPC) did better as it bought back stock more aggressively.

In this article, we’ll discuss what I expect in 2023 as we’ll likely deal with much slower economic growth hurting gasoline demand, ongoing supply tightness, and hopefully (likely) an aggressive dividend hike. After all, VLO has not hiked its dividend since the pandemic. Improved fundamentals allow for a return to aggressive future dividend growth.

So, let’s get to it!

Tight Supply

One of the most widely-followed economic indicators of the average consumer is the price of gasoline. Most consumers do not engage in macro research unless it’s for their stock portfolio or part of their job. Gasoline prices, however, impact everyone. It drives both consumer sentiment and presidential approval ratings.

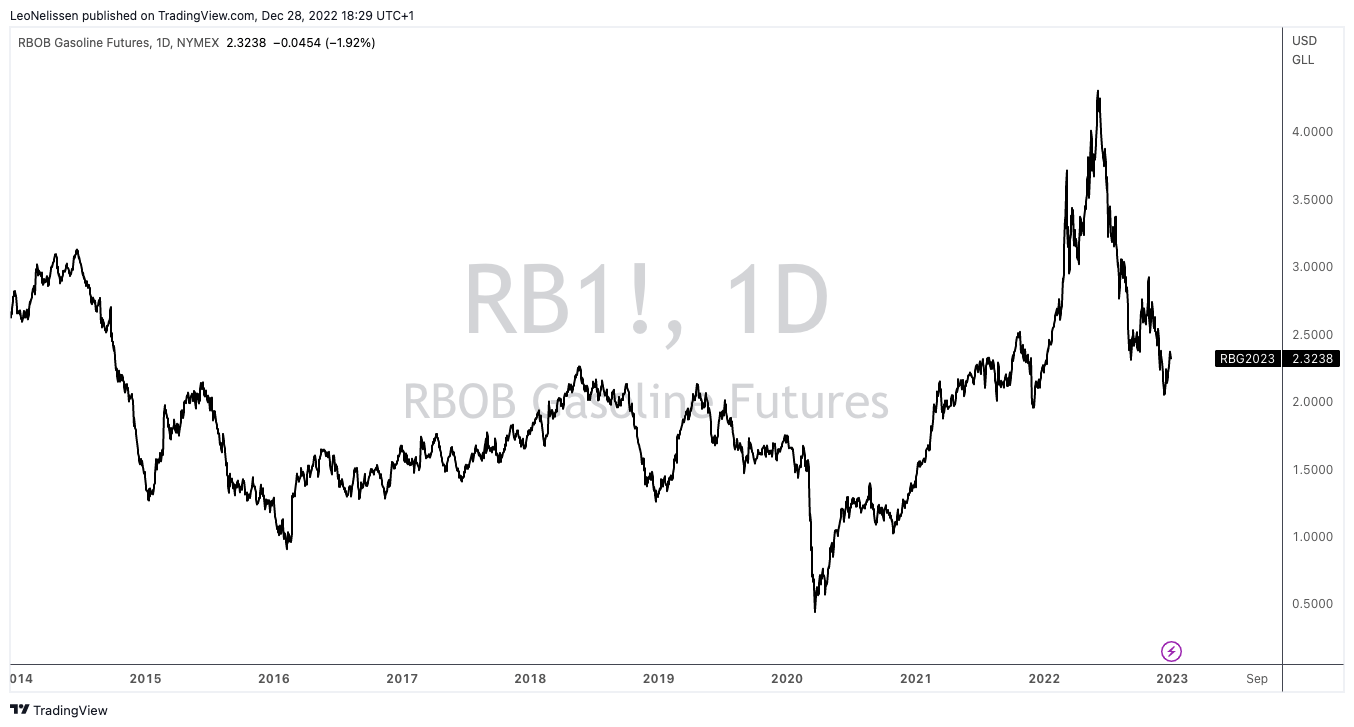

This year, we were bombarded with gasoline price headlines as RBOB gasoline futures briefly touched $4.30 per gallon. That’s more than double the pre-crisis median price.

