bjdlzx/iStock via Getty Images

Introduction

Kinder Morgan (NYSE:KMI) is a prominent midstream company with a significant focus on natural gas operations, accounting for 62% of its business. The company boasts the largest natural gas transmission network in the United States, spanning over 70 thousand miles. KMI plays a crucial role in transporting 40% of U.S. natural gas production and has a stake in 700 Bcf of working storage capacity, representing 15% of U.S. natural gas storage. I covered the stock here in April, and I am upgrading my rating due to several compelling reasons.

KMI’s Financials

In the first quarter of 2023, Kinder Morgan’s results remained relatively stable compared to the same period in 2022. However, the company did increase its dividend payment by 2% to $0.2825 per share year over year, resulting in a well amount of 6.69% dividend yield. Despite fluctuations in free cash flows, which are common in the oil and gas industry, Kinder Morgan has consistently increased its dividend payment for the past six years. This is a positive sign for investors who are interested in holding onto high-quality value stocks without having to worry about timing their sales.

Also, The CEO recognized that shareholders will gain from their approach of maintaining a robust investment-grade balance sheet, funding expansion opportunities internally, providing an attractive and growing dividend, and further enhancing value by opportunistically repurchasing shares. Along with increasing the dividend this quarter, the company has also repurchased around 6.8 million shares for $113 million at an average price of $16.62 per share. Recent regulations passed by the U.S. Congress have made it more difficult to obtain permits for new natural gas pipelines, which could make the market less favorable for new entrants and benefit existing midstream companies like Kinder Morgan. As a result, they plan to focus on their contracts as their pipelines become more valuable due to reduced competition.

Kinder Morgan has maintained a strong balance sheet and even improved it by passing its targeted net debt-to-Adjusted EBITDA of 4.5x. As of the end of the first quarter of 2023, they had reached a net debt-to-Adjusted EBITDA of 4.1x. The management has ensured the success of KMI by increasing their project backlog by $400 million and expanding their interstate natural gas pipeline projects by $324 million. Their current backlog of projects, totaling $3.3 billion, is expected to generate an average Project EBITDA multiple of approximately 3.5x. It is noteworthy that KIM is dedicating 86% of its project backlog to lower-carbon energy services, including renewable natural gas (RNG) and renewable diesel projects such as a new renewable feedstock storage and logistics hub in Louisiana.

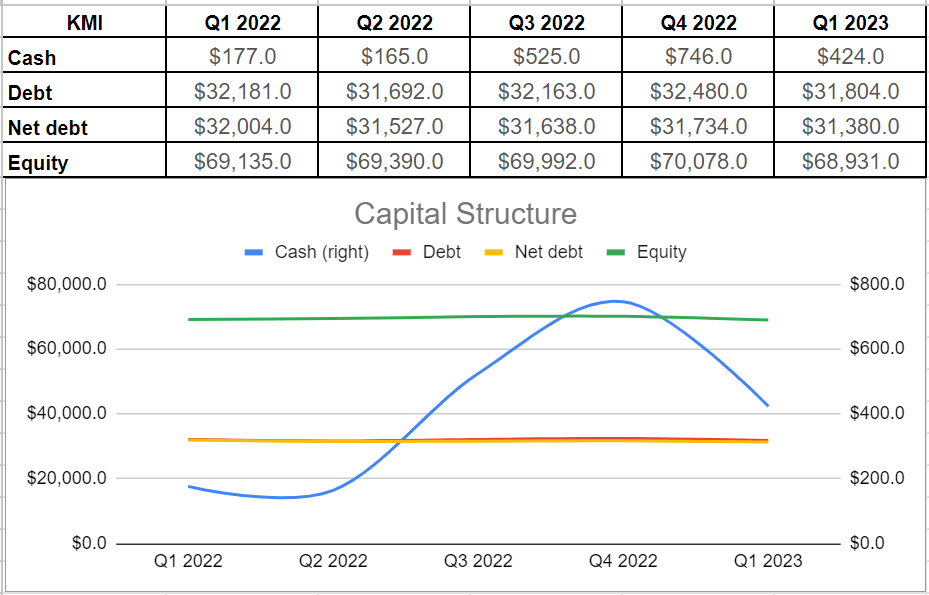

During the first quarter of 2023, KMI’s cash balance declined by 43% to $424 million versus $746 million at the end of 2022, while boosted considerably year over year versus $177 million in 1Q 2022. Their net debt level remained almost flat during the last year and sat at $31.3 billion in 1Q, which there are no concerns since their equity level is well enough at approximately $ 69 billion (see Figure 1).

Figure 1 – KMI’s capital structure (in millions)

