adventtr/iStock via Getty Images

One of the constant fears for Qualcomm (NASDAQ:QCOM) shareholders is the loss of the modem business from Apple (AAPL) iPhones. The tech giant has long been known to be working on a 5G modem to replace the Snapdragon chips from Qualcomm, but the recent news has these fears disappearing fast. My investment thesis remains ultra Bullish on Qualcomm with the stock nearly $60 below the yearly highs.

Apple Modem Switch

After ending a lawsuit with Qualcomm over royalties back in 2019, Apple bought the Intel (INTC) modem business to eventually work on a replacement 5G modem. Apple had switched to Intel 4G chips with some success, but Intel wasn’t able to compete with the Snapdragon chips with the start of the 5G iPhone back in late 2021.

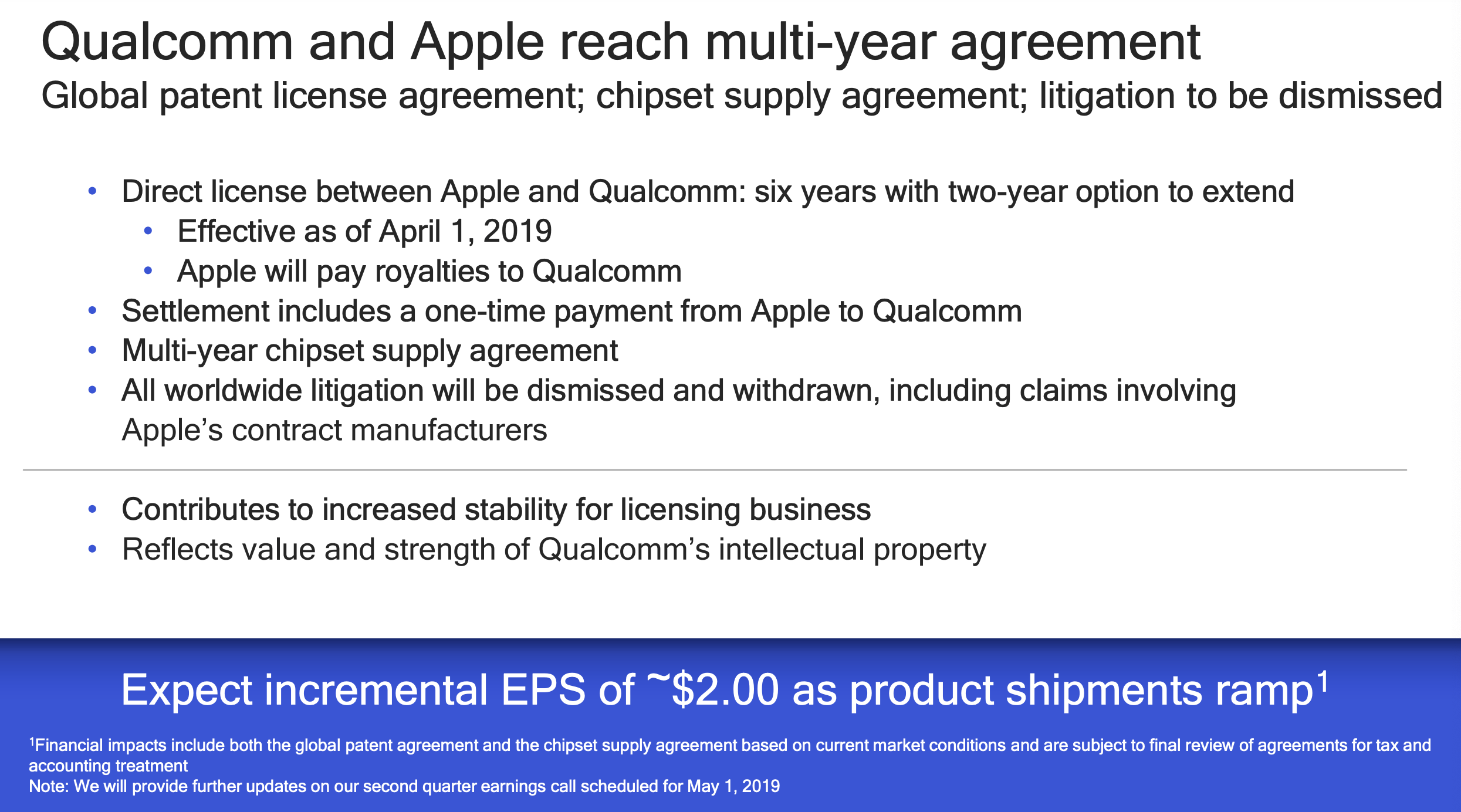

Apple signed a mega deal with Qualcomm to purchase chips for multiple years and pay royalties under this agreement through 2025. While Apple appears to have no path to ending the royalty payments, the biggest risk to the current business model is Apple producing their own modem and no longer paying royalties requiring another legal battle.

Source: Qualcomm/Apple license agreement

For this reason, the biggest risk to the investment story is Apple replacing the modem. The original expectation was Apple introducing modem chips as early as 2023 for the iPhone 15.

Qualcomm originally estimated about a $2+ EPS related to the Apple deal, which included about $1.50 for the royalties and $0.50 for the chips. Clearly, the real risk is the end of the royalty payments, though the lawsuit listed the royalties at no more than $15 per iPhone.

The news had Apple pushing out the transition date to 2024 with a single iPhone 16 device. A Bloomberg report suggested the tech giant was looking to move away from Broadcom (AVGO) Wi-Fi and Bluetooth chips in a strong signal the days were numbered for Qualcomm modem chips in an iPhone.