TradingView (RBOB Gasoline Futures)

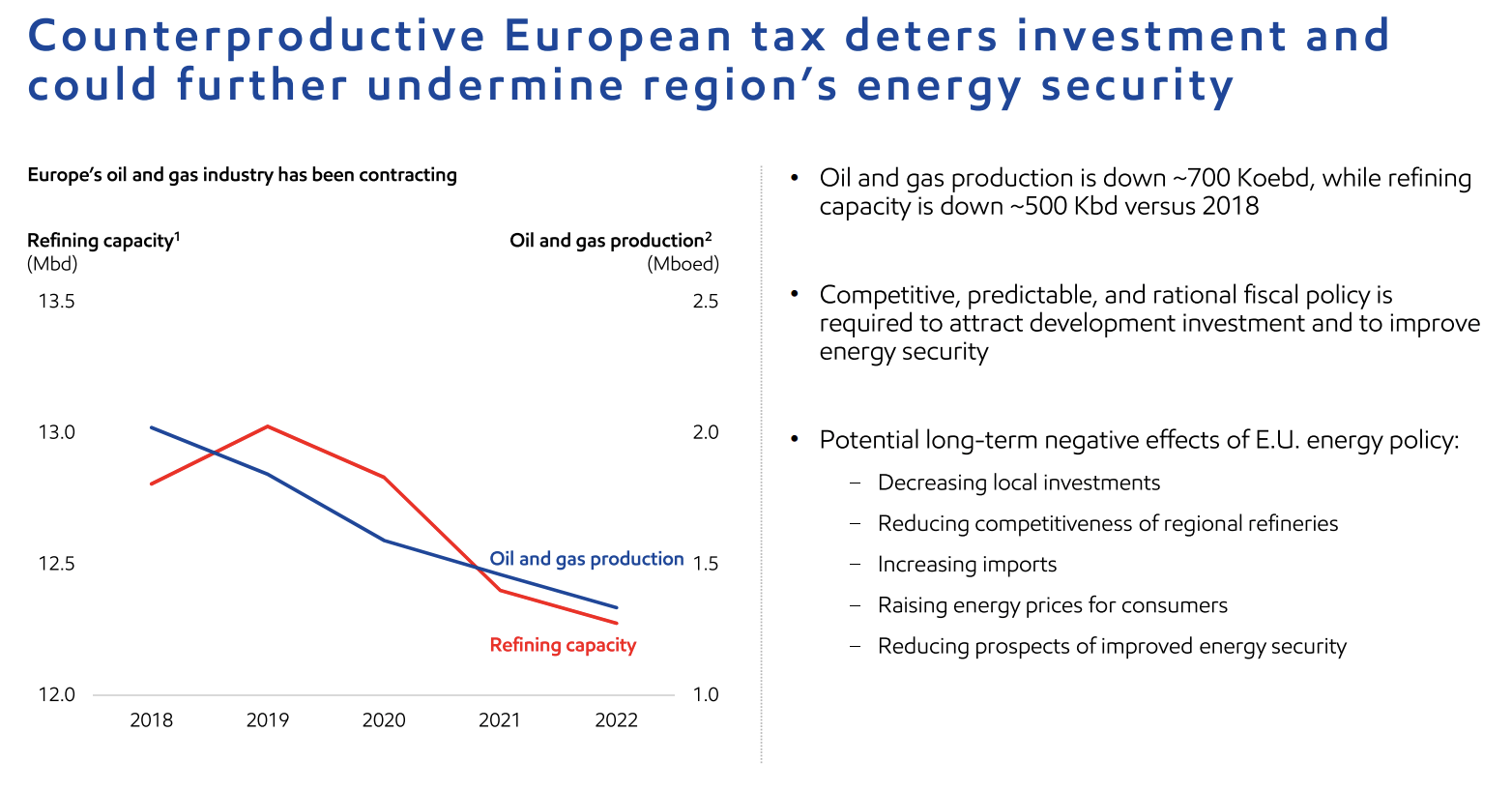

On the one hand, this was caused by the war in Ukraine, which has caused much-needed oil flows from Russia to Europe to plummet (mainly due to sanctions).