Author

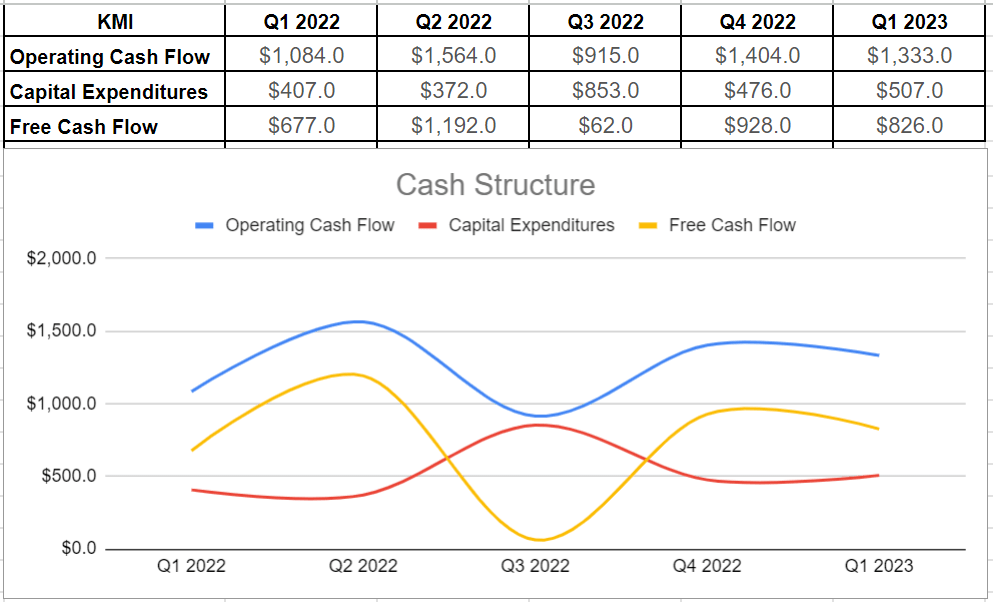

Moreover, in 1Q 2023, the company experienced a slight decline in free cash flow and it was mainly due to their significant investments in expanding their natural gas pipeline systems. Specifically, Kinder Morgan invested heavily in the Permian Highway Pipeline system, adding approximately 550 million cubic feet per day of capacity. They also upgraded and added facilities to Con Edison, which improved its capacity and efficiency. During the quarter, Kinder Morgan spent $507 million on capital expenditures, a 24% increase from the same period in 2022. Additionally, a $1.33 billion of operating cash flow was translated to $826 million free cash flow, a 10% lower than the end of 2022. Going forward, the company’s free cash flow may continue to decline as they prioritize capacity expansions through further expenditures (see Figure 2).

Figure 2 – KMI’s cash structure (in millions)

Author

Market outlook

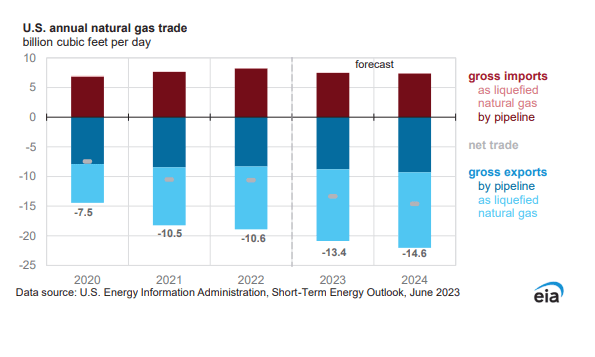

It is anticipated that the Henry Hub natural gas benchmark in the United States will experience a rise during the summer months, with an average of over $2.6/MMBtu expected in 3Q 2023. This increase in natural gas prices can be attributed to a surge in usage within the electric power sector and production growth. Additionally, it is projected that Henry Hub natural gas will reach $3.40/MMBtu by 2024, indicating a 30% growth compared to 2023. Furthermore, U.S. natural gas exports are on the rise, as demonstrated by Figure 3 which shows an expected increase in annual natural gas trade (gross imports + gross exports) for both 2023 and 2024 compared to 2022. The graph also indicates that U.S. natural gas exports via pipeline are increasing, with gross exports expected to climb from 8.31 Bcf/d in 2022 to 8.81 Bcf/d in 2023 and further to 9.31 Bcf/d in 2024.

Figure 3 – U.S. annual gas trade

EIA

Kinder Morgan is well-positioned to take advantage of the numerous opportunities available in the LNG market. With the global demand for LNG on the rise, KMI’s projects can provide additional transport capacity to meet this growing demand. The U.S. is expected to see a significant increase in LNG gross exports from 10.59 Bcf/d in 2022 to 12.08 Bcf/d and 12.73 Bcf/d in 2023 and 2024, respectively, with most of this demand coming from Texas and Louisiana. KMI’s existing network, which is expanding, puts it in a favorable position to benefit from these market conditions in 2023 and 2024. Additionally, KMI’s terminal business can improve due to the increasing demand for renewable and sustainable fuels. The higher demand for renewable diesel, supported by environmental regulations and governments, may increase KMI’s cash generation ability through its renewable diesel plants and renewable natural gas facilities. As previously mentioned, KMI has allocated 86% of its project backlog to renewable projects, with plans to reach an RNG production capacity of 7.0 Bcf by the end of 2024. This focus on renewables positions KMI well for future growth opportunities while also contributing positively towards environmental sustainability efforts.

Risks

Despite its strong financial and market position, Kinder Morgan is not immune to risks that could impact its operations. One key risk is the company’s heavy reliance on the continued production of natural gas, crude oil, and other products by its customers. If production declines or costs rise, customers may struggle to explore new reserves affordably. Additionally, fluctuating commodity prices and changes in tax incentives could lead producers to drop exploration or transportation contracts. Finally, KMI’s operating results could be negatively impacted by unfavorable global or U.S. economic conditions, financial market uncertainty, inflation rates, and rising interest rates. It is important for investors to be aware of these risks when considering investing in Kinder Morgan.

Conclusion

Kinder Morgan’s well performance, strong financials, and the company’s project backlog aligned with higher market demand may cater to notable opportunities for the company. Analyzing their financials and market outlooks, I have updated my previous rating to a buy rating.

Be the first to comment