prim91/iStock via Getty Images

The United States Brent Oil Fund (NYSEARCA:BNO) provides exposure to Brent crude oil futures. Oil supply/demand balance is expected to remain tight in 2023 as China re-opens its economy. There is also a risk of price spikes like in March 2022 if Russia’s war with Ukraine takes a turn for the worse or if western countries impose additional sanctions on Russia. I am a buyer of BNO as the risks appear skewed to the upside.

Fund Overview

The United States Brent Oil Fund is an exchange-traded security that gives investors exposure to the daily price changes of Brent crude oil. BNO tracks the daily moves of the near month Brent futures contract traded on the ICE Futures Exchange. If the contract is within 2 weeks of expiration, BNO will roll to the next month expiry.

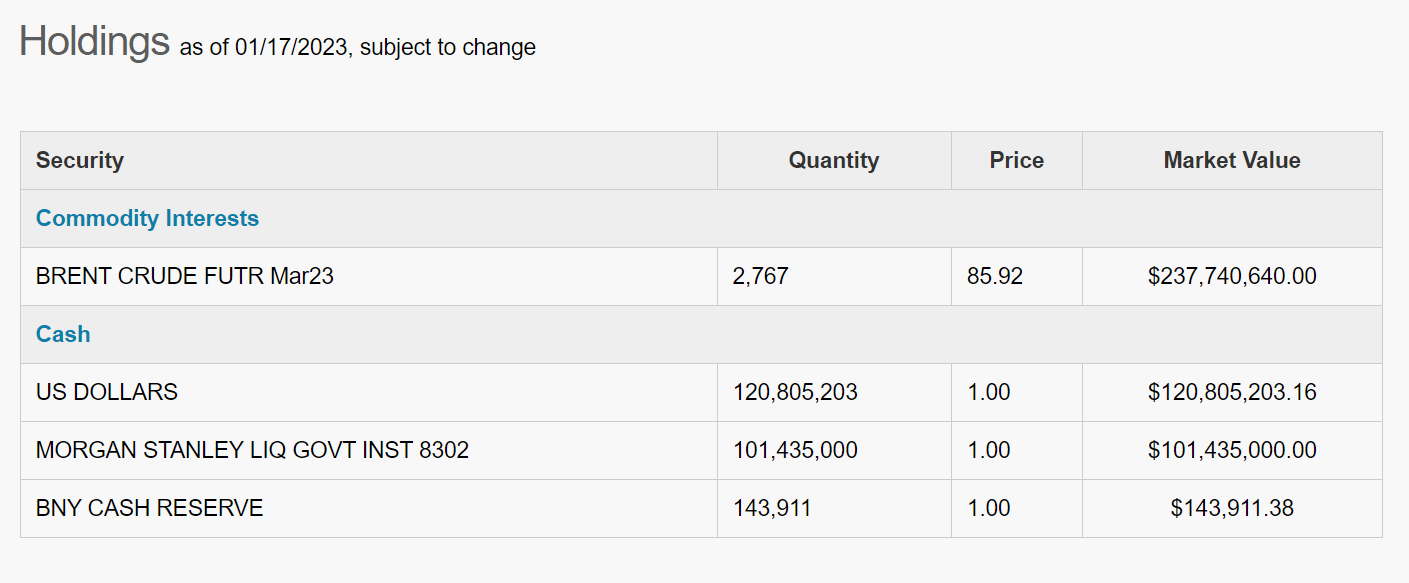

The BNO fund has approximately $240 million in assets and charge a 1.09% total expense ratio (Figure 1).

Figure 1 – BNO fund details (uscfinvestments.com)

BNO Does Not Hold Crude Oil

First, investors need to understand that futures-based exchange-traded securities like the BNO do not hold physical commodities. Instead, their commodity exposure is obtained via the futures market. Figure 2 shows the current holdings of the BNO fund.