On the other hand, refining capacity was already in a long-term downtrend before the start of the war. Strict environmental policies and the fact that building and maintaining refineries is extremely capital intensive have caused refining capacity to drop by 500 thousand barrels per day since 2018, according to Exxon Mobil (XOM) numbers.

Exxon Mobil

As Europe still requires petroleum products, it put more pressure on foreign producers – in an already tight market.

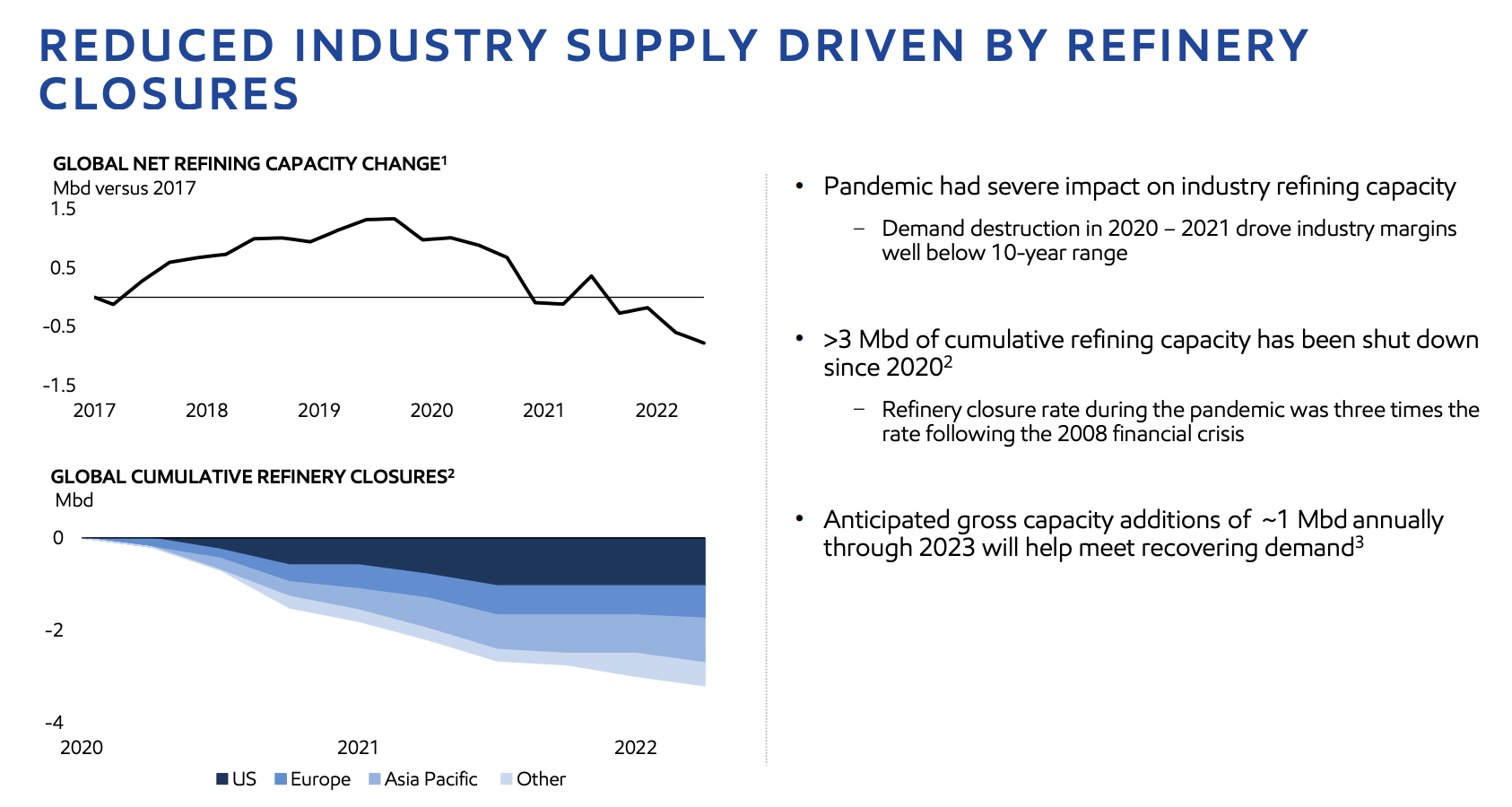

And speaking of Exxon, it’s the only company expanding refinery operations in the United States. I’m bringing this up to highlight how tight the US market has become.

Over the past three years, the US market has lost 1.3 million barrels per day in refining capacity.

The same holds true for the global market.

Exxon Mobil

According to the Energy Information Administration (EIA):

The International Energy Agency estimates that global refining capacity decreased by 910,000 barrels per day (b/d) in 2021—the first decline in global refining capacity in 30 years. In the United States, refining capacity has decreased by about 1.1 million b/d since the start of 2020, contributing 184,000 b/d to the global decline in 2021.

