(Note: This report was originally published to my marketplace service – The Quantamental Investor – on 11th November 2022. The note has been updated to reflect market action up to last Friday’s session.)

Introduction

When I started writing this article, Upstart (NASDAQ:UPST) was trading at ~$14 and change, but after a cool ~50%+ bounce off of its lows over the last two sessions, it is now sitting at the pre-earnings level of ~$20-22. As an investor in Upstart, I am happy to see a bounce; however, the driver of this move is unsettling. After its Q3 ER report, Upstart was down ~25% but then went on to close Wednesday’s session at $17, down by just about ~10%. On Thursday, we got a cooler inflation print, with CPI coming in at 7.7% (vs. expectation of 7.9%), and this data led to a wild upswing in equities. The QQQ ETF (QQQ) jumped up ~7.4%, and Upstart closed the day 27% higher. On Friday, the rally in equities continued, with Upstart rising another 4%.

In this note, we will assess Upstart’s Q3 results and take a look at the long-term vision and strategy of the company. Lastly, we will round out this note with a brief exercise on valuations. Without further ado, let’s get started.

Another Shocking Report & Guide

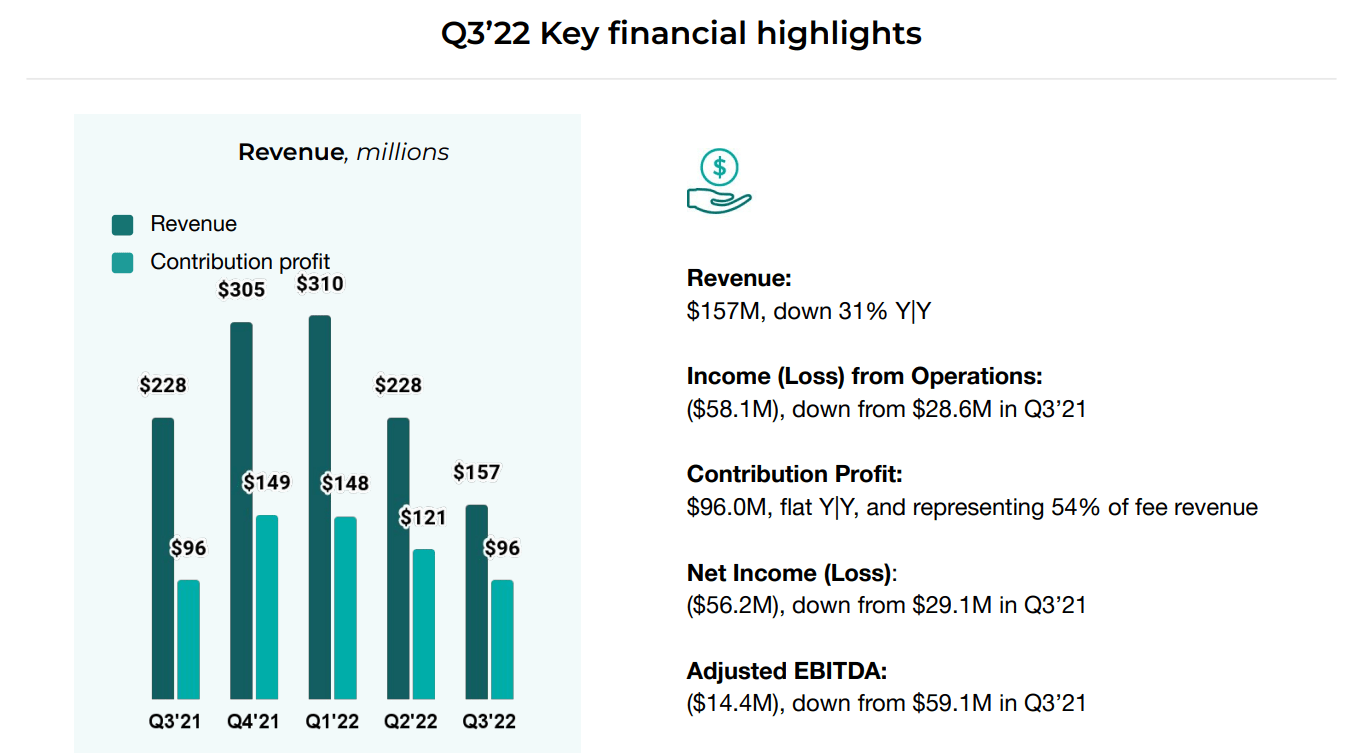

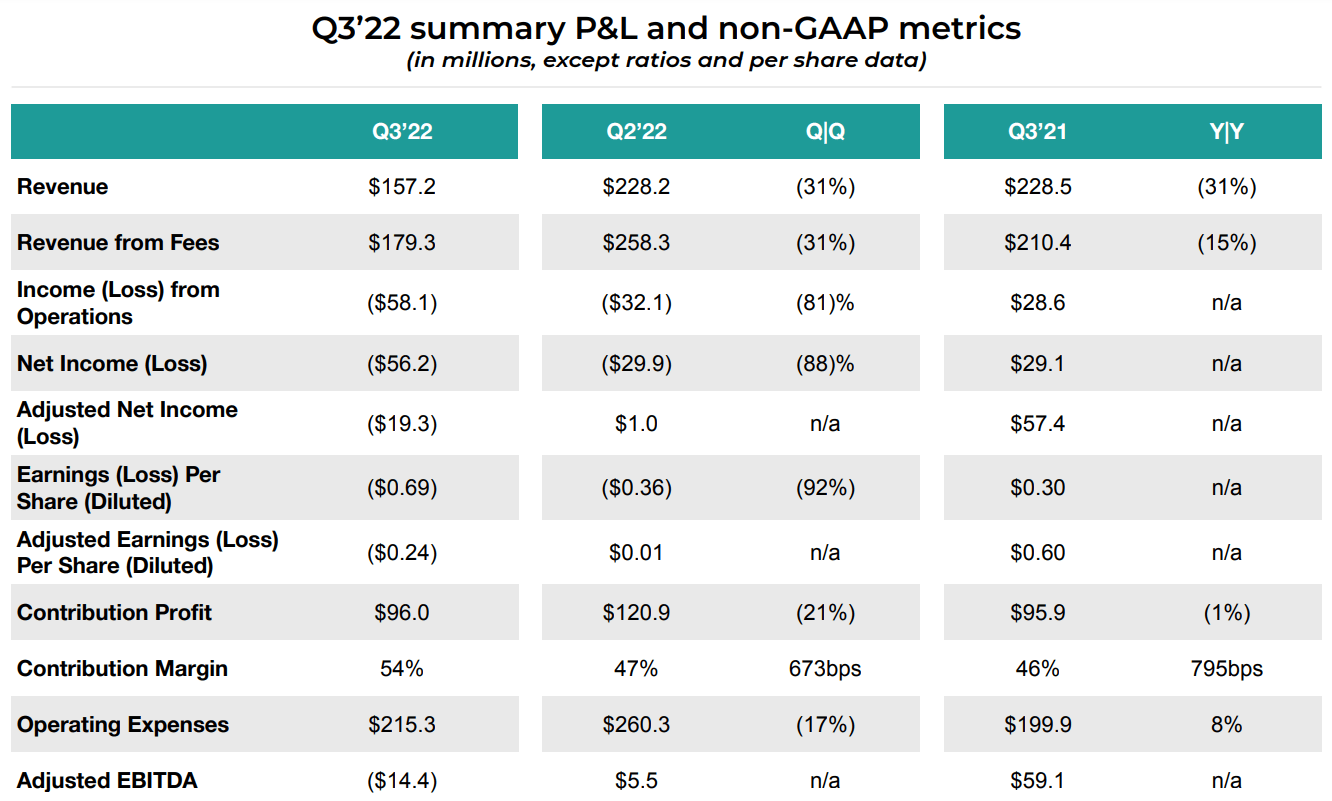

