Luca Sage

Investment Thesis

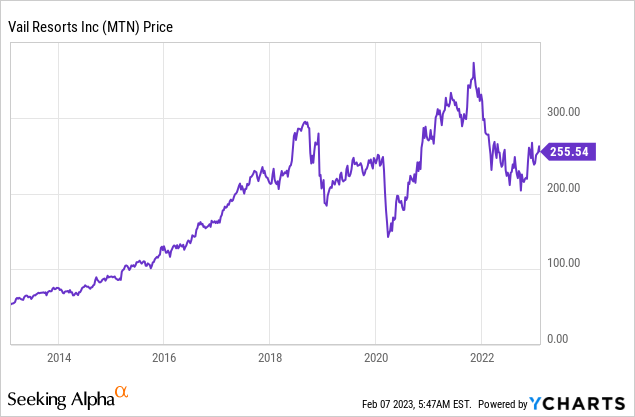

Vail Resorts (NYSE:MTN) is one of the largest ski resort companies in the world. It owns 41 ski resorts across multiple countries such as the US, Canada, Australia, and Switzerland. The company has performed well during the past decade, with shares up over 360% during the period despite facing significant disruption from the pandemic in 2020, comfortably beating the S&P 500 Index. I believe Vail Resorts is a great company for investors that want growth and dividend at the same time.

The company has an unmatched number of ski resorts that create a strong moat and should continue to grow steadily. The ongoing shift from selling lift tickets to passes will also provide better revenue stability and help offsets seasonality. Its current valuation seems appealing as multiples are near 10-year historical lows while the dividend yield is near the historical high. I rate MTN stock as a buy at the current price.

Why Vail Resorts?