The recovery in global output will be slow. This year, the surge will likely be 1.0 million barrels per day. In 2023, that number could be 1.6 million barrels.

However, all projects will be outside of the United States and Europe, except for Exxon’s Beaumont expansion.

When Can We Expect Dividend Growth To Resume?

While favorable industry fundamentals boosted capital returns, they did not result in a higher dividend.

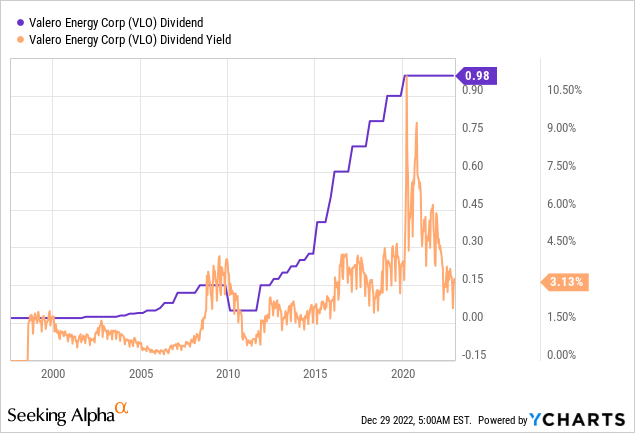

Valero currently pays a $0.98 quarterly dividend per share. This translates to a 3.1% dividend yield.

3.1% is not a very high yield. In most cases, it is not enough to convince people to invest in highly cyclical energy stocks. Most demand a higher yield – and rightfully so.

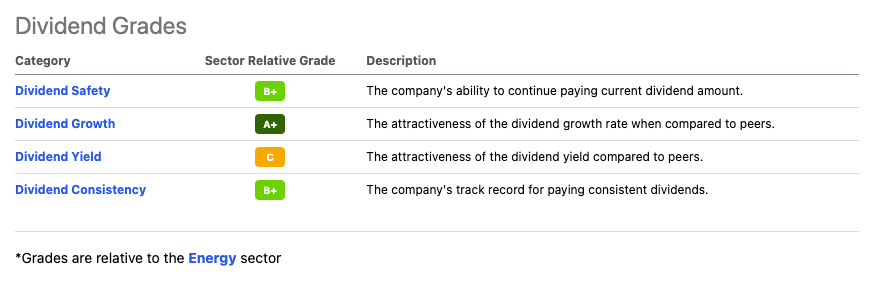

Looking at the Seeking Alpha dividend scorecard below, we see that the yield is the worst-graded category. It also does not help that the energy sector is now filled with high-yielding cash cows as a result of the energy bull market.

Seeking Alpha

One of the many reasons why VLO is still so attractive is the fact that the company is a dividend growth stock, as the high relative score in the table above shows.