Figure 2 – BNO holdings (uscfinvestments.com)

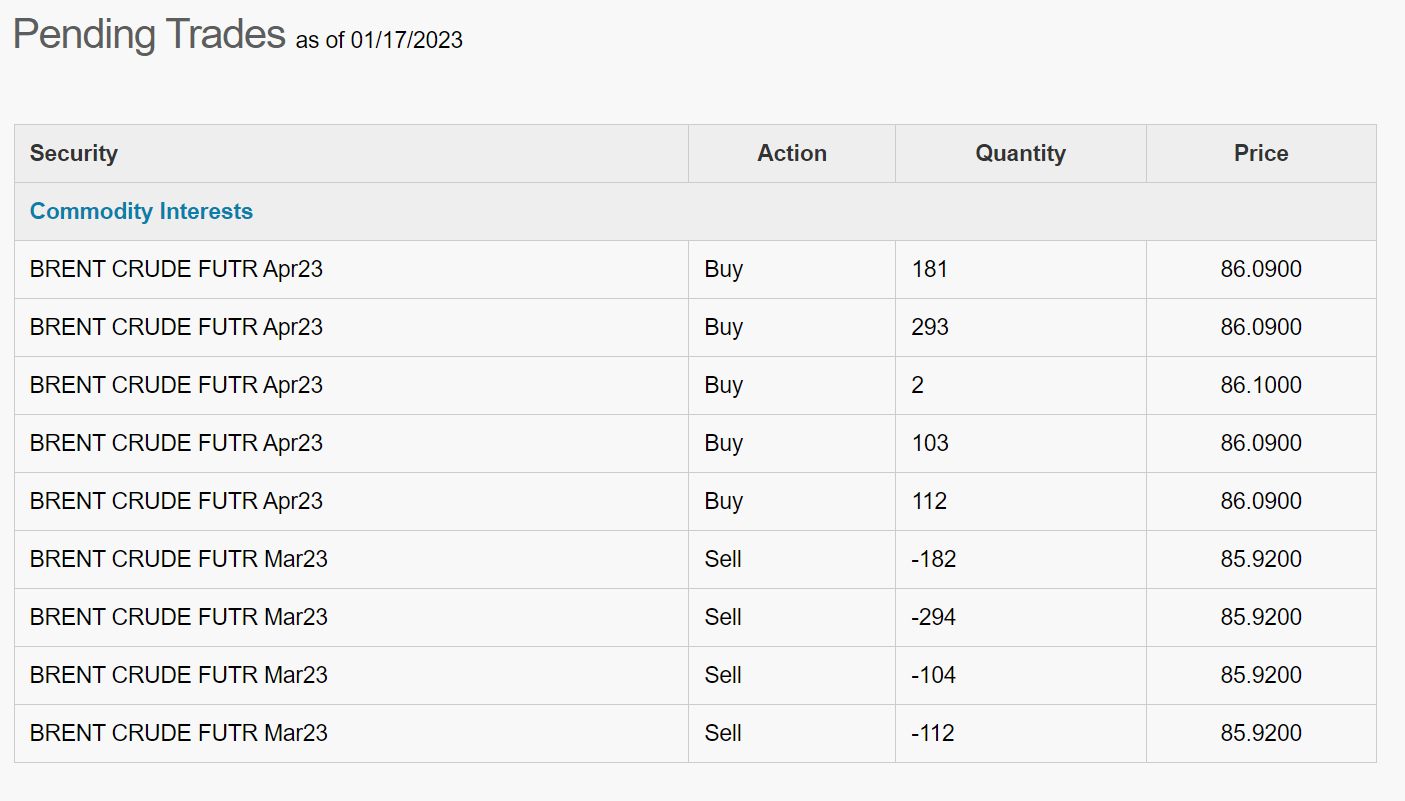

When we get near the expiry of the Brent March futures contract, the BNO fund will ‘roll’ into the April expiry by selling the March futures and buying the April futures. Figure 3 shows the fund’s pending trades.

Figure 3 – BNO pending trades (uscfinvestments.com)

