Justin Paget/DigitalVision via Getty Images

June 24th of 2022 proved to be a remarkable day for shareholders of USA Truck (NASDAQ:USAK). In response to news that the company had agreed to sell itself to another buyer, shares of the entity skyrocketed by 112.6%. This surge in price takes the company to a level that is more or less in line with what many of its competitors are trading for. But on an absolute basis, shares do still look rather cheap. In all, investors should view this as a mildly disappointing outcome, even though they are capturing significant upside in a short timeframe.

A great little business got snatched up

Back in September of last year, I wrote my first article about USA Truck. In that article, I mentioned management’s high expectations for the company and the low price at which shares were trading. By low price, I don’t just mean the nominal price. I mean the multiple the company was trading for relative to its cash flows. In addition to this, I also lauded the company’s historical financial performance, particularly its revenue growth and its robust and generally growing cash flows. At the end of the day, I ended up rating the business a ‘buy’, underscoring my belief that the company would likely generate a return that is materially greater than what the broader market would over an extended timeframe. Since the publication of that article, USA Truck has drastically outperformed even my own expectations. Even as the S&P 500 is down by 17%, shares of the enterprise were up by 0.4% prior to news of this development breaking. Now, they are up by 109.6% compared to the 13.7% decline experienced by the broader market.

The vast majority of this increase is a result of the aforementioned acquisition. According to a press release issued by management, the company has agreed to sell itself to logistics giant DB Schenker in an all-cash deal valuing the company at $31.72 per share. This translates to a market value on the company’s equity of roughly $285.7 million and an enterprise value of $435 million. Although this represents a significant premium over the company’s prior share price, investors would be right to question whether the terms of the deal makes sense for them. In addition, the question of additional upside between now and the date of closing is certainly reasonable. To answer the first question, we first need to dig into the company’s historical financial performance.