For Q3, Upstart once again missed management’s revenue guidance of $170M, with net revenue coming in at $157M (down 31% y/y). Furthermore, Upstart’s contribution margin came in at 54%, 540 bps below management’s guidance. As volumes and contribution margins fell short of expectations, Upstart’s bottom line performance tanked too. In Q3, Upstart’s adj. EBITDA came in at -$14.4M (missing the outlook of $0 [breakeven]), and net losses widened to -$56.2M. In a nutshell, Upstart’s Q3 report was plain bad.

Upstart Q3 2022 Earnings Presentation

Upstart Q3 2022 Earnings Presentation

While Upstart’s quarter was terrible, I don’t think it was surprising at all. After analyzing quarterly reports from LendingClub (LC) and SoFi Technologies (SOFI), I wrote the following –

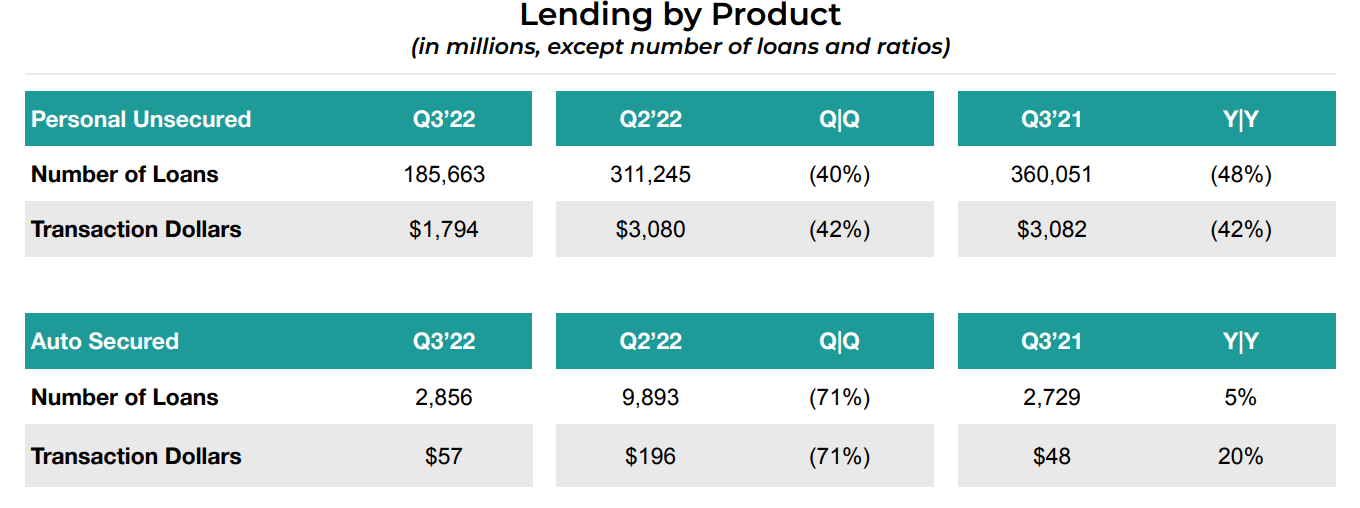

The primary driver of Upstart’s vicious volume contraction is the poor macroeconomic environment we find ourselves in today. Due to the Fed aggressively tightening monetary policy, the probability of a recession is rising. And this is alienating Upstart’s bank and credit union partners from unsecured personal lending (Upstart’s core business at this time). In response to rising interest rates, Upstart is pricing loans at ~800 bps higher than last year. And such a massive move is driving a sharp decline in conversion rates as borrowers reject such pricey loans. On the earnings call, Upstart’s CFO, Sanjay Datta, talked about an ebb and flow between funding constraints and borrower demand. So far, we were in the know about funding constraints, but now the other side of Upstart’s marketplace is hurting too.

Upstart Q3 2022 Earnings Presentation

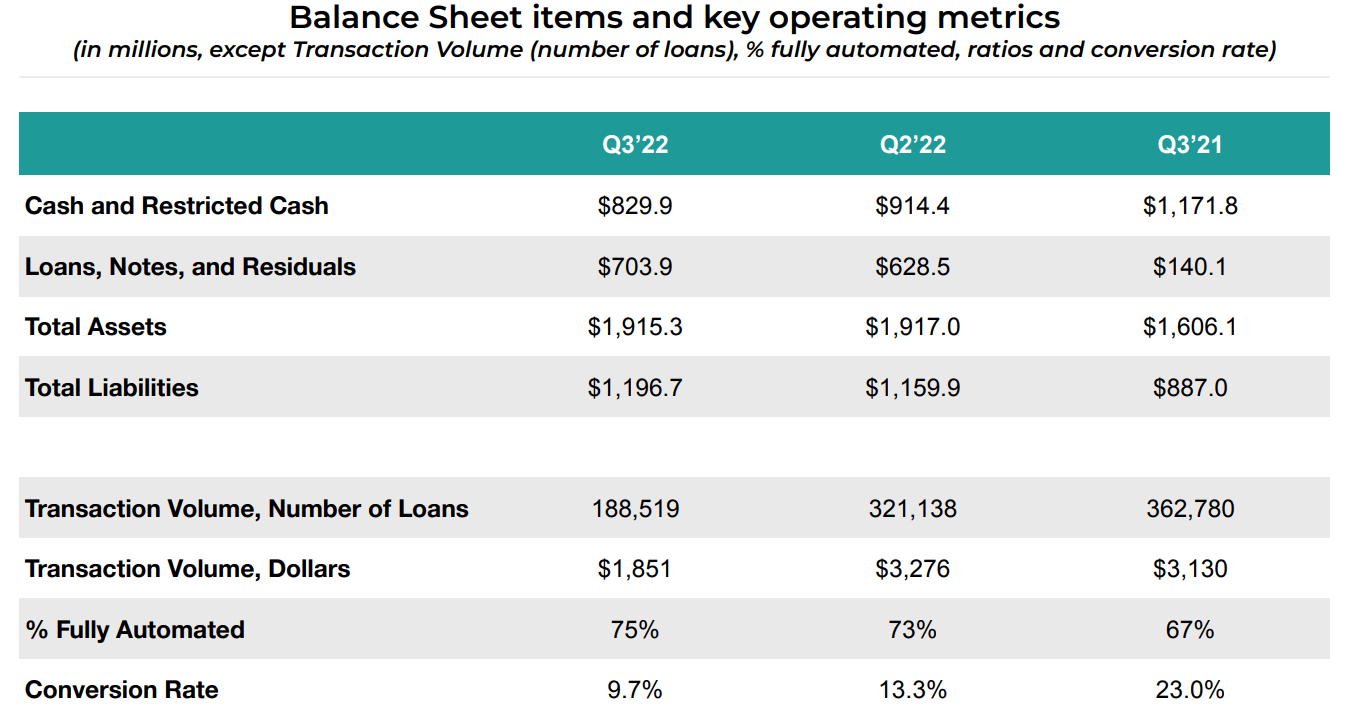

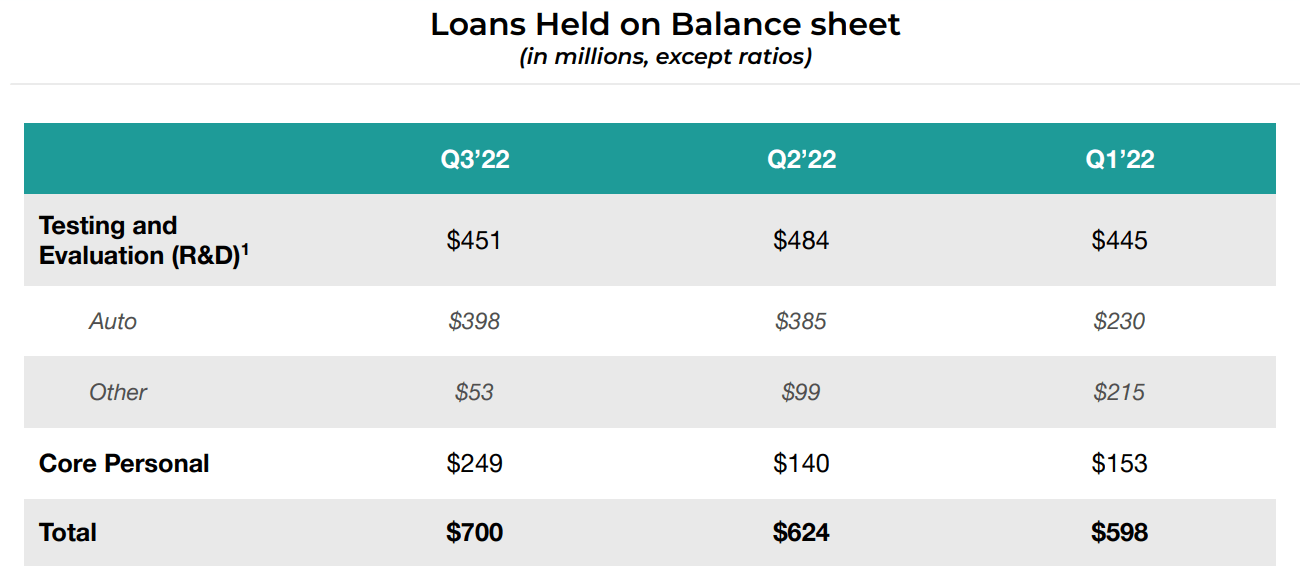

Furthermore, investor appetite for unsecured loans is just not there, as evidenced by reports from SoFi, LendingClub, and now Upstart. As interest rates stabilize (even at higher levels), credit markets should unfreeze, and in that context, the Fed potentially slowing its rate hikes is a positive development for Upstart. In the meanwhile, Upstart is still using its balance sheet as a bridge to enable loan originations. The impact of this activity is a pile-up of loans on Upstart’s balance sheet. As of Q3, Upstart is holding ~$700M of loans, of which $250M are unsecured personal loans, and the rest are R&D loans (auto, auto refinance, etc.). In the past, I projected Upstart’s loan holdings to grow to $1B by the end of 2022; however, this figure now seems unlikely, and ~$800M would be a far more suitable estimate.

Upstart Q3 2022 Earnings Presentation

Upstart Q3 2022 Earnings Presentation

As lending activity has slowed on its marketplace, Upstart has chosen to increase its take rate and reduce marketing expenses to boost contribution margins. However, Upstart’s report clearly showed that these moves from Dave and Co. failed to match the CM guide for Q3 and led to a sharper-than-expected drop in lending volumes. The macroeconomic environment is not ripe for Upstart’s business model, which looks broken at this moment in time. Now, Upstart’s CEO, Dave Girouard, had the audacity to term this ongoing lending volume contraction as a “feature” of Upstart’s business model, and I think Dave is sticking with Upstart’s marketplace vision, despite the business model being hinged on the credit cycle, i.e., exposed to severe volume contractions.