At this point people may disagree as Valero’s most recent hike was announced in January 2020. However, I like to look at the bigger picture, which shows that the stock is indeed a dividend growth stock.

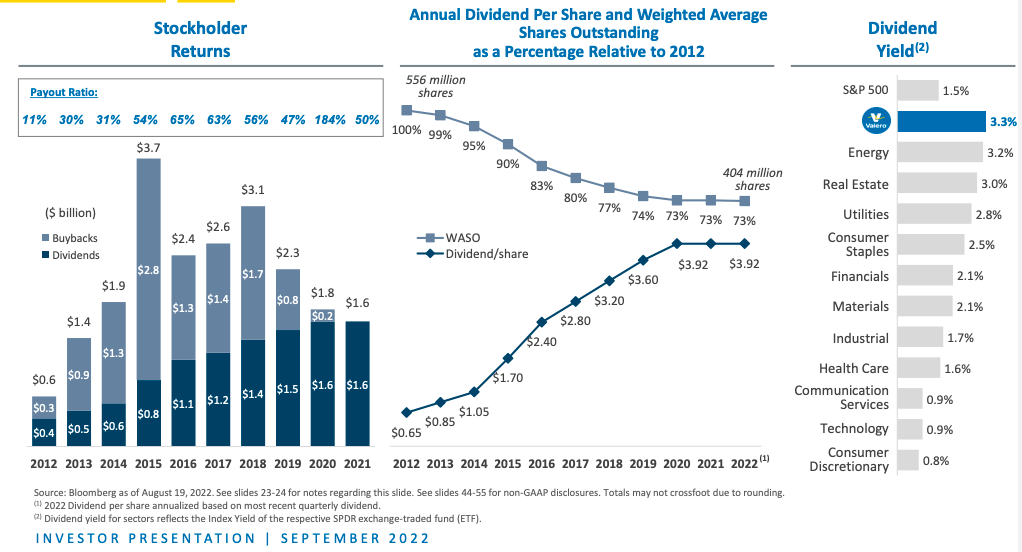

Using Seeking Alpha’s numbers, the company has a 10-year compounded annual growth rate of 20.8%. Note that this includes two years without dividend growth. That’s impressive.

The 5-year dividend CAGR is obviously a lot less high at 7.0%.

On top of that, the company used to spend as much on buybacks as on dividends. Since 2012, the company has bought back 27% of its shares outstanding.

Valero Energy

As the overview above shows, the company has maintained a conservative payout ratio in most years. In 2020, that was not possible as lockdowns caused a scenario where the company didn’t even have enough operating cash flow to service capital expenses. However, VLO did not cut its dividend. It used its healthy balance sheet to maintain the dividend it hiked just a month before the bad news from Wuhan broke.

Now, the question is, when will dividend growth return?

