LauriPatterson/E+ via Getty Images

Description

Utz Brands, Inc. (NYSE:UTZ) (“the company”) is a middle-sized manufacturer of branded salty snacks, including potato chips, tortilla chips, pretzels, cheese snacks, pork skins, veggie snacks, pub/party mixes, and other snacks. The company’s portfolio includes brands like Utz, Zapp’s, ON THE BORDER, Golden Flake, Good Health, and Boulder Canyon.

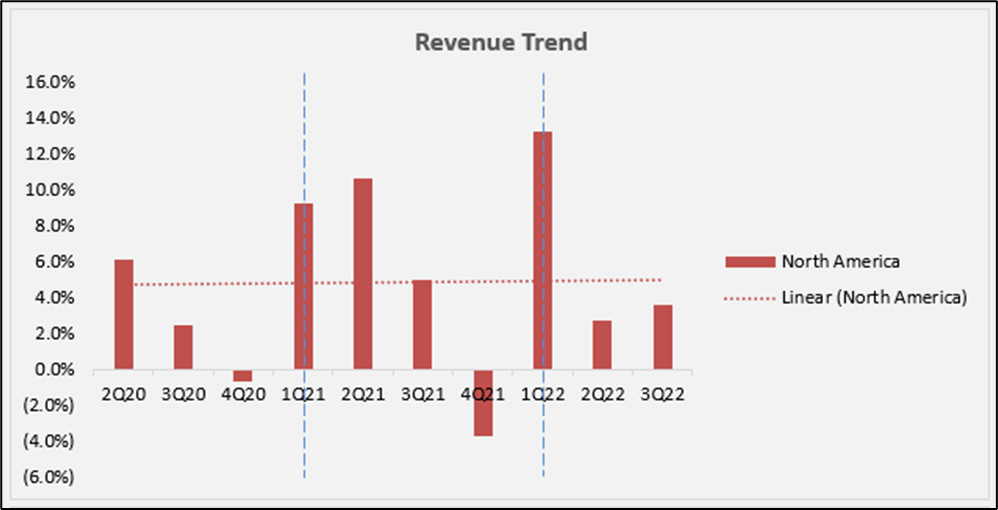

Below, you can see how the company did recently.