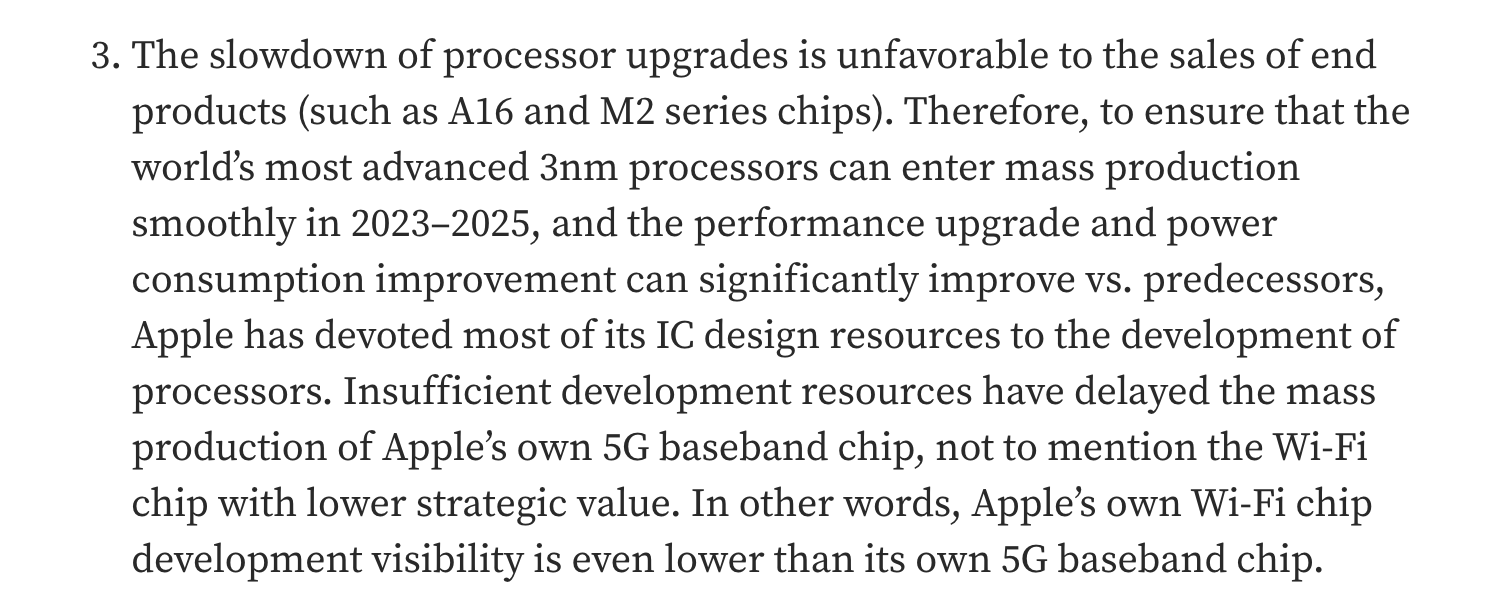

With the technology landscape changing quickly, Apple has apparently made a dramatic shift to focus chip design on processors and away from Wi-Fi chips. Following the cancellation of the iPhone SE rumored as due to 5G modem issues, the news on the Wi-Fi chip halt could be a combination of the desire to save costs and focus on a bigger opportunity where Apple has already seen success in the M1/M2 processor chips.

Analyst Ming-Chi Kuo went on to suggest Apple is focusing most of the IC design resources on the A16 and M2 series chips. The company wants to focus on the transition to 3nm production, though the analyst suggests the 5G baseband chip to replace Qualcomm might have more strategic value than the Wi-Fi chip.

Source: Ming-Chi Kuo Medium.com

Considering Qualcomm appears to have made a case to the European Commission for Apple working to devalue standard-essential patents while charging excessing fees for access to the App Store, the wireless giant might not face any risk of a further royalty battle. In fact, Apple has possibly pulled back on modem chip implementation with knowledge the royalty case won’t be won.

Nokia (NOK) made a very compelling case to the EC regarding the tech giant’s efforts to devalue SEPs helping the case of Qualcomm:

Source: Foss Patents

Full Speed Ahead

Qualcomm has seen the stock rebound to $135 after hitting a crazy low of $101 last year. The company faces short-term hits to profits from weak smartphone demand, but the wireless company has a bright future with or without Apple as a customer.

The chip company has a burgeoning business in the booming auto tech sector and IoT to move beyond wireless modem chips. Once the smartphone demand normalizes with an improving economy and China reopening, Qualcomm should be full speed ahead.