Author – SEC EDGAR Data

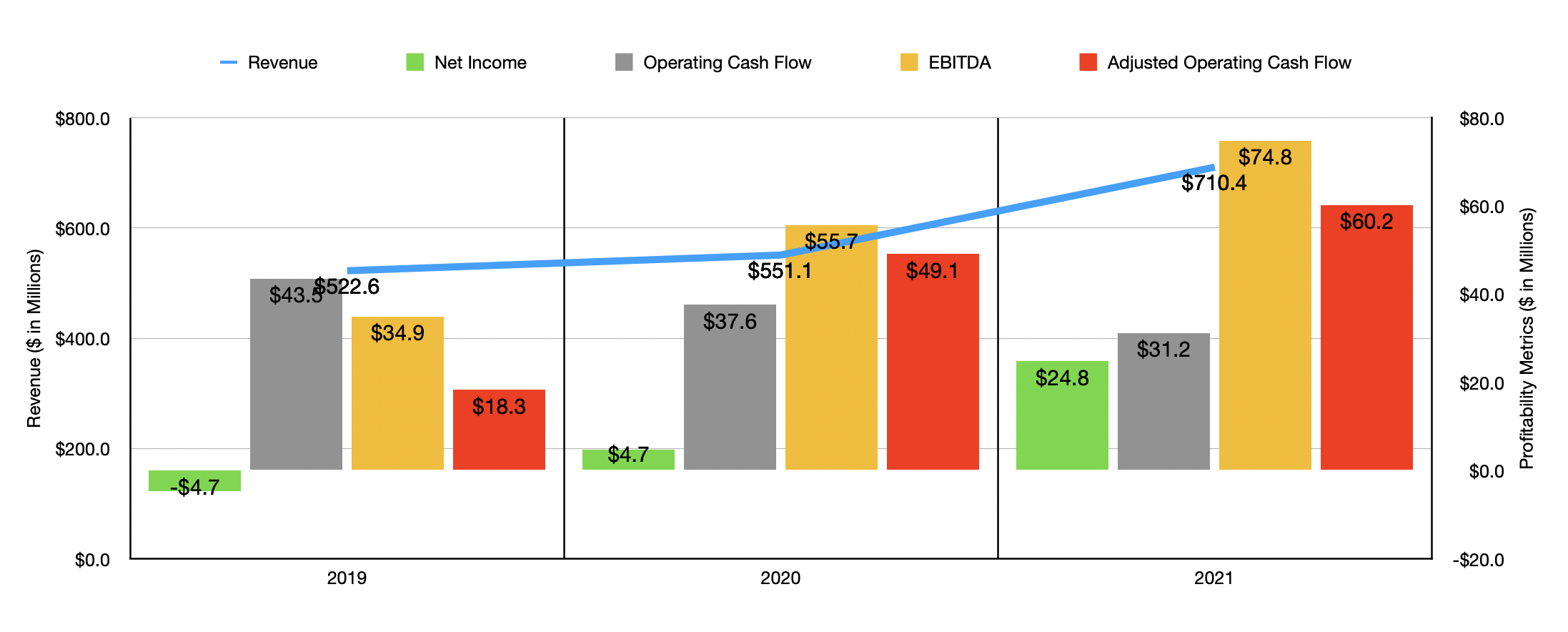

When I last wrote about the firm, we only had data covering through the first half of the company’s 2021 fiscal year. Now, we know how 2021 worked out. We also have data covering the first quarter of the company’s 2022 fiscal year. For 2021 as a whole, revenue came in at $710.4 million. That represents an increase of 28.9% compared to the $551.1 million generated in 2020. One significant contributor to this rise in sales was the Trucking segment, which saw revenue climb by 14.8% from $384.3 million in 2020 to $441.1 million last year. Even though the total miles driven by the company decreased by 7.9%, base revenue per loaded mile grew by 20.7% and base revenue per available tractor per week jumped by 18.4%. Even more impressive was the performance of the USAT Logistics segment, which saw revenue rise by 68.5% from $192 million to $323.4 million in the course of just a single year. This was driven in part by a 17.5% rise in load count. However, the larger contributor was a 43.4% increase in revenue per load. Supply chain constraints clearly have proven beneficial for shareholders recently.

As revenue increased, so too did profitability. Net income of $24.8 million dwarfed the $4.7 million generated in 2020. Operating cash flow went from $31.2 million down to $37.6 million. But if we adjust for changes in working capital, it would have risen from $49.1 million to $60.2 million. Meanwhile, EBITDA for the company also improved, climbing from $55.7 million in 2020 to $74.8 million in 2021. Though these increases may seem disproportionate to the rise in revenue, this shouldn’t be much of a surprise for investors who are used to buying into asset-intensive companies in low-margin industries. Even a small improvement in pricing or volume can have a material impact in a firm’s bottom line.