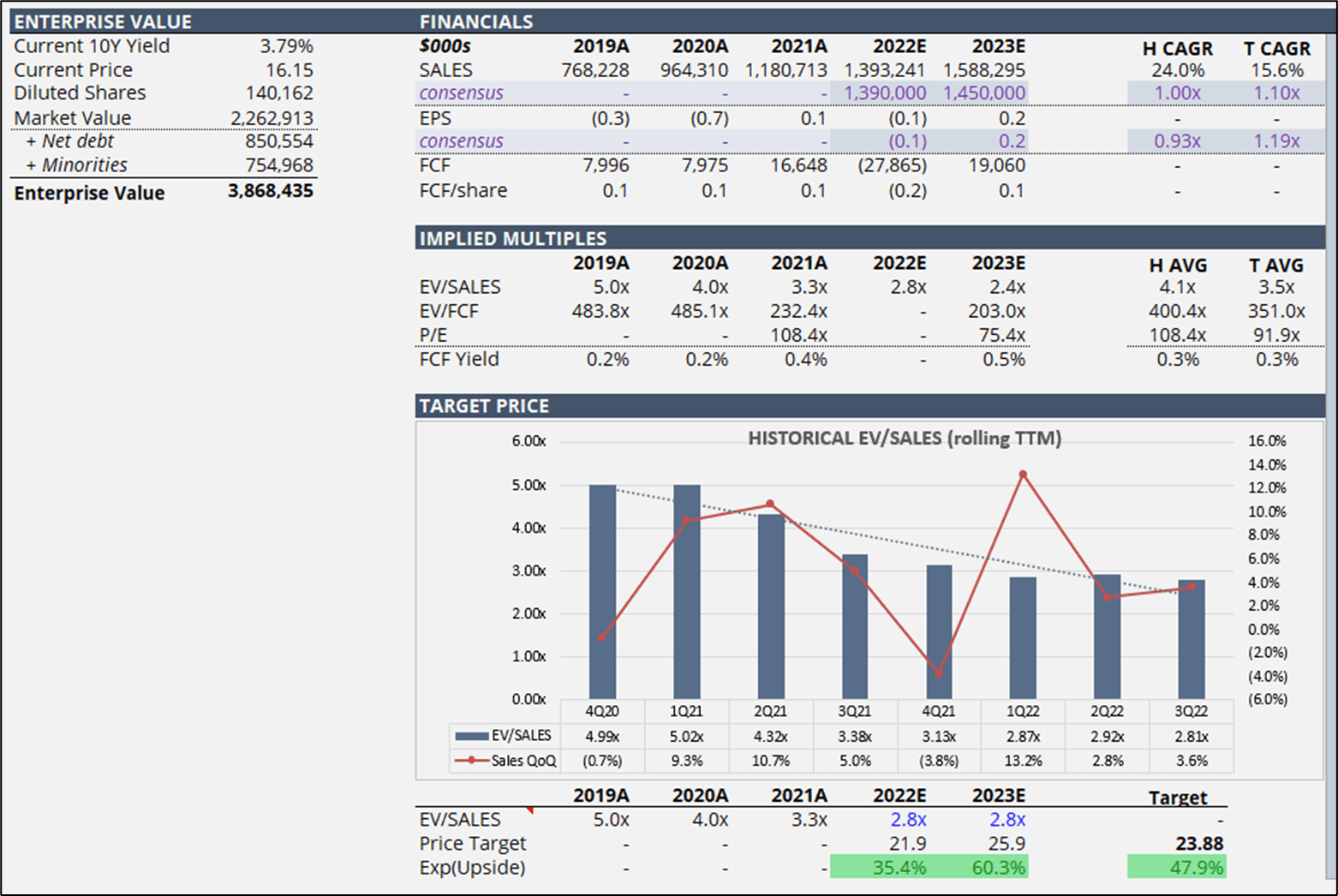

Author’s Estimates

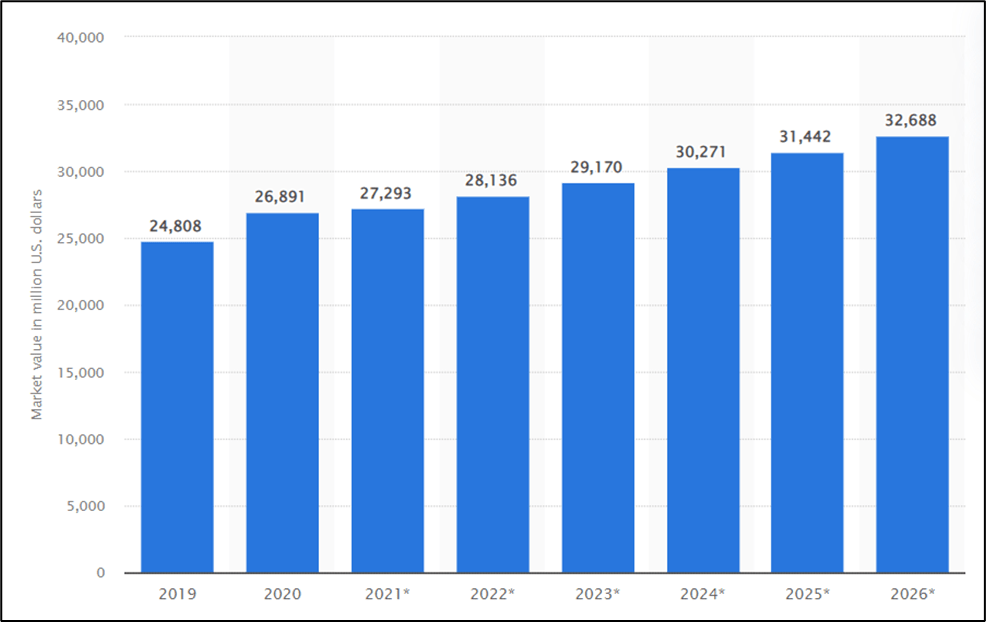

The company is, relative to the U.S. salty snacks market, a small player (TTM 4.95% market share) that is growing very fast.

In fact, while the overall market grew at a CAGR of 4.9% over the 2017-2021 period, the company’s revenue grew at a CAGR of 24.0% (4.9x the market’s CAGR) over the same period. This is a positive trend that I expect to continue in the future, driven by the company’s future plan to be well-established across the U.S. and not only in the Northeast.

Statista

Company Valuation

Competition

The company operates in a highly competitive industry, with few barriers to entry. The competition is represented by well-established companies like PepsiCo (PEP) as well as private labels. The latter, in particular, was addressed during the 1Q22 earnings call:

The private label threat within our subcategory has remained minimum as private label dollar share in the salty snacks category has per IRI, declined for the last 16 12-week periods.