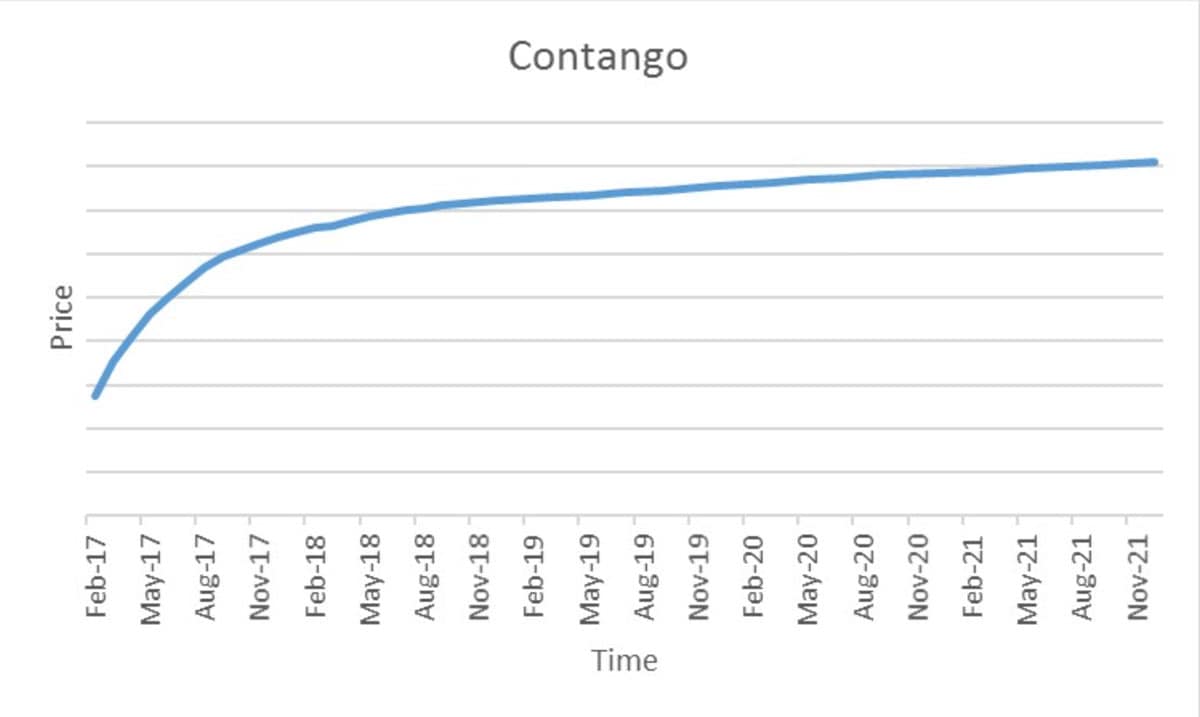

Depending on how commodity futures curves are priced, this ‘roll’ can be beneficial or detrimental. When future curves are in contango, where longer-dated futures are higher in price, futures-based funds like the BNO suffer from a ‘roll-decay’ because they must sell the ‘cheap’ expiring futures and buy the more ‘expensive’ future that is further out in expiry (Figure 4).

Figure 4 – Illustrative contango chart (cmegroup.com)