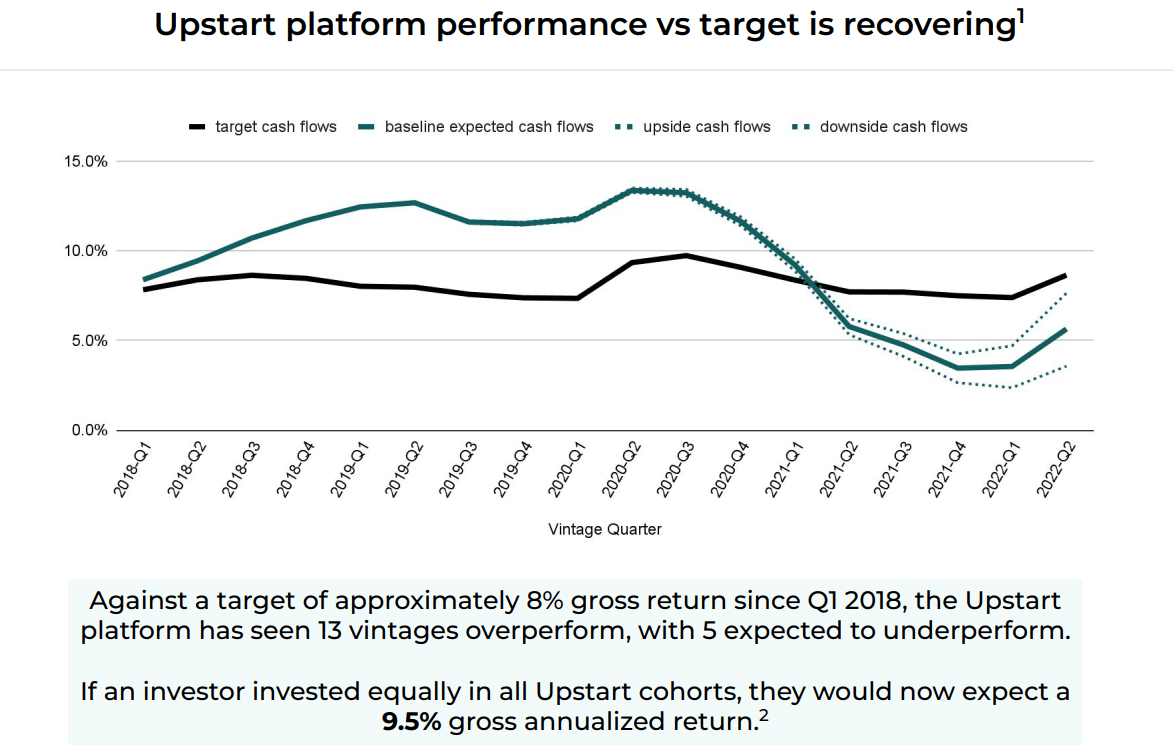

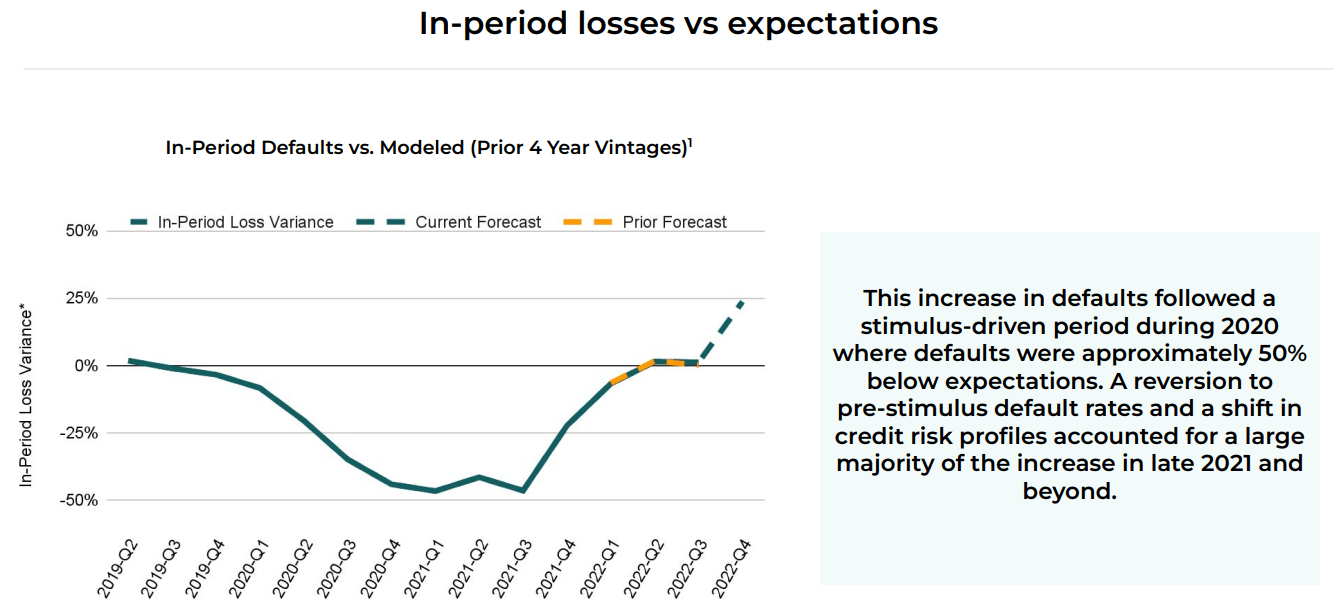

While it is easy for bulls to dismiss Upstart’s weakness as a macro problem, I think Upstart’s failure to deliver on target cash flows is troubling. Coming out of the pandemic, Upstart’s lending activity rebounded spectacularly and kept on growing like wildfire as credit investors gulped up Upstart’s loans. Prior to 2020, Upstart’s loans had been outperforming target returns magnificently, and then in-period default rates came in 50% below modeled default rates for almost a year due to stimulus payments and a robust economic rebound.

Upstart Q3 2022 Earnings Presentation

As a consequence, Upstart’s lending volumes jumped up, and that brought about a shift in credit risk profiles from near-prime towards non-prime and sub-prime borrowers. With inflation causing havoc, people with these riskier credit profiles have been hurt lopsidedly, and this has led to higher default rates at Upstart, which are now back to the pre-stimulus period (and heading higher). Due to higher-than-expected default rates, all of Upstart’s loan cohorts since Q2 2021 are now projected to deliver gross returns well below target returns. While the management has tried to spin these results as much as they can and pointed to the average performance of vintages from 2018, Upstart’s investors have been burnt to an extent.