Now, private labels represent a threat, however, if you had ever tried the product you may immediately understand that the threat is present but it is not a big deal (not yet at least). Personally, I believe that the product is delicious and the company keeps doing a great job by adding new flavors.

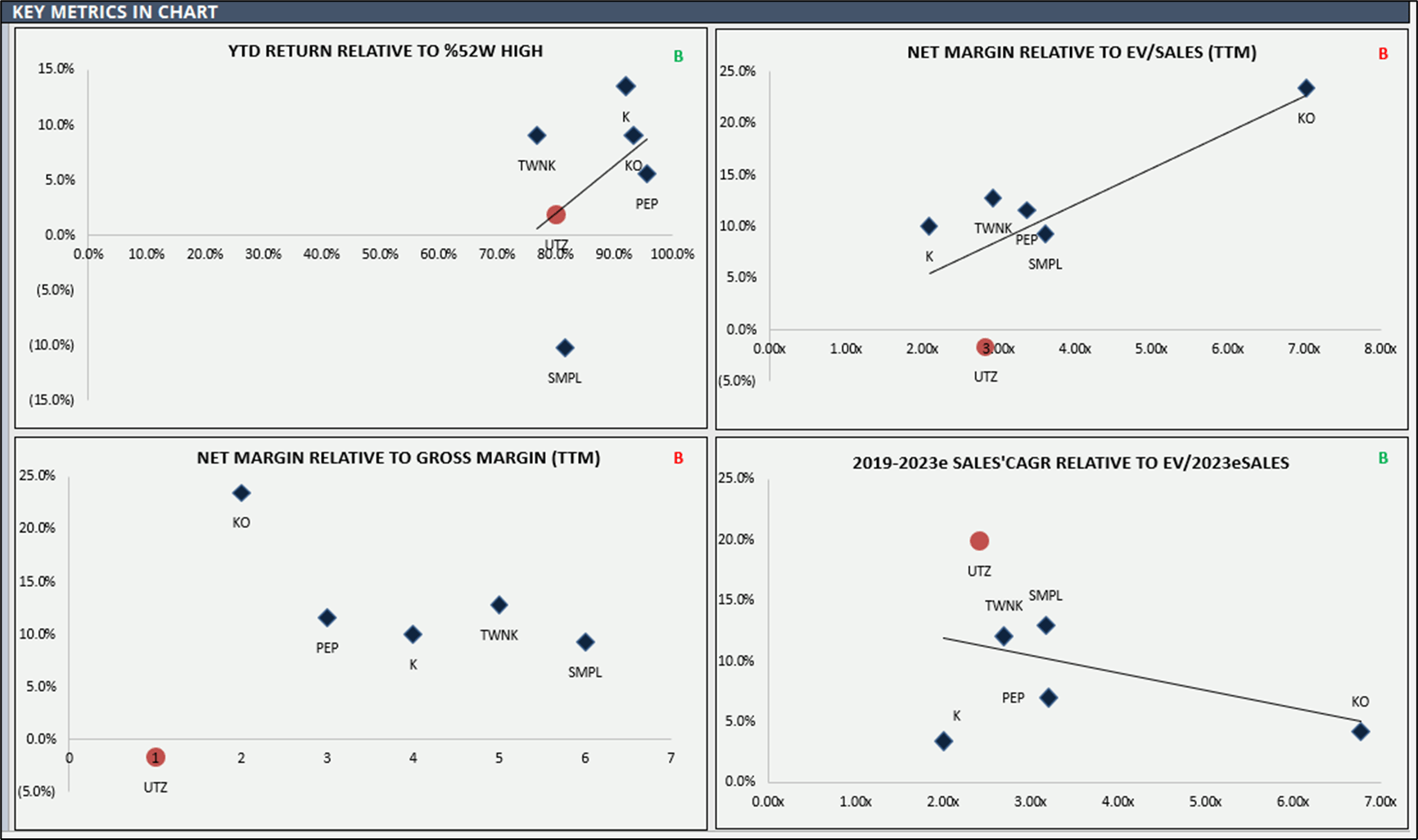

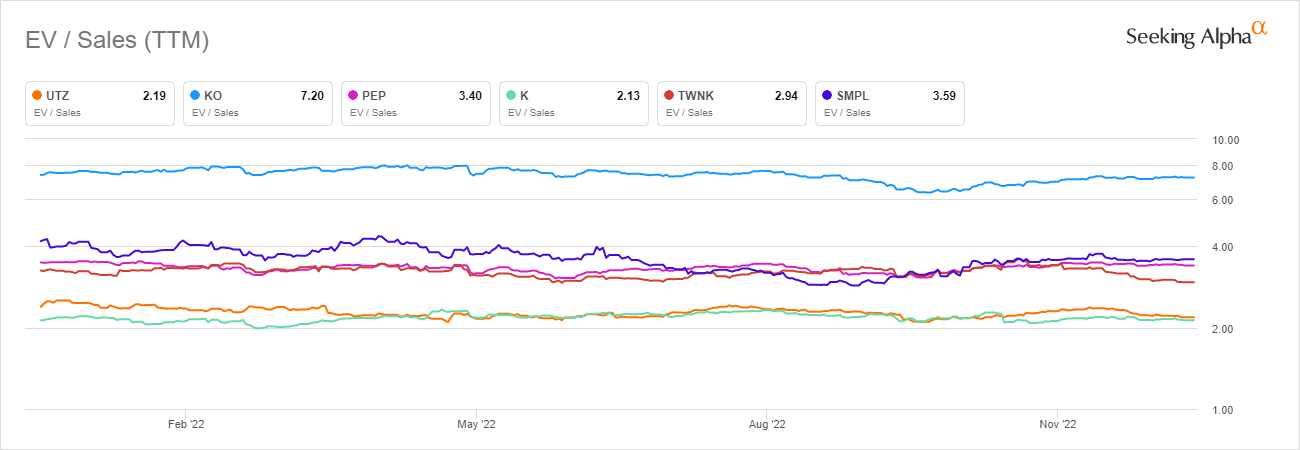

Valuation

The company is trading at an EV/SALES of ~ 2.83x TTM, which represents a discount relative to the peer’s median EV/SALES of ~ 3.15x TTM.

Author’s Estimates

I believe that the company is undervalued, but with a big caveat that investors must be aware of.