The company earned $12.53 last year reducing the risk of Apple replacing the modem chip. Back in 2019 when the iPhone owner sued Qualcomm, the wireless giant was focused on a $7+ EPS highlighting the huge importance of the Apple business accounting for 30% of profit targets.

The story is different now with Apple accounting for a far lower amount of EPS targets. The tech giant already dropped the lawsuit to obtain the 5G modem and license from Qualcomm, but Apple pursued a case rejected by the Supreme Court all but ending any legal path to question Qualcomm patents and royalties. In addition, Qualcomm extended a licensing deal with Samsung (OTCPK:SSNLF) through 2030 in a sign of the perceived value of the Snapdragon technology.

Now, Apple appears to have a limited case for eliminating the royalties and the fact the tech giant won’t be able to create their own 5G modem until 2024, at the earliest, speaks volumes to the patents created by Qualcomm. In theory, Apple would only be able to bypass the $0.50 portion of the profits paid for the Snapdragon modems.

At a $12+ normalized profit stream, Qualcomm has mass risks of 4% of profits with Apple moving the modem business. Even assigning a generous $1 EPS hit from higher Apple volumes would impact Qualcomm’s profits by just 8%. iPhone unit sales have only risen slightly during this period questioning any reason the impact would top the original $0.50 forecast.

Qualcomm reports FQ1’23 earnings after the close on Thursday. The market shouldn’t expect anything great from the wireless company, even with limited pull forward from smartphone, IoT or automotive demand during covid. In fact, automotive production was weak in 2022 suggesting a thesis of valuing the stock based on FY22 EPS holds.

Takeaway

The key investor takeaway is that the Apple risk is fading fast. The stock should be valued at least at 15x Y24 EPS targets of $12+ valuing the stock a lot closer to the all-time highs above $180.

Investors should use the weakness and any future fears regarding losing the Apple modem business as buying opportunity.

Be the first to comment