100pk

It’s better to buy a quality dividend payer near its 52-week low than high, and that may be the case with United Parcel Service (NYSE:UPS). As shown below, UPS is now trading well under the midpoint of its 52-week range, and at $176.72, it’s far below its 52-week high of $234. In this article, I highlight why now may be a great time to layer into this high quality dividend growth stock, so let’s get started.

UPS Stock (Seeking Alpha)

Why UPS?

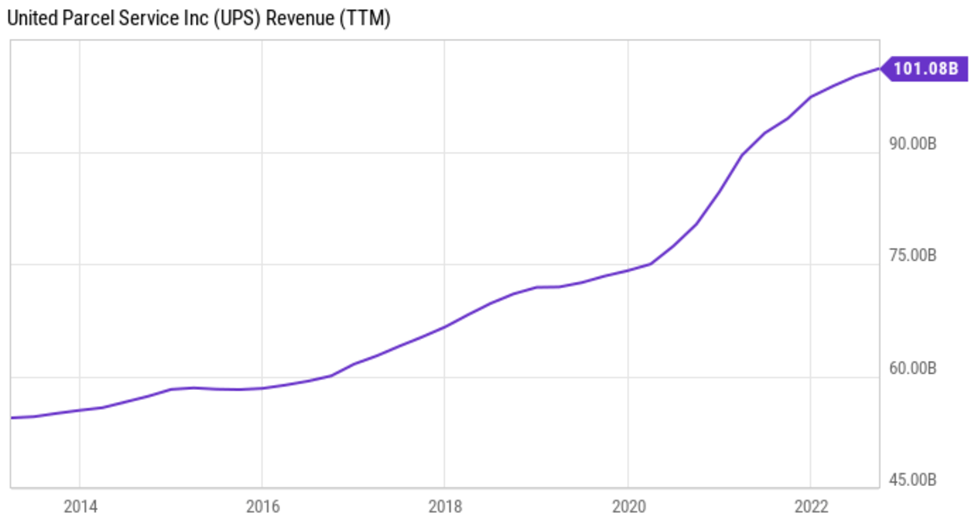

UPS is a global leader in logistics and delivery services with presence in 220 countries and territories and employs 500,000 people. Over the trailing 12 months, UPS generated annual revenue of $101 billion, surpassing its competitor FedEx (FDX) by $7 billion. As shown below, UPS has nearly doubled its revenue over the past decade, with acceleration happening over the past 3 years.

UPS Revenue (YCharts)

While most recognize UPS as just a package delivery company, it also leverages its wide scale and expertise to provide valuable supply chain management solutions to enterprises around the world. Also, in recent years, UPS has been focusing on expanding its e-commerce capabilities. This includes investments in technology and infrastructure to support the growth of online shopping and the introduction of innovative new services such as UPS My Choice, which allows customers to track their packages and make delivery adjustments.

Additionally, UPS has been expanding its fleet of electric and alternative-fuel vehicles, which helps to reduce its environmental impact and save on fuel costs at the same time. This is reflected by UPS’s newest hub in Harrisburg, Pennsylvania, which is home to its largest natural gas fueling station in its network, with the ability to remove 8 million gallons of diesel fuel per year, equivalent to removing 17,000 gasoline-powered passengers cars from the road.

Meanwhile, UPS is seeing respectable growth with consolidated revenues growing 4% YoY to $24 billion during the third quarter. It’s also seeing strong operating leverage, as adjusted operating profit and adjusted EPS grew at faster pace of 6% and 10% over the same timeframe. The top-line growth was driven by the inflation resilient nature of the business, as UPS was able to raise revenue per piece by 9.8% domestically in the U.S., its largest market, which was higher than the rate of inflation.

Near term headwinds include the potential lower demand for package deliveries as management expects for volumes to peak in early winter as customers return to more pre-pandemic shopping behaviors. However, UPS is making moves to become more efficient through use of technology in all aspects of its business, including the onboarding of new employees, which should help save costs. This was noted by management during the recent conference call:

While we will continue to use technology to match daily capacity with customer demand, we are also optimizing air and ground volume to make room for new customers where we can add the most value. In terms of labor, we will bring on more than 100,000 seasonal hires this year related to hiring.