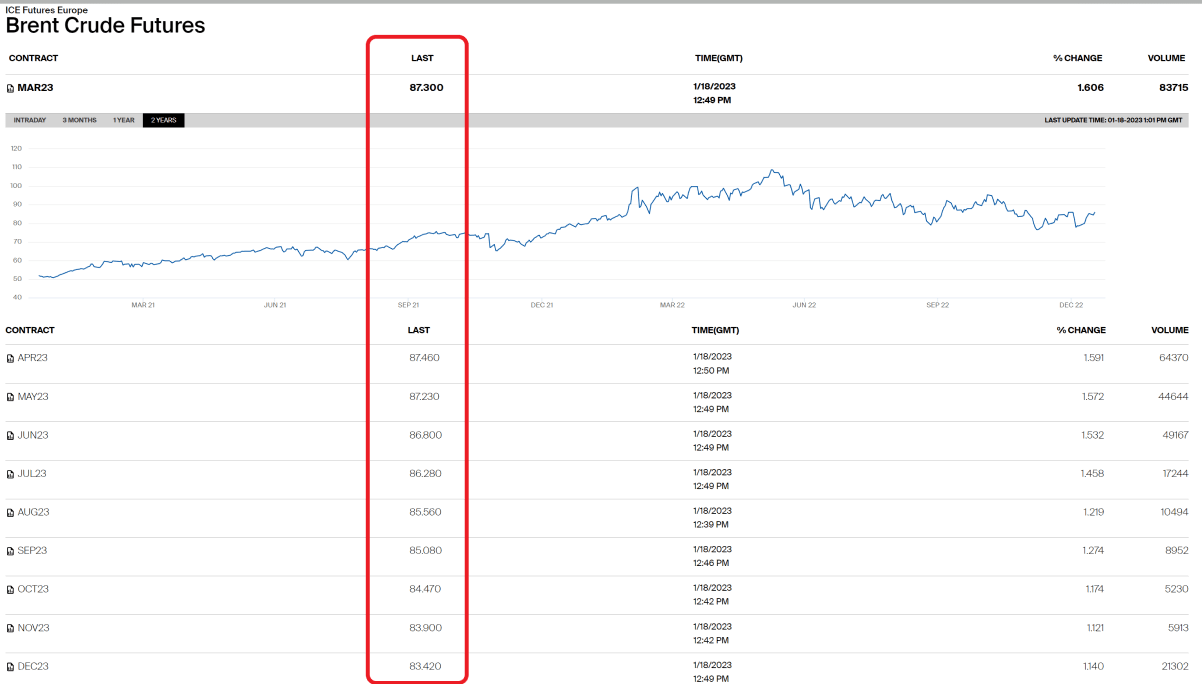

Conversely, when future curves are in backwardation, where shorter-dated futures are higher in price, futures-based funds can earn a ‘roll-yield’ as they sell the ‘expensive’ expiring future and replace it with a ‘cheap’ future that is further out in expiry. Backwardation means supplies are tight in the near-term, so traders are willing to pay a premium for delivery.

Currently, the Brent futures curve is in slight contango at the front end, and backwardated at the longer maturities (Figure 5).

Figure 5 – Brent futures curve (theice.com)

Returns

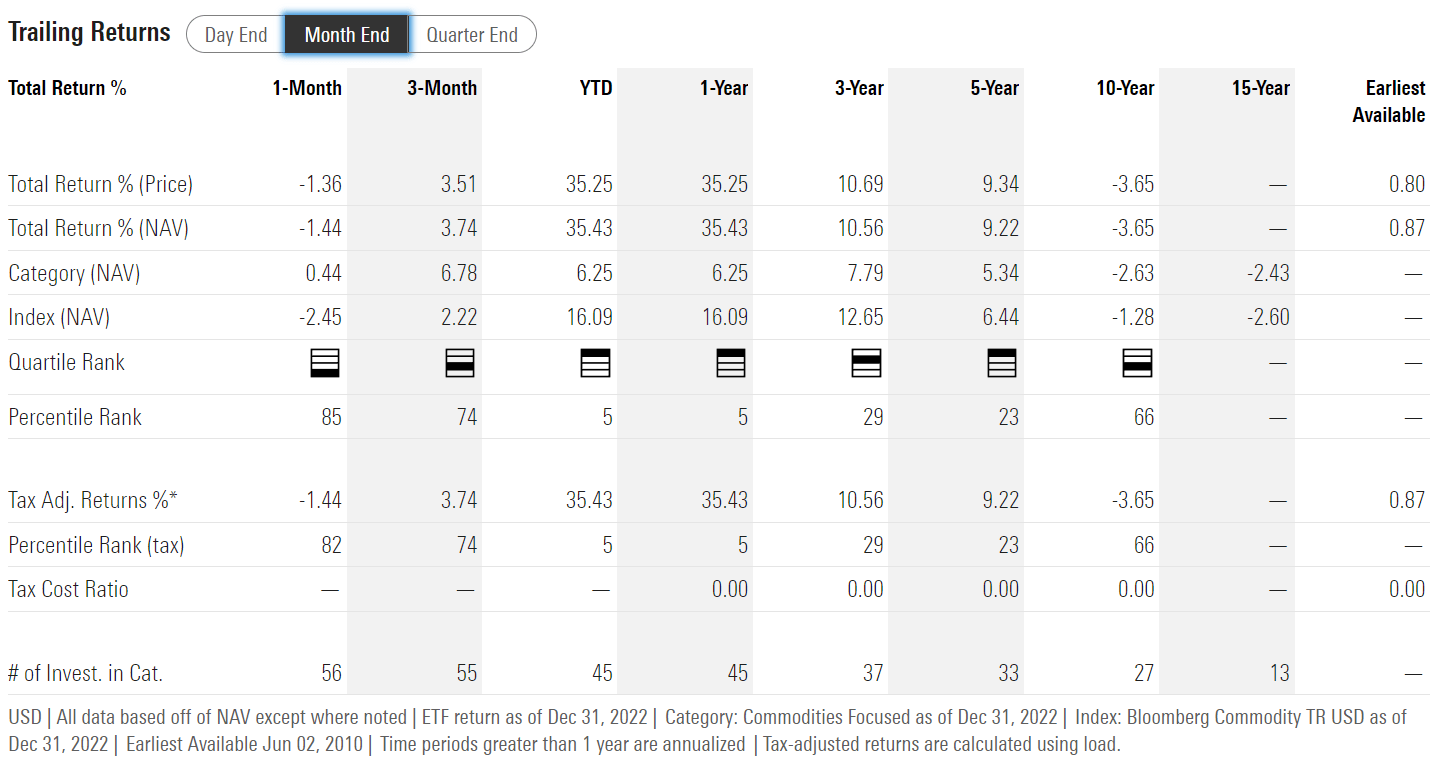

On a trailing 1Yr and 3Yr basis to December 31, 2022, the BNO fund has delivered strong average annual returns of 35.4% and 10.6%, despite the painful drop in the early months of 2020 at the beginning of the COVID pandemic (Figure 6). Long-term 10Yr returns for BNO have been poor, as crude oil is still trading below its peak price from the commodity supercycle.