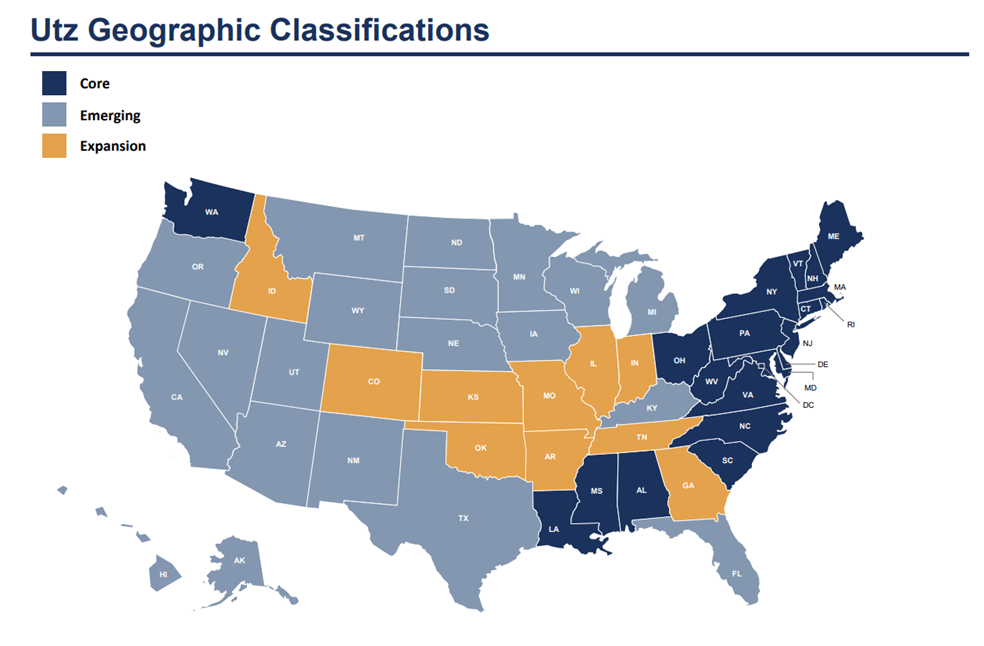

First, as I said before Utz Brands is mostly a regional story, in particular a Northeast story, where it is well-recognized and loved by its customers. However, it is not well known to people from other regions. This offers tremendous opportunities for growth, and the company is well aware of it. In fact, it keeps up investing in the critical supply chain to support geographic expansion nationally. In other words, it is trying to replicate something that is already working in the Northeast, also in the Midwest, West, and South.