Upstart Q3 2022 Earnings Presentation

For Q4 2022, Upstart is forecasting in-period defaults to come in 25% above their modeled defaults. And while this is bad, overall gross returns for Upstart’s loans are set to improve as Upstart is now charging far greater APYs to borrowers on new loans. From this data, one can conclude that Upstart’s AI models failed to price risk appropriately during an era of free money (zero interest rates), and it is now paying the price in the form of low investor demand. Yes, the macro is playing a big part here, but Upstart’s AI model could have and probably should have done a better job here.

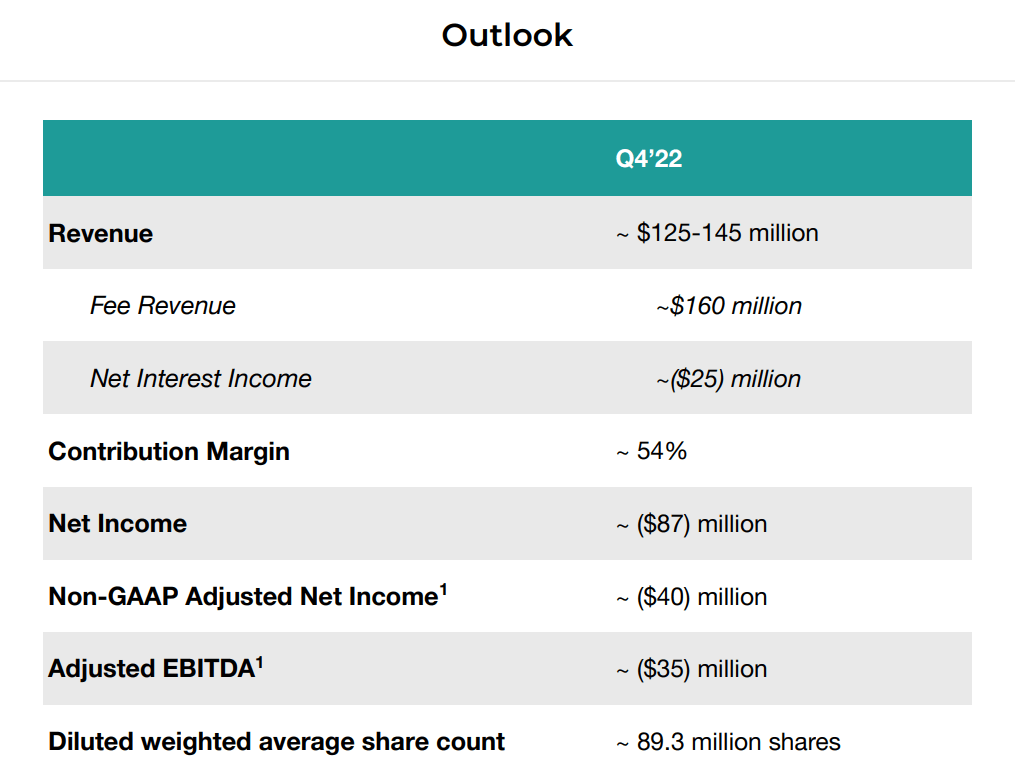

The macroeconomic environment could be set to worsen over the coming months as the lagged impact of the Fed’s aggressive tightening measures shows up in the real economy. As such, Upstart’s lending volume contraction is set to continue in Q4, with management guiding for revenues of just ~$125-145M. I say “just” because street expectations for Upstart’s Q4 revenues were ~$186M before the Q3 report came out.

Upstart Q3 2022 Earnings Presentation

Furthermore, Upstart’s losses are set to grow wider, along with a significant drop in adj. EBITDA to -$35M. Upstart is now a cash-burning business; however, with a cash balance of ~$700M (and loans of $700M), Upstart has little to no bankruptcy risk for the foreseeable future. FYI, the cash burn (represented by adj. net income) as of Q3 was ~$20M, and the guide for Q4 was ~$40M. Until credit markets unfreeze, Upstart’s cash flows could remain under pressure, and they could even worsen further in case of a (very likely) recession.

Without mincing any words, I want to admit that Upstart is screwed right now. The marketplace model simply doesn’t work in recessionary periods, and Upstart continues to remain exposed to severe volume contractions. While the near-term business outlook remains poor, Upstart is a long-term investment for us. So, let’s take a long-term view of the business.

Looking To The Future

From a strategic viewpoint, I think Upstart’s management finally provided us with some much-needed clarity on how they are going to run this business in the long term. After months of vacillating between being a marketplace, using its balance sheet as a bridge, and getting a committed source of funding – Upstart’s CEO, Dave Girouard, has chosen to stick with their initial vision of building a marketplace where thousands of banks & credit unions are on one side of the platform and millions of borrowers on the other side. He explicitly termed the current contraction in lending volumes as a “feature” of Upstart’s platform and added that this marketplace model would get Upstart to the scale (and profitability) no other fintechs have achieved.

Here’s what Dave said on the call about Upstart’s marketplace vision –

We don’t like volatility any more than you do, but we won’t allow it to set us off course from our long-term goal to reinvent how credit works. Our goal is to become the destination with the best rates and the best process for all forms of credit for everyone. This can’t and won’t be done by a single bank, but it can be done by a vast network of banks, credit unions and credit investors powered by a modern cloud-based AI platform.

Great companies separate themselves from merely good ones during the hardest of times. They are clear-eyed about how the environment has changed. They make smart and fast decisions in order to ride out the turbulence, but they also retain an optimistic focus on the horizon as they continue to invest in the future. You have my full commitment to ensure Upstart is exactly that type of company.

We certainly think about funding on our platform pretty much constantly. But I will say this, we believe fundamentally in a marketplace structure in the sense that a lot of lenders making independent decisions over the long haul is going to get to the right answer. I mean marketplace — market-based economies are historically far more efficient than centrally planned economies. That’s a very — I would just say a very basic truism.

But having said that — so that means we don’t want to become a centrally planned economy. We don’t believe us being a bank makes a lot of sense for what we hope to pursue for lots of reasons. But having said that, we can certainly do a better job of securing supply of funding on our platform. And that can really be through some of the things we talked about getting longer-term funding agreements in place; being in more products — a more diverse set of products, such as secured products like auto loans, mortgages, et cetera.