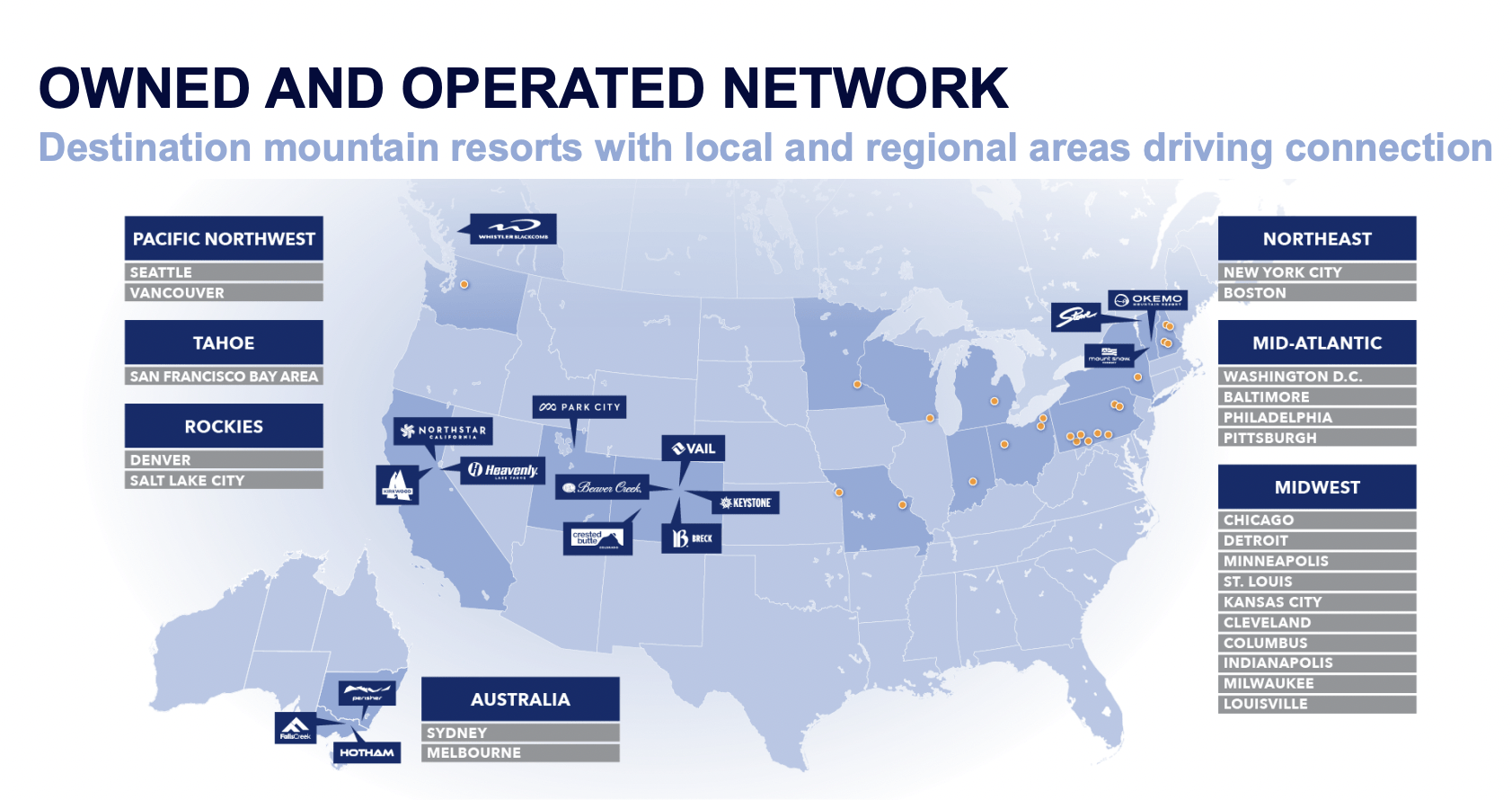

I believe Vail Resorts have a strong competitive advantage against other ski resorts. Unlike hotels that can keep building and expanding, opening a new ski resort is nearly impossible due to the constrained supply of mountains. Yet, a strong portfolio of resorts is one of the keys to success. The resorts that operate only in one location may struggle the whole year due to weather inconsistencies. While Vail Resorts is able to diversify the location and encourage customers to go to another resort if the weather is bad in certain areas.

Thanks to this, the company is able to increase the price and attractiveness of its passes as competitors are not able to provide such alternatives. Not to mention it also operates ski resorts overseas. As the company continues to grow in size, it also has much more money to invest in other services such as lodging and dining which improves the overall experience. Vail Resorts is able to provide the most complete offerings which drive customer loyalty and it is just very hard for smaller resorts to compete in the long run.

Vail Resorts

From Ticket To Pass

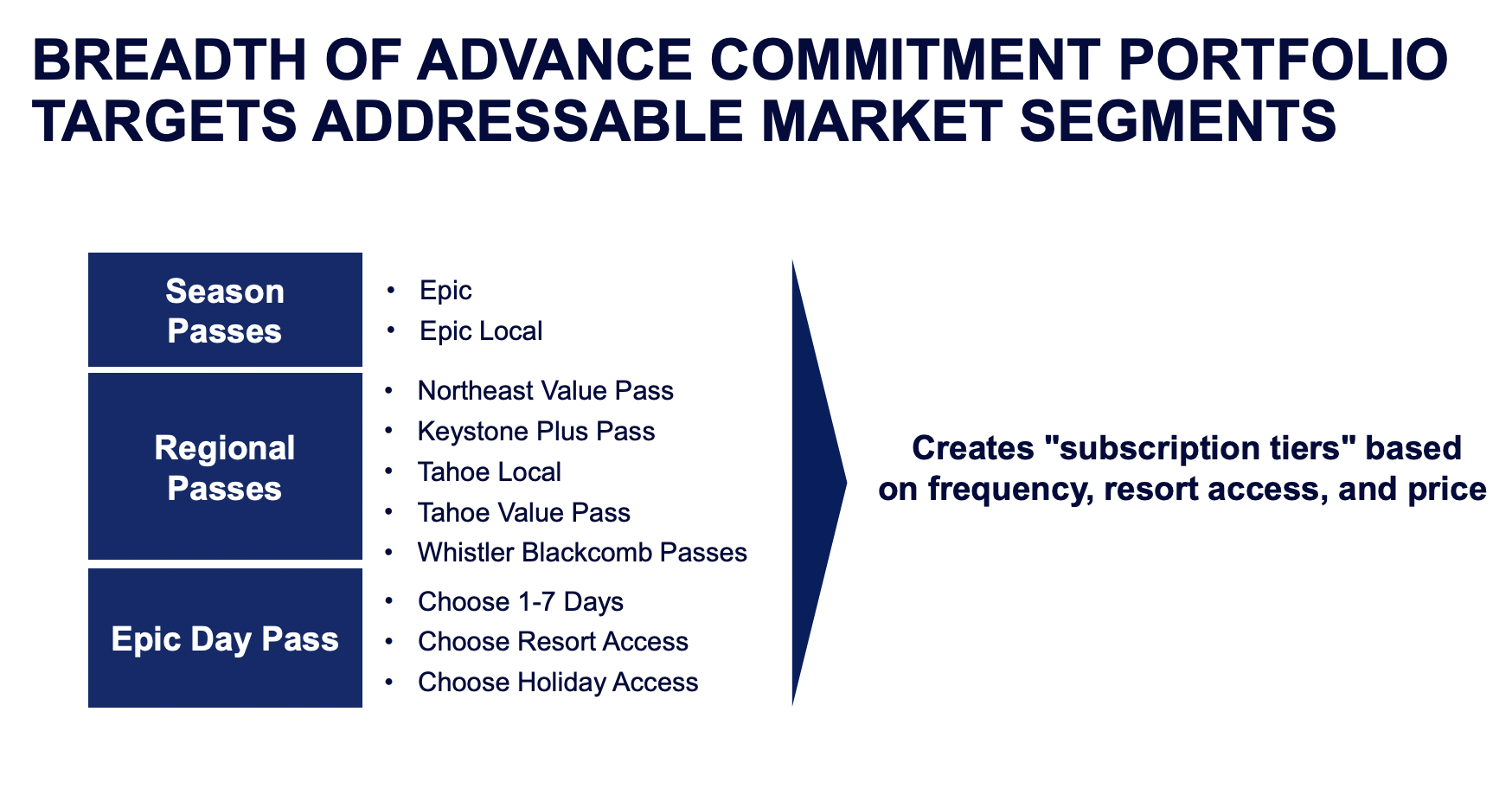

Vail Resorts continues its effort to shift customers’ focus from lift tickets to passes. The company is offering discounted passes to attract customers to make purchases in advance of their travel dates, and they often purchase higher-tier passes (e.g. multi-day or seasonal) as they think it has better value. For instance, 10.4% of pass holders have trade-up in FY22, up from just 0.4% in 2020. Customers tend to have stronger commitments and spend more time at the resorts as they have already paid in advance which results in higher spending on lodging and other services such as food. Seasonal passes also encourage skiers to visit more on weekdays and non-holidays which helps utilize excess capacity.