Author – SEC EDGAR Data

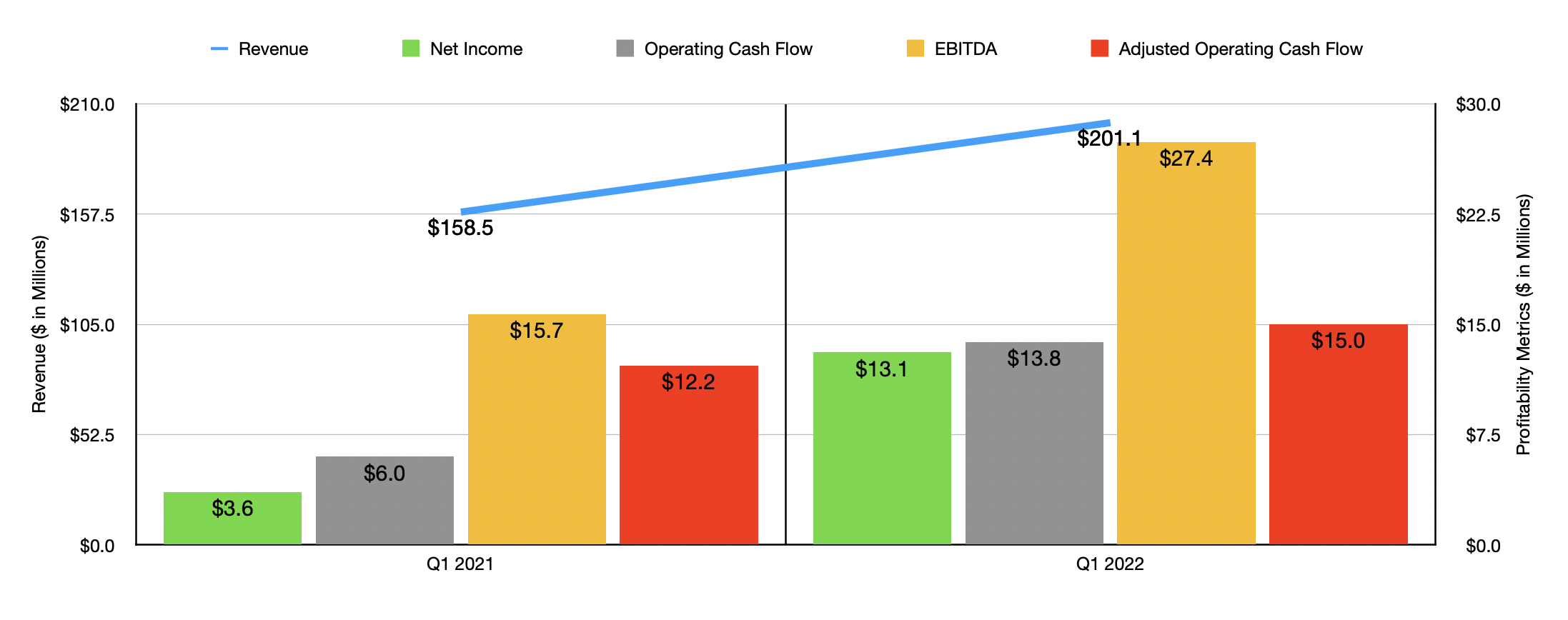

Strong financial performance continued into the 2022 fiscal year. During the first quarter, revenue for the company came in at $201.1 million. That translates to a 26.9% increase over the $158.5 million generated the same quarter one year earlier. Both segments reported year-over-year growth in sales, but the best performing segment by far was USAT Logistics, with revenue climbing 52.6% from $55.7 million to $85 million. Load count for that segment shut up 24.8%, while revenue per load grew by 14.2%. Naturally, profitability followed suit. Net income rose from $3.6 million in the first quarter of 2021 to $13.1 million the same time this year. Operating cash flow more than doubled from $6 million to $13.8 million. However, if we adjust for changes in working capital, the increase would have been smaller, with the metric rising from $12.2 million to $15 million. And finally, EBITDA for the company increased from $15.7 million to $27.4 million.