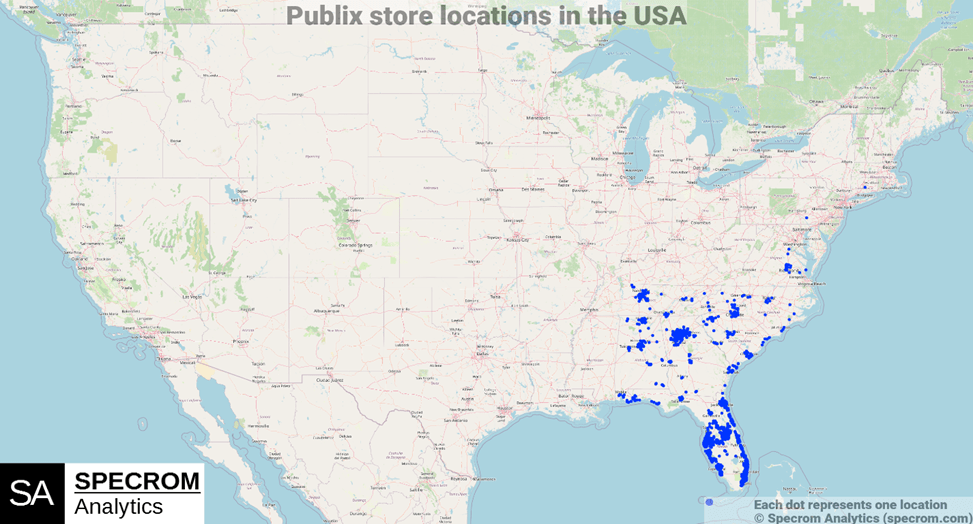

Below, you can see the UTZ geographic presence.

Utz 3Q22 Earnings Presentation

Personally, I believe that the company is on track, as it recently announced the debut of its portfolio of products across nearly 1300 Publix stores. This debut is very important to strengthen its position in the South, in particular in Florida, thanks to Publix store distributions in the USA.

Specrom Analytics

However, the opportunity to participate in this tremendous growth comes at a cost, as represented by debt. In fact, at the end of 3Q22, net debt was 5x normalized adjusted EBITDA. High leverage during good times is viewed as something positive, but during an economic downturn, the trade-off is a potential bankruptcy. Roughly 90% of total interest-bearing debt is represented by Loan B, with expiration on 01/01/2028 and with a variable leg (3.0% + LIBOR).

Our weighted average interest rate for the thirty-nine weeks ended October 2, 2022 was 4.3%, up from 3.5% during the thirty-nine weeks ended October 3, 2021. We have used interest rate swaps to help manage some of our exposure to interest rate changes, which can drive cash flow variability related to our debt

The company is well-aware of having a high debt level (above the company’s target of 3.5x Net debt/EBITDA) but still, it keeps ignoring it. I do believe they will take action in 2023, but I don’t think they will do much as they are likely to focus more on M&A. Overall, I do see an issue here, however, I also believe that the FED won’t keep the policy rate at a high level for a prolonged period of time and in my opinion, it will start cutting interest rate in 4Q23.

Overall, I do see many good reasons that make me willing to invest in this company. In fact, I believe that the company can increase its earnings in two ways: first, by expanding its presence in the U.S.; second, by selling more and by improving efficiency in existing markets.

Having said that, I expect the company to maintain the current valuation of EV/SALES of ~ 2.82x.

Author’s Estimates SeekingAlpha.com

Investment Risks

In terms of downside risks, here are a few:

- Competition, If the competition will be perceived as being a key driver of slower growth, it would negatively affect the company’s share price. Having said that and reading the past company’s earnings call, the street seems to be mostly concerned with the competition from private labels, which at the moment, in my opinion, doesn’t represent a threat due to the price of private label products (which, on average, are pricier than those of UTZ Brands).

- Leverage, a high level of debt increases the bankruptcy risk, especially in a scenario of an economic downturn, and it makes raising additional capital through debt more challenging which means that the burden may shift onto shareholders’ shoulders.

- Expansion, the 2023E growth assumptions are mostly based on the company’s ability to effectively penetrate in the South region.

Final Remarks

I rate shares as Buy with an estimated fair value of $23.88/share, which would represent a 47.4% upside from the current price of $16.20.

Having said that, even if I do believe in the growth potential, I am waiting on the sidelines as I do expect the overall market to go lower in the 1Q22. Overall, for a risk-tolerant investor, this may represent an interesting opportunity to keep on the radar.

Be the first to comment