Investor Trying To Figure Out Why He Missed The 400 Signs That Upstart Was A Bubble

Ridofranz

Stabilizing revenues and a return to GAAP profits were the need of the hour for Upstart Holdings, Inc. (NASDAQ:UPST) the last time we wrote on it. Rapidly declining revenues painted a dire picture regarding the demand for the company’s loans. This was the state even before the start of the long anticipated recession.

Ironically the one silver lining we saw was the high short interest. Well, because a short squeeze was always on the card with that. Bottom line, we saw the company having limited time to turn things around.

Upstart is now on the clock and has to turn things around within 1-2 quarters. At a minimum this requires a stabilizing revenues and ideally it will require a return to GAAP profits. If the company does land up as a benefactor of a short squeeze, it should strongly consider a massive stock issuance to buy itself more time to deliver on its promises. This may seem counterintuitive, especially considering that the company bought back stock at far higher prices, but we have to move past that sunk cost. At present we rate the stock as a hold/neutral and don’t think risk reward favors either the bulls or the bears at this juncture.

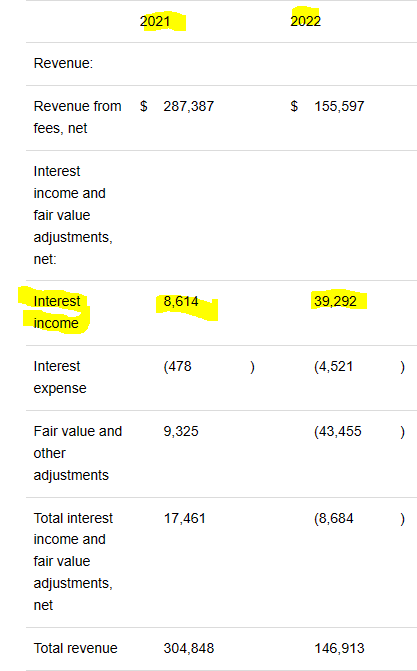

Upstart Holdings, Inc. has reported Q4 results and they did beat the revenue estimates, though we must add here that those had been relentlessly bludgeoned by analysts over the last 3 months. With a revenue base of $146.9 million, the first clear shoutout was to the growth groupies. That shoutout was that there is no growth here.

Year-over-year revenues were down a stunning 52%. We have to add here that all metrics of both real and nominal GDP from different sources continue to show solid growth. So, that 52% revenue drop has happened in the context of an economic expansion. One more point here is that while the Federal Reserve’s interest rate hikes might have burst this massive bubble, it did actually help UPST’s numbers quite a lot. Interest income was up almost $31 million year-over-year.

UPST Q4-2022 Press Release

UPST adjusted EBITDA, which excludes a lot of relevant expenses, was down 45% and to negative $16.6 million from $91.0 million in the same quarter of 2021. We reference back our previous article that losses were about to skyrocket. Looks like we got there way ahead of schedule. UPST stunningly continues their share repurchase policy and spent a valuable $28 million buying 1.4 million shares. Besides being pointless here, Upstart Holdings is wasting very valuable cash that creates an existential issue down the line.

Outlook

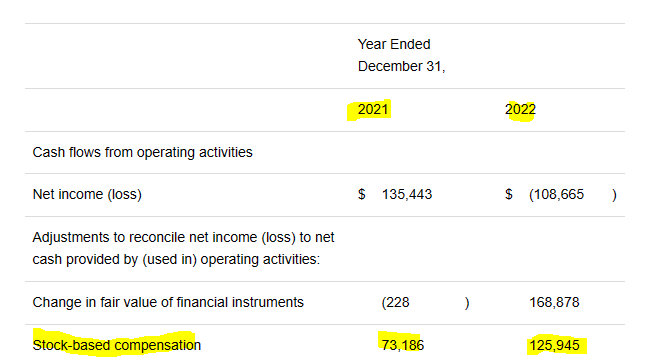

Let’s take a moment to appreciate that Upstart Holdings, Inc.’s stock-based compensation (“SBC”) was the only real “growth” play this quarter.

UPST Q4-2022 Press Release

At a $126 million quarterly run rate, UPST stock-based compensation is now within a micron of the revenue run rate. Not the earnings, the revenue run rate. Of course, that was the last quarter. Q1-2023 should fix that.

Financial Outlook

For the first quarter of 2023, Upstart expects:

Revenue of approximately $100 million

Revenue From Fees of approximately $110 million

Net Interest Income (Loss) of approximately ($10) million

Contribution Margin of approximately 55%

Net Income (Loss) of approximately ($145) million

Adjusted Net Income (Loss) of approximately ($70) million

We always had the opinion that Coinbase Global (COIN) would be the first to breach the barrier where stock based compensation exceeded revenues, but we got that wrong in spades. UPST will wear that crown next quarter. Alongside that, the adjusted EBITDA was negative $45 million. So acceleration of losses continues as UPST downsizes its revenue base. Let’s be clear here, folks, things are extremely grim. When we told you in August 2022, that UPST would miss the 2023 revenue estimates ($1.38 billion at that point) by a mile , the bulls chided us.

We are going to go out on a limb here and say that UPST misses the 2023 revenue estimate number by at least 50%.

UPST just guided to $400 million (annualized run rate), making us look like perpetual optimists. At a $400 million revenue run rate (about half of which will be interest income), they will have to slash non-stock based compensation expenses by about 40% to come close to EBITDA profitability. We are still ignoring the $500 million of stock based compensation which makes the equation worse, even if UPST does make it out on the other side. And that is a realistic question. Analysts were still detached from reality before this report, forecasting revenues of $723 million.

Seeking Alpha

Non-GAAP earnings were forecasted at 14 cents.

Seeking Alpha

The reality here is that EBITDA loss run rates will be $180 million ($45 million annualized). So Non-GAAP earnings are likely to be a loss of over $2.00 a share. That means a huge downgrade cycle starts this evening. Just adding $500 million of stock-based compensation annually on that gives you $680 million on 82 million shares. That gives you a GAAP loss number of over $8.00 a share. This is our base case here. Before you add in the very likely restructuring charges that should be on their way. We think Upstart Holdings, Inc. stock will be in the single digits by the end of the year. Buyer beware.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment