skynesher

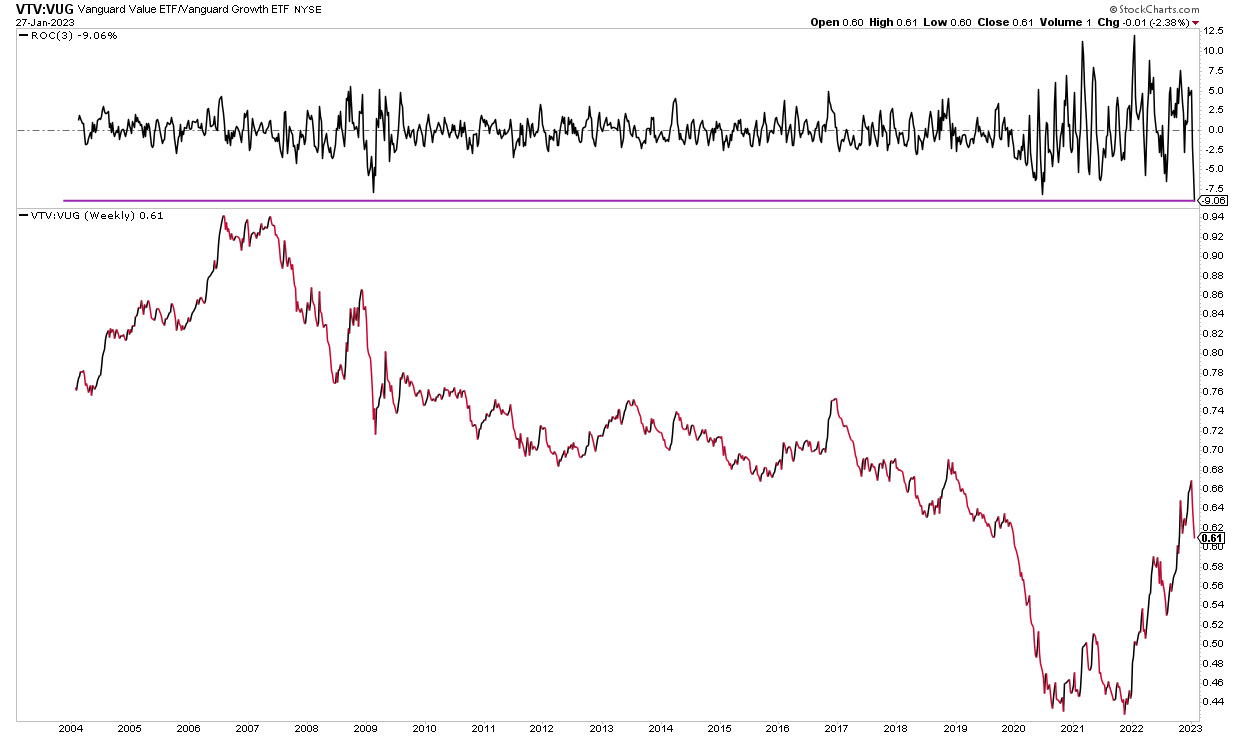

Growth stocks have had a hot start to 2023. Value led the way last year as interest rates were on the rise and the tech-heavy Nasdaq plunged by more than 30%. In fact, over the last three weeks, the Vanguard Value ETF (VTV) is down more than nine percentage points to the Vanguard Growth ETF (VUG). That is the biggest gap in favor of growth in the two funds’ 19-year history.

One value stock is up 70% YoY, but is rolling over, perhaps a part of the broader value-to-growth rotation. But is Unum (NYSE:UNM) still a buy on valuation? Let’s check it out.

Step Aside, Value. Growth Is Back In 2023

Stockcharts.com

According to Bank of America Global Research, Unum is a leading provider of disability income insurance and ranks among the world’s leading special risk insurers. Unum has a strong market share in the U.S. and U.K. Unum has a large legacy book of long-term care (LTC) and individual disability but has put these businesses in runoff. The company distributes via captive sales representatives, brokers, and sales consultants.