Figure 6 – BNO historical returns (morningstar.com)

Prices Languished After Russian Surge

Many analysts and pundits were very bullish oil in 2022, especially after Russia invaded Ukraine, putting supply from one of the largest global oil producer at risk. However, crude oil prices actually languished in the second half of 2022, as global growth slowed and China, the largest global oil consumer, suffered from self-inflicted rolling lockdowns due to its Zero-COVID policies. Brent crude prices fell from $125 per barrel in June to a low of $75 in early December.

China Re-Opening To Boost Demand

However, after massive civilian protests in November, the Chinese government’s Zero-COVID position became untenable and risked destabilizing the country. Therefore, the Chinese government changed tack, removing their Zero-COVID policies virtually overnight. PCR test centers were dismantled and travel restrictions were lifted. Infected citizens no longer had to quarantine in ‘quarantine camps’ and contact tracing was canceled.

Although this policy shift has led to an incredible surge of COVID cases in the past few weeks, it does pave the way for China to re-open to the world in the coming months. Recently at the World Economic Forum in Davos, Chinese Vice Premier Liu He commented that China is returning to normal faster than expected and expects “that in 2023 China’s growth will most likely return to its normal trend.”

China’s re-opening has lifted the prospects for crude oil, with the International Energy Agency (“IEA”) recently forecasting in its January outlook report that China’s re-opening could lift oil demand by 1.9 million barrels per day to a record 101.7 mmbpd, with more than half of the growth coming from China. Similarly, OPEC is expecting Chinese demand to grow by more than 500,000 bpd in 2023.

Supply Remains Tight With Little Spare Capacity

On the supply side, the world may be running out of oil supply growth. In August 2022, OPEC famously rebuffed President Biden’s call for OPEC and its allies to produce more oil, stating that the cartel only had ~1 mmbpd in spare capacity. Although the November OPEC production cuts improved spare capacity to ~3 mmbpd, that spare capacity may not be able to cover the expected demand growth plus any supply declines from Russia, due to EU sanctions that recently went into effect.

In summary, the oil supply/demand balance is expected to tighten in 2023, which should be supportive for prices. In an upside scenario, famous energy trader Pierre Andurand recently forecasted Brent crude can trade beyond $140 per barrel if demand growth is higher than expected as Asia fully re-opens.