So it is certainly something we have to think hard about and do more work on. But underneath it all, we do believe a market-based economy — a marketplace where there’s a lot of participants on both sides will ultimately have the greatest scale and the greatest opportunity. Albeit we’re dealing with volatility today, but over the long haul, we’re confident this will lead to the greatest outcome for Upstart.

This was a clear signal that Upstart is going to be a cyclical platform business, and the management is looking to reduce revenue volatility by moving into secured lending markets like auto and mortgage. Getting committed funding on board is something they would like to do, but taking on such funding is fundamentally misaligned with Upstart’s marketplace vision.

Back in July, I laid out my investment thesis for Upstart and summarized it –

Debt markets are cyclical, and Upstart’s business is inherently volatile due to its dependence on lending partners. Hence, Upstart investors will need to get accustomed to business volatility and wild swings in its stock. If you are not on board with these sorts of fluctuations, I don’t think Upstart is a suitable investment for you.

Despite Upstart being a tech company, it cannot be valued as one due to the nature of its business. And I have learned this the hard way (losing a lot of money on the stock). As an early-stage investor, I am willing to accept the volatility inherent to Upstart’s business as its disruptive AI-based credit underwriting has the potential to create a paradigm shift in the consumer lending space. With a virtually infinite TAM, Upstart’s management can build a large and profitable business worth tens of billions of dollars.

Upstart Q3 Earnings Presentation

Yes, Upstart’s executives have made some mistakes, but their decision to tighten up the belt and focus on profitability over volumes is the right way to go in the current market environment. I like the fact that Upstart is being managed with a focus on long-term sustainability over short-term stock price fluctuations. Upstart’s management has acted naively in recent months in my opinion, but I think they can get their act together and win investors’ and Wall Street’s trust once again in due time.

Credit is the bedrock of the American economy, and we can be sure that debt markets will come back (as they did after the Great Financial Crisis). Upstart will come back stronger at the other end of this cyclical downturn, and I say so with utmost confidence based on Upstart’s accumulation of new lending partners even during this tumultuous period.

Investors will need to be patient, but a long-term investment from current levels is likely to be rewarded handsomely. Due to the sheer conservatism of my model, I believe that Upstart offers incredible returns from current levels with a spectacular margin of safety.

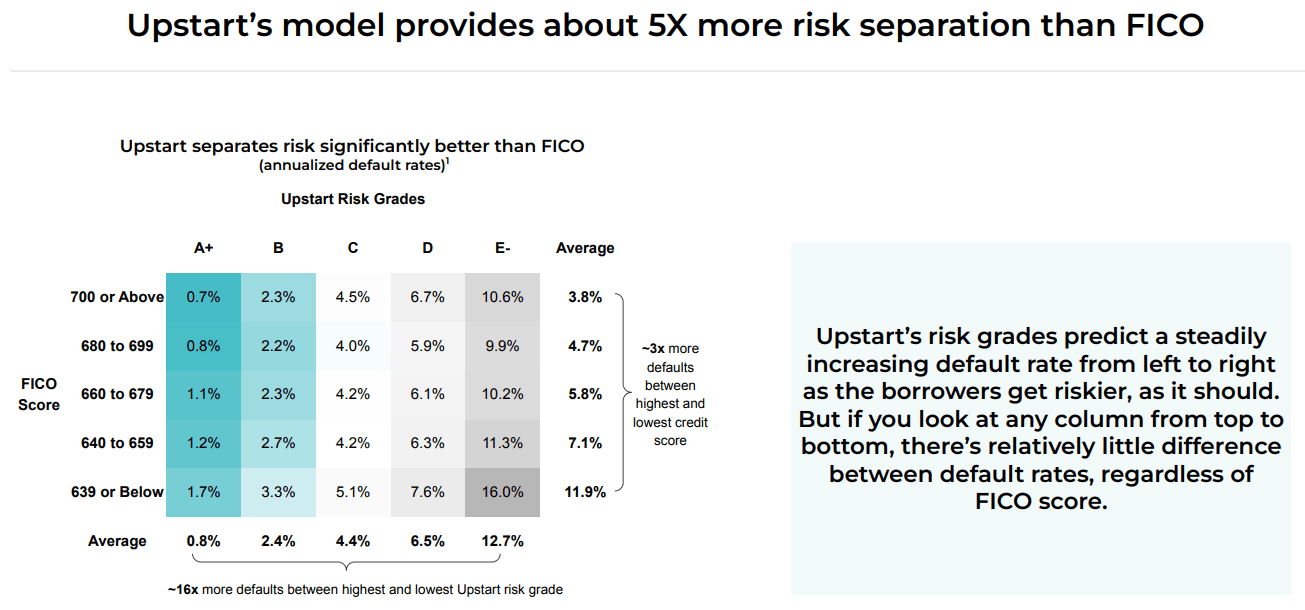

While we are going through a tumultuous economic period, and the pain is not over yet, the credit markets are going to come back at some point. As you know, Upstart’s long-term success depends on its AI’s ability to assess credit risk better than traditional FICO-based lending models. And for now, Upstart’s model is still ~5x better at risk separation than FICO.