The Tennessee-based $8.3 billion market cap Insurance industry company within the Financials sector trades at a low 7.1 trailing 12-month GAAP price-to-earnings ratio and pays a decently high 3.2% dividend yield, according to The Wall Street Journal.

Ranked no. 5 in its industry by Seeking Alpha, the company is rewarding shareholders with a stock buyback on top of its already solid dividend yield. Unum is also operating well as evidenced by earnings beat back in November. A key risk this year is if interest rates decline – Unum’s big long-term care insurance book is very sensitive to changes in interest rates.

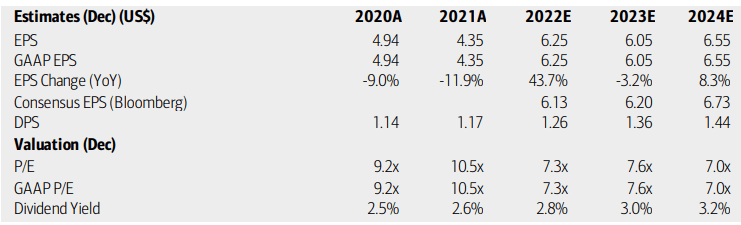

On valuation, analysts at BofA see earnings having risen sharply in 2022, but this year should feature a modest EPS decline. Per-share profits are then anticipated to rise at a solid clip by 2024. The Bloomberg consensus forecast is slightly more sanguine compared to BofA projection. Dividends, meanwhile, are expected to rise despite some earnings volatility over the coming quarters.

The stock still trades at very modest operating and GAAP earnings multiples – solidly in the single digits while paying an above-market rate yield. What I like about Unum is that its forward PEG ratio is just 0.52, a more than 50% discount compared to the sector median and a 24% discount to the stock’s 5-year average. Moreover, the price-to-book ratio, key for Financials sector firms, is just 0.9 (though that is above its 0.62 5-year average). Overall, I continue to like the valuation of this insurance name even after a strong relative 1-year return.

Unum Group: Earnings, Valuation, Dividend Yield Forecasts

BofA Global Research

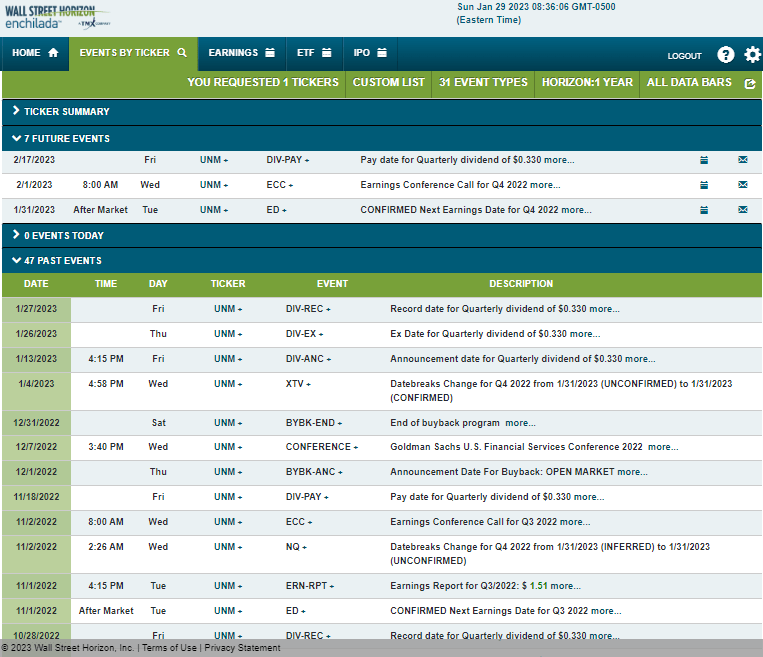

Looking ahead, sparks could fly around UNM’s Q4 2022 earnings date which is confirmed to take place on Tuesday, January 31 AMC. Corporate event data provided by Wall Street Horizon also shows an earnings conference call beginning shortly after the results cross the wires. You can listen live here. The risk calendar is light on volatility catalysts aside from the reporting date.