Author – SEC EDGAR Data

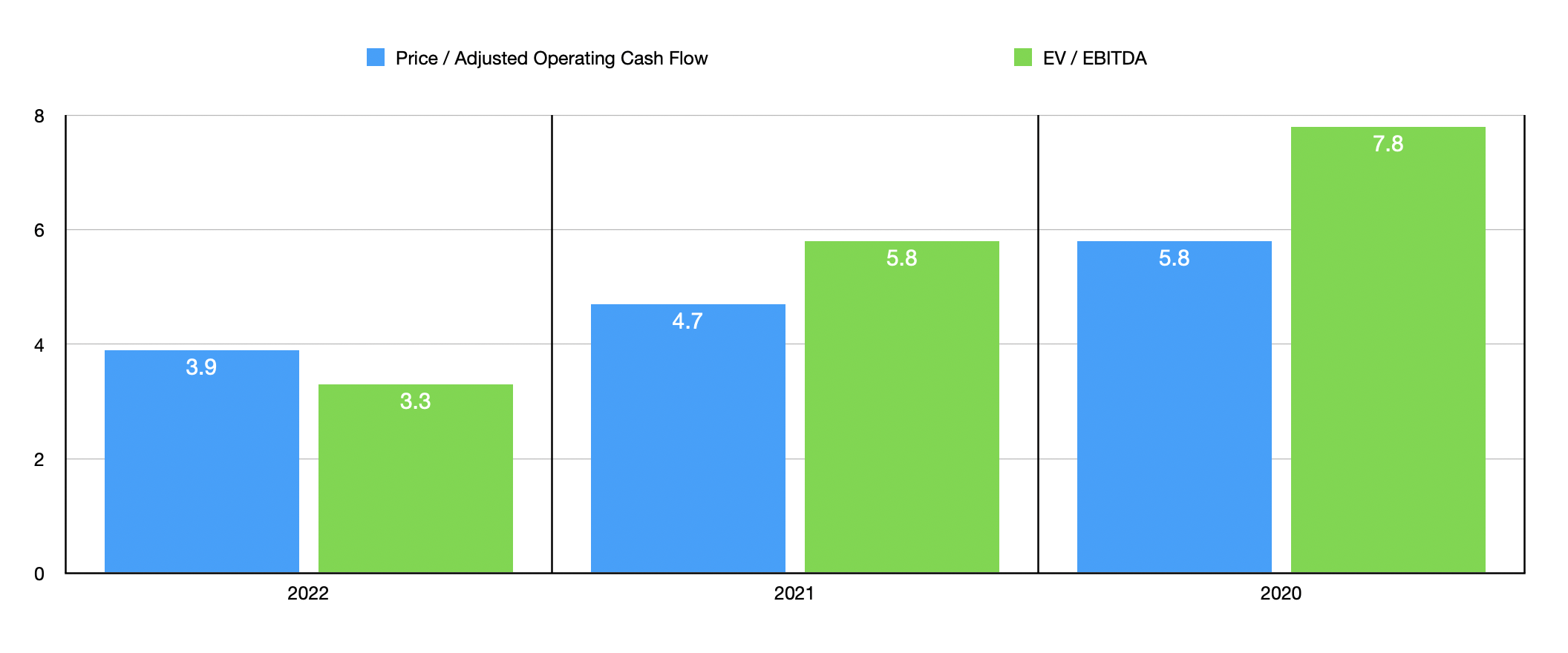

We don’t know what the rest of the 2022 fiscal year will look like for USA Truck, but if we annualize results seen so far this year, we should anticipate operating cash flow of $74 million on an adjusted basis and EBITDA of $130.5 million. Using this data, we can easily value the business. On a forward basis, the price to adjusted operating cash flow multiple is 3.9. This compares to the 4.7 reading that we get if we rely on 2021 results. Meanwhile, the EV to EBITDA multiple should come in at 3.3, which is a material improvement over the 5.8 reading that we get using 2021 figures. Of course, some investors may think that we are being too optimistic by assuming that current market conditions will continue in perpetuity. This is a perfectly fair point. But even if financial performance reverts back to what we saw in 2020, these multiples are incredibly low at 5.8 and 7.8, respectively. Shares of the company are also cheap relative to other players. Relative to five other similar companies, I found that the firms traded at a price to operating cash flow multiple of between 1.8 and 8.5. In this case, three of the five companies are currently cheaper than USA Truck. Using the EV to EBITDA approach, the range was from 2.5 to 5.9. In this scenario, four of the five companies are cheaper than our prospect.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| USA Truck | 4.7 | 5.8 |

| Ryder System (R) | 1.8 | 3.6 |

| Daseke (DSKE) | 3.0 | 4.0 |

| TFI International (TFII) | 8.5 | 5.9 |

| Covenant Logistics Group (CVLG) | 3.7 | 2.5 |

| P.A.M. Transportation Services (PTSI) | 5.2 | 4.0 |

Takeaway

At first glance, this buyout looks incredibly attractive for investors. This is especially true when you consider how shares of USA Truck are priced relative to similar players. At the same time, however, shares are still cheap on an absolute basis, even if financial performance reverts back to what it was in prior years. Given the current share price of the company relative to the stated buyout price, there is some additional upside of about 2.3% to be had. For investors who like merger arbitrage opportunities, this might be worth snatching up, especially if it can be done with leverage and if investors are anticipating further downside for the broader market. Because of this, I would still rate the business a soft ‘buy’, but absent something significant changing, all of the easy money has been made.

Be the first to comment