We are ahead of where we were this time last year. One reason is because we have made the digital hiring process even faster and easier this year. We have also improved training for our new driver helpers, which shortens the amount of time from hire to dispatched. Newly hired driver helpers can complete training on their phones and begin work on Day 1.

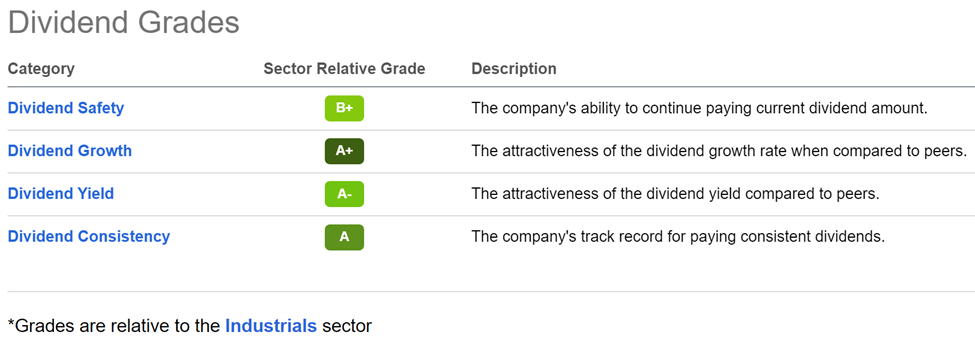

Importantly, UPS maintains an A rated balance sheet and it pays a respectable 3.4% dividend yield that’s well covered by a 43% payout ratio. UPS also has an impressive 5-year dividend CAGR of 13% and 13 years of consecutive dividend growth. As shown below, UPS scores mostly A grades for dividend safety, growth, yield, and consistency.

UPS Dividend Grades (Seeking Alpha)

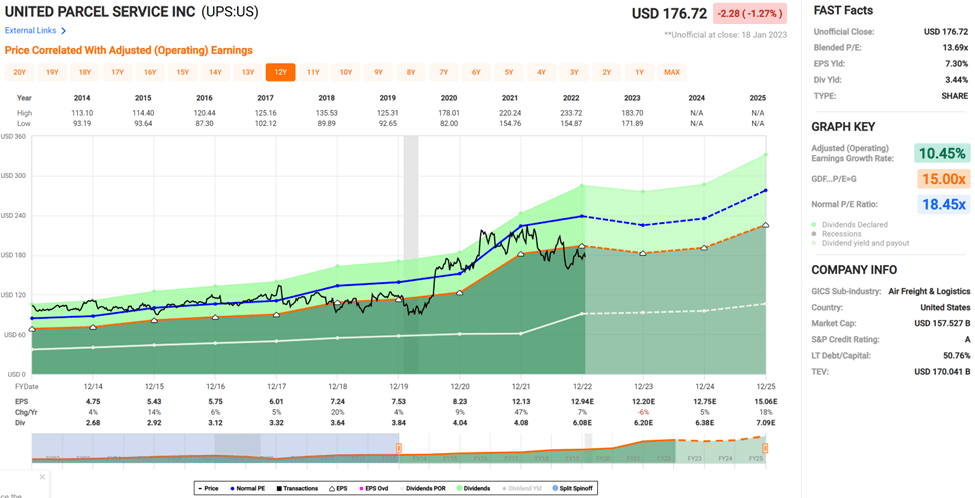

Lastly, UPS is reasonably attractive at the current price of $176.72 with a forward PE of 13.7, sitting well below its normal PE of 18.5 over the past decade. While analysts estimate 2023 earnings to decline in the mid-single digit this year, growth is expected to resume in the following year, and I believe near term headwinds are already baked into the share price.

Analysts have a consensus Buy rating on the stock with an average price target of $189.35, which, while conservative, still translates to a potential one-year 11% total return including dividends.

UPS Valuation (FAST Graphs)

Investor Takeaway

UPS is a global giant that continues to invest in its infrastructure and technology, which should help it become more efficient over the long run. Near term headwinds include the potential lower demand for package deliveries as customers return to more pre-pandemic shopping behaviors. However, this appears to be baked into the share price. Meanwhile, UPS sports a respectable dividend yield coupled with a strong track record of growth, and appears to be attractively valued for long-term investors.

Be the first to comment