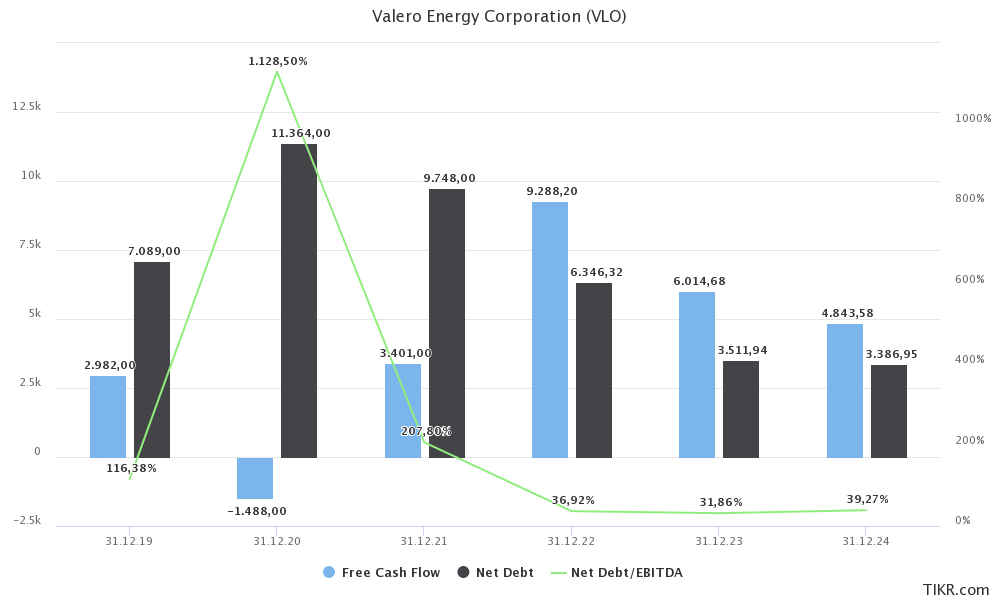

Financially speaking, it’s time for a hike. The company’s net debt is expected to end this year at $6.3 billion. That is below 2019 levels. Moreover, the net leverage ratio is expected to be less than 0.4x EBITDA – and expected to remain that low in the years ahead.

TIKR.com

Moreover, next year’s $6.0 billion free cash flow estimate implies a 12.4% free cash flow yield. In other words, the company could (technically) pay a dividend of 12.4%. That won’t happen – especially because FCF is expected to moderate. However, it shows how much free cash flow the company is generating. Even if FCF moderates, there is a very strong case for the return to high dividend growth.

Year-to-date (first three quarters of 2022), the company has returned 40% of adjusted net operating cash flow to shareholders through dividends and buybacks. That is at the lower end of its 40% to 50% payout ratio as it continued to emphasize its balance sheet.

The company itself did not mention a specific target date to hike the dividend. It is trying to assess the changing macroeconomic environment and looking to lower its debt-to-capital ratio to the lower end of the 20% to 30% range. Right now, that number is 24.5%.

In other words, I’m positive that the first half of 2023 will see a dividend hike. The size of that hike will likely depend on the company’s macroeconomic outlook.

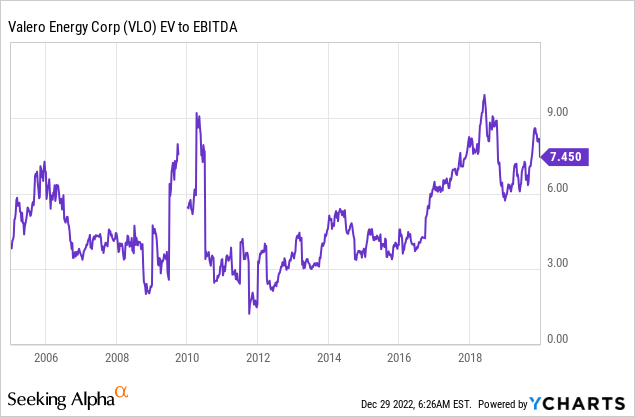

Valuation & Growth Slowing

Valero Energy is trading at 4.9x 2023E EBITDA of $54.2 billion. This is based on its $48.3 billion market cap, $3.5 billion in 2023E net debt, $1.8 billion in minority interests (tied to Diamond Green Diesel), and roughly $600 million in pension-related liabilities.

This is a very fair valuation. The same goes for the aforementioned implied free cash flow yield of more than 12%.