The focus on passes has been seeing strong success. The number of passes grew 76% from FY20-FY22. Pass revenue grew from just $78 million in FY08 to $795 million in FY22, representing an impressive CAGR (compounded annual growth rate) of 18.1%. In FY08, passes only accounts for 26% of lift revenue (lift tickets + passes). The figure has grown to 62% last fiscal year and the company hopes it can reach over 75% over the long run. I believe the shift to passes will continue to be a strong growth driver moving forward.

Vail Resorts

Valuation and Dividends

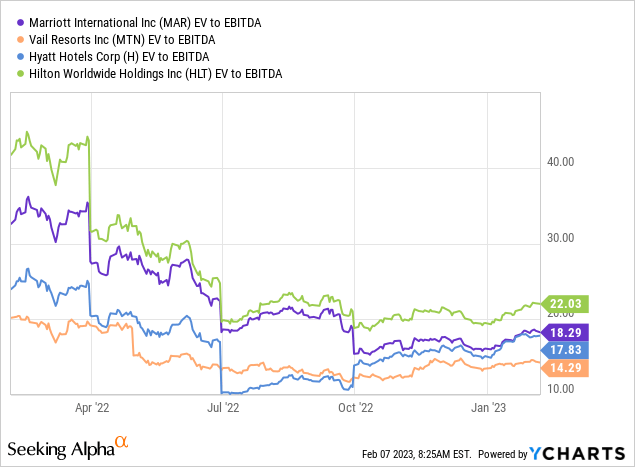

After the 30% drop in share price since late 2021, the valuation is starting to look attractive. The company is currently trading at an EV/EBITDA ratio of 14.29x which is pretty cheap (I am using the EV/EBITDA ratio as it takes the debt into account as well). From the first chart below, you can see that its multiple is way below other hotel companies (since there are no other public ski resort companies) such as Marriott (MAR), Hilton (HLT), and Hyatt (H). The average EV/EBITDA of these hotels is 19.38x, which represents a premium of 35.6%. The current valuation is also discounted on a historical basis. Its 5-year average EV/EBITDA was 20.33x which is much more expensive compared to 14.29x. A return to historical averages should provide decent upside potential from current levels.

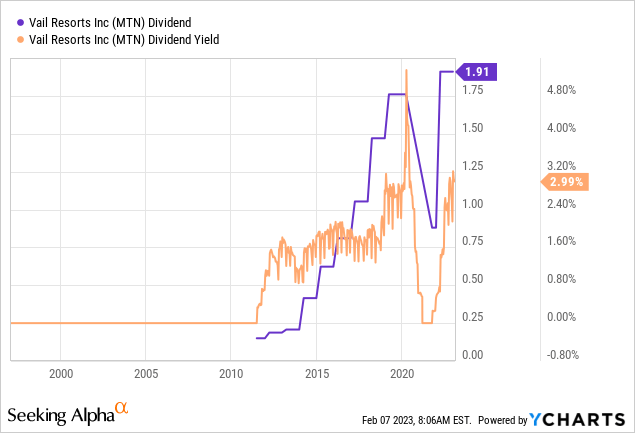

Vail Resorts is a wonderful dividend growth company in my opinion. Besides the dividend cut in 2020 due to the unprecedented pandemic, the company has increased its payout every year. The increase has also been very generous. The first quarterly dividend declared in 2011 was $0.15 and has grown to $1.91 in the latest quarter, which represents an insane increase of over 1,200% in just 12 years. Thanks to that the dividend yield has also grown from roughly 0.4% to 2.99% currently. From the second chart below, you can see that the current yield is now near an all-time high.

Investor Takeaway

Vail Resorts is a nice dividend growth stock with strong fundamentals. While many are bashing its pricing which is understandable, the company continues to deliver year after year. Ski resorts have insane entry barrier that limits the threat from other companies that try to enter the space. Its broad portfolio of ski resorts provides strong competitive advantages against smaller competitors and allows them to raise prices every year and still maintain healthy visiting volumes. The transition from lift tickets to pass should continue to improve revenue stability and customer commitment, which often results in higher service revenue. After the pullback, the company is trading at a compelling valuation with multiples meaningfully below hotel companies and its own historical average. The dividend yield is also near an all-time high with ongoing increases expected, as cash flow remains healthy. I believe Vail Resorts will continue to outperform, therefore I rate it as a buy.

Be the first to comment