Technicals Supportive Of Higher Prices

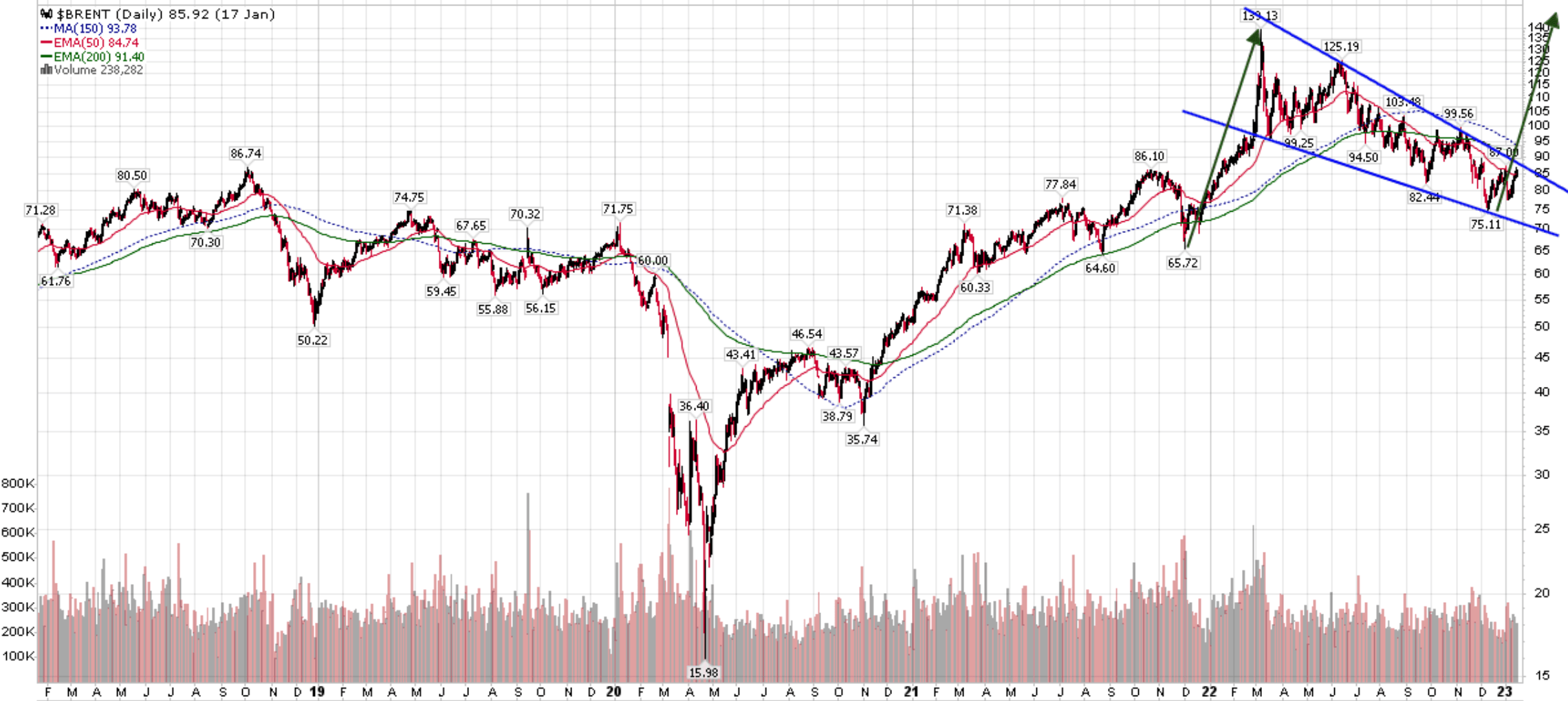

Technically, the price pattern on Brent Crude is shaping a large bullish flag pattern that should target Andurand’s price forecast if triggered (Figure 7).

Figure 7 – Brent oil is shaping a bullish flag pattern (Author created with price chart from stockcharts.com)

Risks

There are two key risks to the BNO fund. First, much of the recent excitement in commodities have been driven by optimism on Chinese demand recovering in 2023. I wrote more about this topic in a recent article on the Global X Copper Miners ETF (COPX).

However, there is a risk that this demand surge may not materialize as envisioned. Many analysts are using China’s 4 trillion RMB stimulus plan in 2009 as a roadmap for the current period. However, that stimulus plan arguably led to tens of billions in malinvestments and corruption, so China’s policymakers may not be using the same playbook this time around.

Furthermore, China’s economy has been heavily developing and adopting clean energy technologies in the past few years. It leads the world in wind and solar power generation, as well as the sale of electric vehicles (Chinese EV’s account for 19% of vehicle sales vs. the global average of 10%). So it is possible that the Chinese economy’s oil sensitivity has lessened relative to 2009.

Second, although China could boost oil demand in the coming year, slowing global growth in western economies could reduce global oil demand, counteracting China’s influence. For example, the IMF recently predicted that 1/3 of global economies would be in recession in 2023, which could be drag to global oil demand.

On the flip side, any negative developments in the Russia/Ukraine war could further reduce Russian oil supplies and spike global oil prices. Russia has already said it will not sell oil to nations that implement an oil price cap. As EU’s oil embargo recently went into effect, how will it affect oil prices?

For context, Russia produces ~11 mmbpd of oil and there is not enough global spare capacity to replace Russian supplies if the country suddenly decides to stop exporting oil. Just think what would happen to global oil prices if Russia suddenly decides to cut oil exports to only 5 mmbpd to ‘friendly’ countries like China and India. Prices would double overnight and Russian oil revenues would be unchanged, but western countries like the EU and the U.S. would suffer a catastrophic energy crisis.

Conclusion

The BNO fund provides exposure to Brent crude oil futures. Oil supply / demand balance is expected to remain tight, especially as China re-opens its economy. This should provide a bid to oil prices. There is also a risk of price spikes like in March 2022 if Russia’s war with Ukraine takes a turn for the worse as Russia accounts for more than 10% of global oil supplies.

Be the first to comment