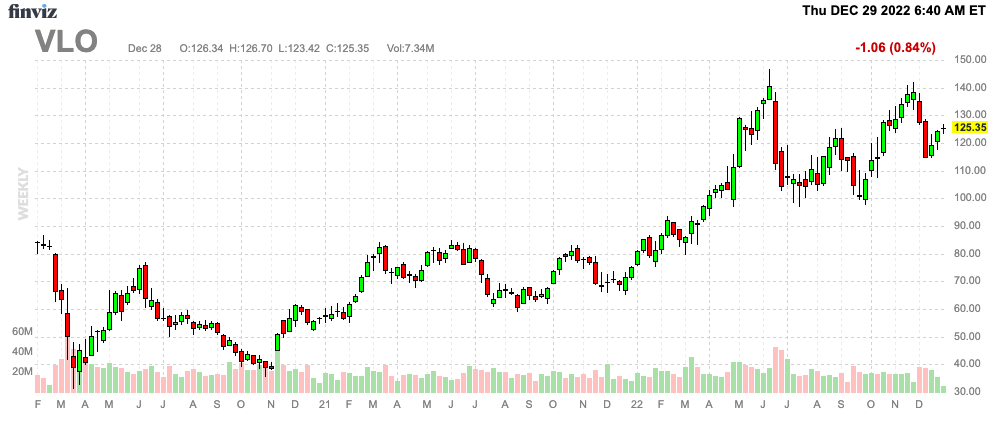

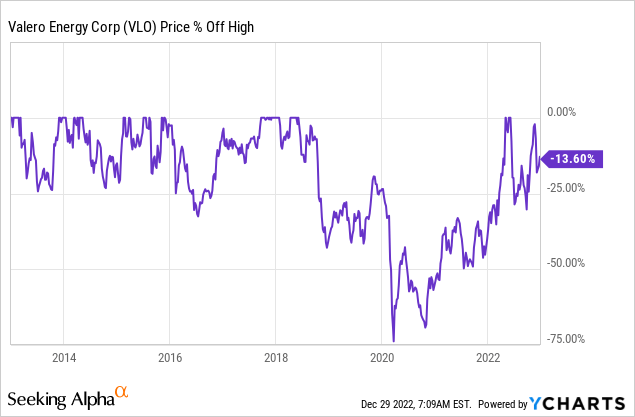

Despite this valuation, the stock is down 15% from its 52-week high and unchanged since May.

FINVIZ

The problem is that the market has digested a lot of the good news (like shortages keeping margins high).

Meanwhile, the market will likely be forced to price in slower economic growth down the road – or even contraction depending on the severity of the recession in 2023.

Wells Fargo

Moreover, as I wrote in a recent economic outlook article, I believe that the pressure on the economy will continue to build as the Fed is eager to get inflation down as fast as possible.

This is the longer-term outlook I gave in that article:

- The Fed is feeling tremendous pressure to control inflation. That makes sense as the US economy is consumer-driven. Also, high inflation can quickly turn into lasting above-average inflation once wages and spending habits adjust. That’s a no-go!

- Hence, I believe that the Fed will not be scared to do damage to the US economy to achieve its target of lower inflation. This includes hurting housing demand/prices, unemployment, and consumer spending.

- Once the Fed pivots (I still believe it will happen in 2023), the economy will slowly adjust to lower rates. Demand will come back. So will inflation.

- Given the aforementioned secular factors, I believe we are in a prolonged period of Fed hikes and cuts at above-average rates (versus 2009-2021).

Hence, I believe that Valero will refrain from breaking out until a Fed pivot allows economic demand expectations to rebound.

Personally, I’m fine with that. I still believe that Valero will hike its dividend and benefit from industry supply shortages. That will provide the company with tailwinds in an environment of economic decline.

It’s also great for long-term investments, My strategy is to buy corrections. If we ignore what happened in 2020 (lockdowns), the stock regularly sells off 25%, which is roughly what I use as a guideline when adding to my Valero position.

Takeaway

Valero is one of my favorite high-yield stocks. Unfortunately, the company does not have a high yield, as capital gains in 2021 and 2022 were not supported by post-pandemic dividend growth.

However, that does not make the stock less attractive. All signs point to the return of dividend growth in 2023 thanks to rapid debt reduction supported by high demand and tight industry supply.

Unfortunately, economic expectations are quickly deteriorating, which is causing me to be on the lookout for stock price weakness in 2023. While I do expect the stock to break out as soon as post-pivot demand rebounds, I believe we will be able to buy the stock at least 25% cheaper.

If we were to get such an opportunity, we would be dealing with a yield of almost 4.0% (excluding any hikes), which is a great deal and a reasonable target for long-term investors looking for VLO exposure.

(Dis)agree? Let me know in the comments!

Be the first to comment