Upstart Q3 2022 Earnings Presentation

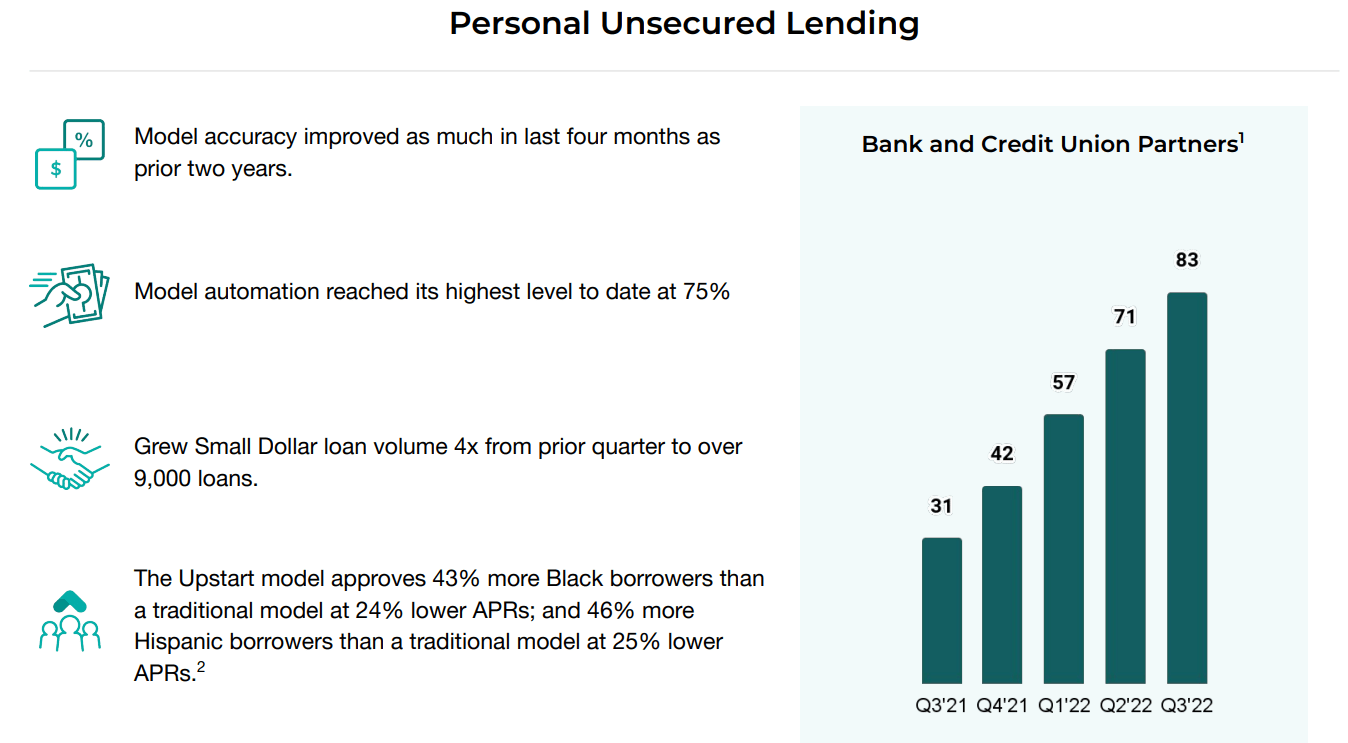

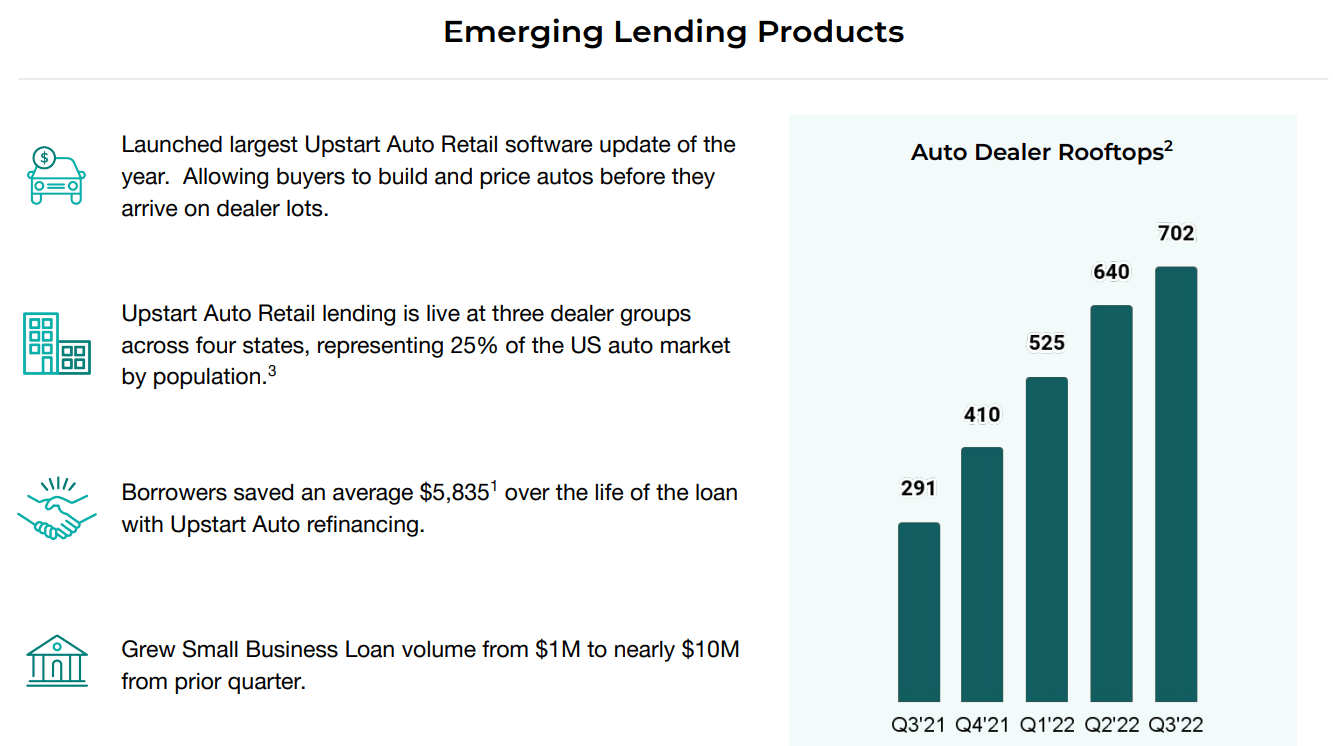

Looking at Upstart’s credit performance, I understand that it is hard to believe that its AI model is any better than FICO. However, the increasing number of bank and credit union partners is a telling sign of some sort of an edge. Despite experiencing a vicious volume contraction, Upstart’s banking partners have risen to 83, and the company is also expanding its presence across auto dealerships quite rapidly. The journey to having thousands of bank partners on its marketplace platform is long, and Upstart’s investors could need to exercise patience for multiple years.

Upstart Q3 2022 Earnings Presentation

Upstart Q3 2022 Earnings Presentation

The Fed pivot is still not forthcoming; however, we are getting closer to terminal rates now, and slower rate hikes represent an easier business environment for Upstart. A downcycle in credit markets is the right time to invest in Upstart as volumes are currently compressed. When we return to an upcycle, Upstart’s volumes will bounce back, and so will its stock. For now, Upstart’s financial performance is crappy, and this will continue over the next couple of quarters; however, the underlying business is getting leaner and stronger. Hence, I continue to like Upstart as a long-term investment.

Valuation

In the face of heightened macroeconomic uncertainty, I don’t know how deep or long the impending recession could turn out to be. Conservatively, I can see Upstart doing $100M in revenue per quarter even if the credit markets get worse from here. That said, a stabilization in interest rates should unfreeze the credit markets to an extent and bring volumes back to Upstart’s marketplace.