Corporate Event Risk Calendar

Wall Street Horizon

The Technical Take

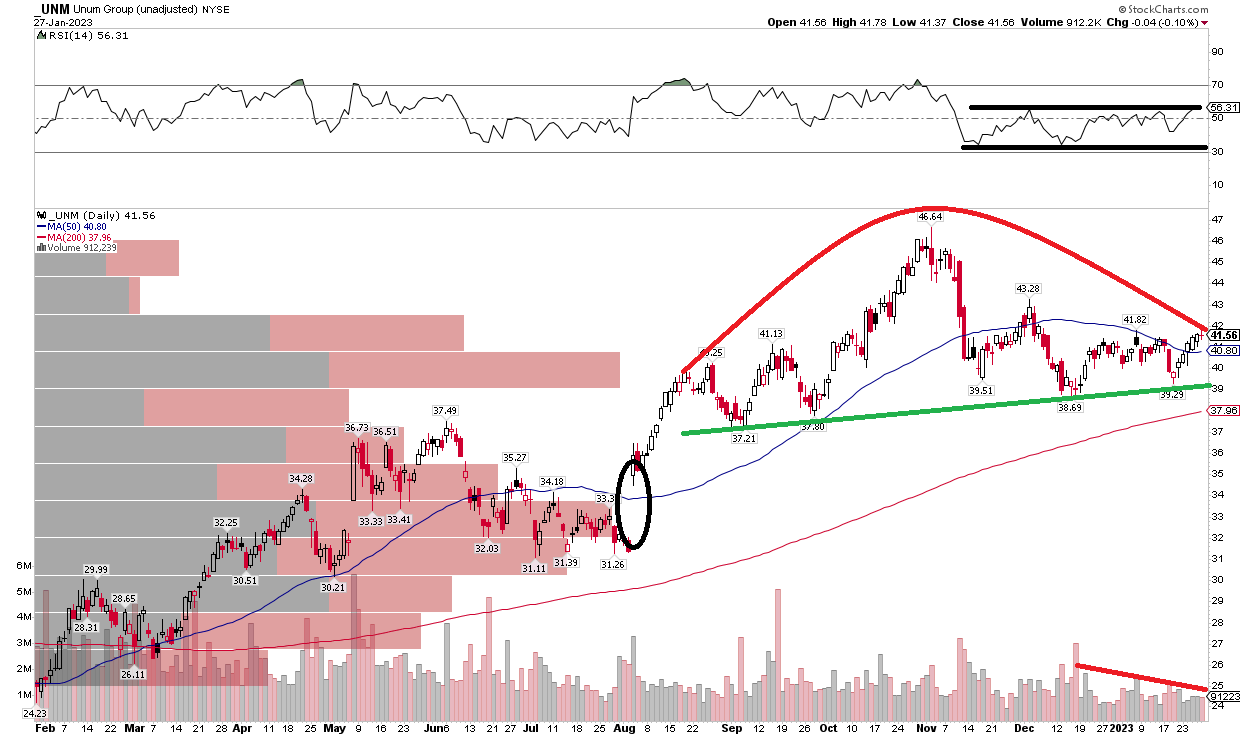

After a massive rally in the last year, UNM shares sport a concerning pattern. Notice in the chart below that there’s a key neckline currently near $39. It is part of a broader head and shoulders pattern with a head at an all-time high near $47. Should we lose the $39 level, then a bearish price target of $31 would be in play – which coincides with the July-August range lows last year and right below a key price gap that happened around its Q2 earnings date.

Right now, the momentum RSI reading is merely sideways in the moderate zone after holding bullish levels during the stock’s uptrend. Moreover, volume is somewhat on the decline during this potential right shoulder forming – that is not a great look technically.

It’s not all bearish though. A bullish potential factor is high volume by price in the $39 to $40 range that should provide some cushion (as we have seen lately). Also, the 200-day moving average is rising, indicative of a bullish long-term trend.

Overall, long here with a stop under the 200-day moving average is a prudent play.

UNM: Bearish Head And Shoulders Forming. Watch $39.

Stockcharts.com

The Bottom Line

While the chart flashes caution, we have a defined risk price level to watch. Perhaps more important for long-term investors, UNM’s valuation and growth outlook are solid despite a pause in EPS advancement this year. I continue to like the stock.

Be the first to comment