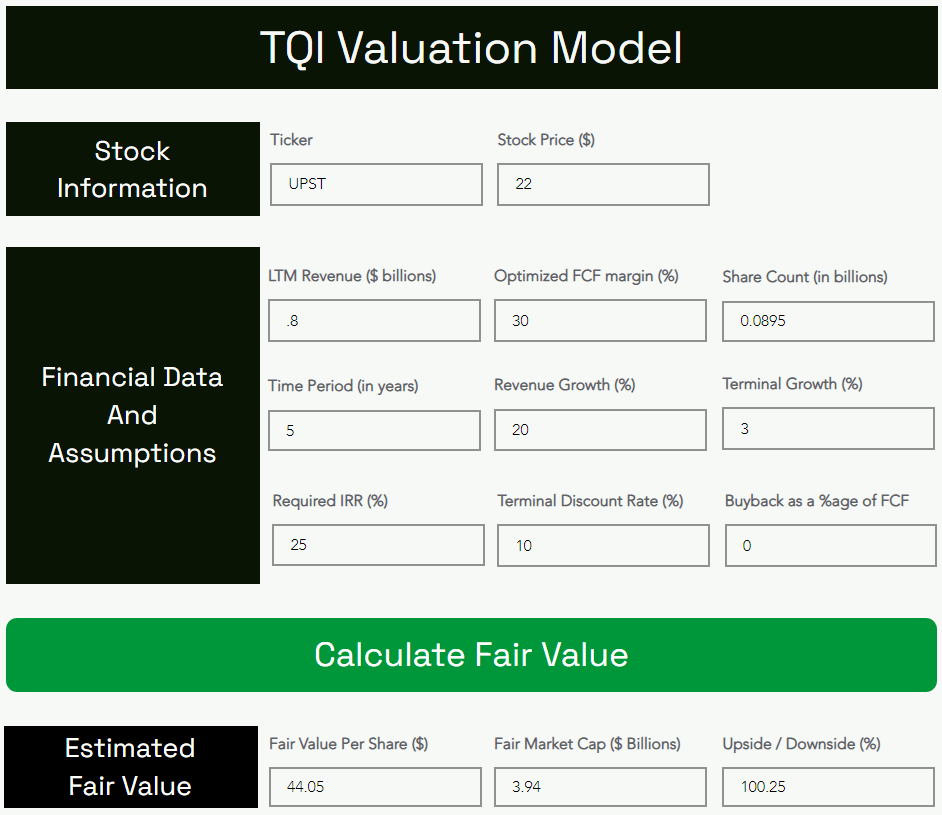

After looking at Upstart’s Q4 revenue guidance, I think we were spot on with our 2022 revenue estimate of ~$800M. While 2023 is a bit of a mystery at this stage, I think a scale-up of Upstart Auto Retail could allow Upstart to return to positive revenue growth in the second half of next year. For today’s valuation exercise, I am holding all the assumptions from my previous analysis, except for buybacks (assuming 0% now) and share count (diluted: 89.5M).

TQI Valuation Model (TQIG.org)

TQI Valuation Model (TQIG.org)

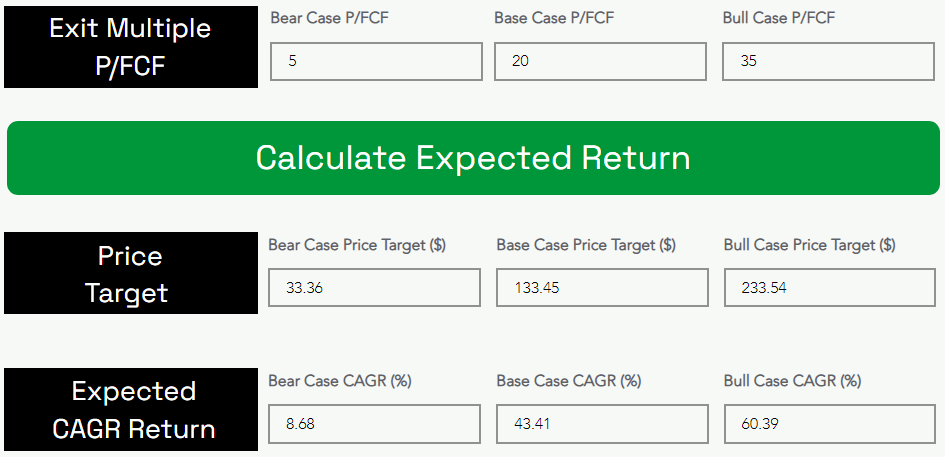

According to these results, Upstart is worth $44 per share. More importantly, I am reducing my 5-yr price target from $171 per share to $133.45 per share (primarily due to a change in assumption for buybacks). The expected CAGR return for Upstart from here is ~43%, which is far greater than my required IRR of 25% for high-risk, moonshot growth bets like Upstart. Hence, I continue to rate Upstart a ‘Strong Buy’ for long-term investors.

Strategic Positioning

Upstart’s stock is cheap; however, if its AI models fail to outperform FICO-based models, Upstart will fail as a business and as a stock. Moreover, Upstart’s revenues are shrinking, and losses are widening. In the current market environment, Upstart is likely to see more selling pressure. Hence, I am staying hedged in this counter. And here’s how I am positioned:

The Quantamental Investor’s Managed Risk Portfolio

Upstart is a high-risk, high-reward bet. The business is clearly struggling in a rising interest rate environment, and the Q3 report turned out to be yet another disappointment. Since we were already expecting a weak quarter, there is no reason to be surprised. Upstart is a long-term investment, and despite its current malaise, we see an uptick in banking partners and auto dealerships as good news. Upstart’s management is sticking to its marketplace vision (unlike LendingClub, which chose to be a bank), and while I commend this conviction, I can’t ignore the fact that Upstart’s marketplace is exposed to credit cycles. Hence, I suggest staying hedged in this counter for now. Also, the stock has rallied ~60% in the last two days, and buying such an impulsive bounce is always risky. If you are looking to buy UPST, be patient and accumulate slowly.

Key Takeaway: I rate Upstart a “Strong Buy” at $22, with an insurance policy (options-based hedge).

Thanks for reading, and happy investing. Please share your thoughts, questions, or concerns in the comments section below.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment