sanjeri

It has taken wholesale distributor United Natural Foods, Inc. (NYSE:UNFI) years to digest its 2018 SuperValu acquisition of $2.9 billion. While the company has grown its customer base and increased its offerings and services, its new business model reduced margins and left it with ongoing high leverage. Although the stock price took a hit after posting its Q1 2023 results and missing EPS expectations, we can see an upward trend since 2020.

Five-year stock trend (SeekingAlpha.com)

COVID-19 at-home eating habits pushed UNFI out of the red, and due to the current economic environment, we are seeing an ongoing trend to eat more meals at home. At a market cap of $2.39 billion and an enterprise value of $6.09 billion, with an attractively low price-to-earnings ratio of 7.97, this undervalued stock has long-term upside potential, albeit risky. It has heavily invested in commercial and automation technology across its operations and warehousing facilities and increased operational efficiencies to improve its scaled operations. Although wary of its debt, the challenging market and low cash from operations, it is priced well below its annual price target estimate of $47.25. Investors may want to take a cautious long-term bullish stance on this company as it grows its customer base and is priced low due to negative sentiment.

Overview

UNFI is a food wholesaler and distributor of food and non-food products focusing on health, natural, organic and specialty offerings. UNFI significantly changed after it acquired traditional grocery distributor Supervalu in 2018 for $2.9 billion. Although the acquisition has had a long-term impact on UNFU’s old margins, it has positively impacted growing the company’s customer base, increasing its offerings and decreasing its reliance on Whole Foods Market.

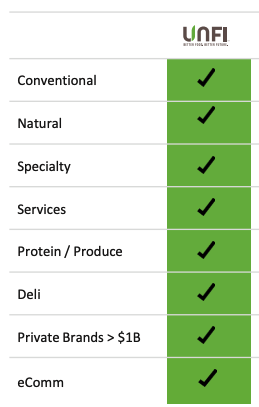

The company’s competitive advantage is its scale of diverse offerings and services UNFI provides retailers, as seen below. Furthermore, its continued investment in e-commerce has prepared the company well for the changing consumer buying habits. It relies on value brands for growth and efficient logistics.

Diverse offerings (Investor Presentation)

The company acts as a one-stop shop that can leverage its offerings to increase customer sales and cost efficiencies by interacting with customers and suppliers.

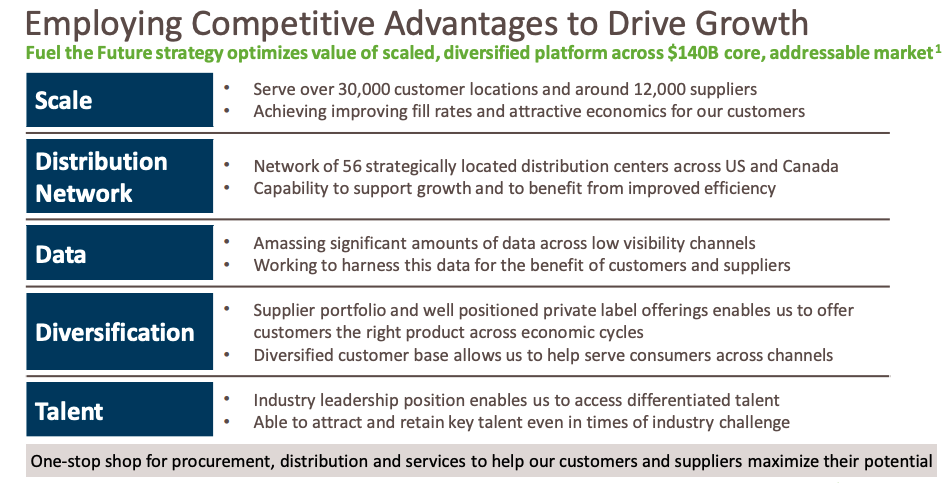

Competitive Advantages (Investor Presentation 2022)

It has grown its offering, created a large distribution centre, reduced transport costs and gained new business and diversified its revenue streams.

Progress charts (Investor Presentation 2022)

Forward-looking, the company, is completing an energy efficient distribution centre which is set to be completed this year. The company is continuing to invest in technology and automation investments. There is still a $140 billion addressable market. The company is also organising Square Roots will allow us to co-locate indoor farms at select distribution centres across our network.

Financial Results

Fundamentally the company is on the mend. UNFI is minimising its leverage, improving efficiency, increasing customer count and buying back shares.

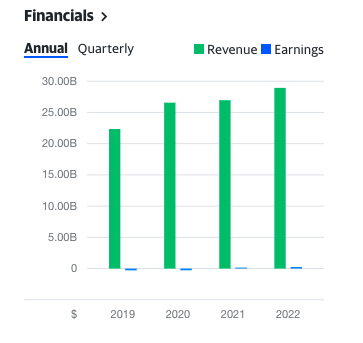

Annual Financials (SeekingAlpha.com)

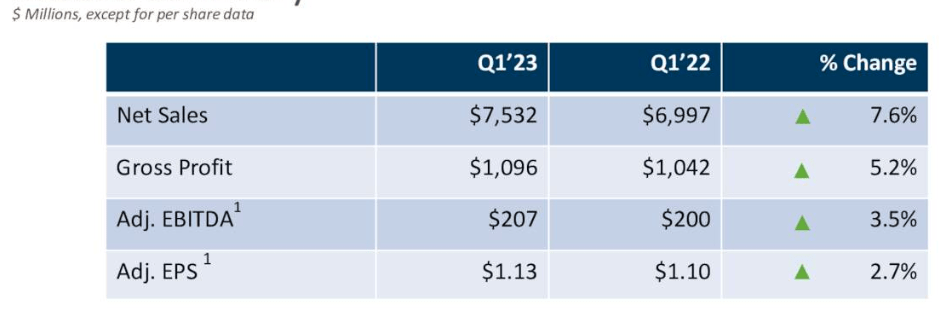

Q1 2023 saw the company achieve a net sales growth of 7.6% year on year to reach $7.53 billion. This was primarily driven by increased inflation, increased new customers and deeper sales penetration of the existing customer base. Net income decreased by 13% yearly to $66 million, and the profit margin decreased by 1.1% year-on-year. Although the company missed EPS expectations by $0.03, the EPS has grown year on year from $1.10 to $1.13 in Q1 2023. The adjusted EBITDA totalled $207 million, up 3.5% over last year’s first quarter.

Q1 2023 Financial Overview (Investor Presentation 2022)

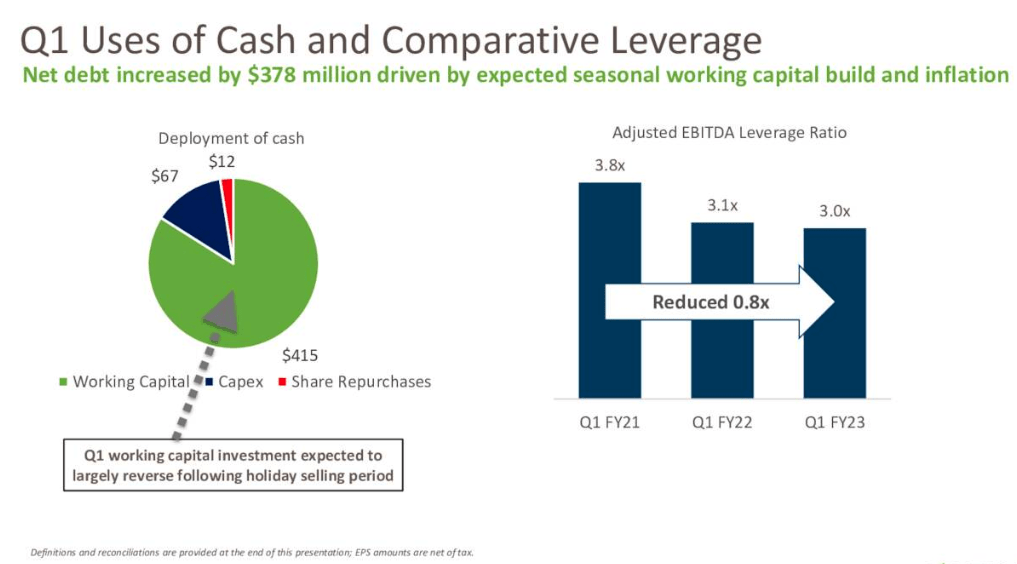

Below we can see the company’s adjusted EBITDA leverage ratio decrease by 0.8 times year on year, and a large portion of the company’s cash is in working capital.

Cash Usage (Investor Presentation 2022)

The company plans to repurchase shares with an authorisation of $200 million. This past quarter UNFI repurchased stocks totalling a value of $12.2 million. Below we’ll be able to see the company’s capital structure. There has been an increase in net debt due to working capital to prepare for the holidays. Ideally, we want to see the net debt to adjusted EBITDA ratio, which is different.

Capital structure (Investor Presentation 2022)

Let’s take a relative peer valuation comparing UNFI to two of the largest retail distributors, Sysco Corporation (SYY) and US Foods Holding Corp. (USFD). We can see that UNFI has a very attractive price-to-earnings ratio of 7.97, much lower than its larger peers.

Peer Valuation (SeekingAlpha.com)

Below we can see that the company has low total cash of $55 million; however, it has a good current ratio of 1.7, indicating that it has enough liquid assets to cover short-term liabilities. It is riskier as the total debt to equity is on the high side at 205.29%, although significantly lower than SYY.

Balance Sheet Comparison (SeekingAlpha.com)

Risks

UNFI has a small number of large customers. UNFI is a risky stock due to its high debt versus equity intake. However, we have seen that it has sufficient liquidity to cover its short-term liabilities. Another risk is that Whole Foods Market was responsible for 20% of its net sales in fiscal 2022, and although the companies have a twenty-year-long partnership, the current contract with them is until 2027. The agreement could change or be reduced, significantly impacting the company’s performance. Another risk is that UNFI is a business characterised by low margins. These margins are currently affected and sensitive to inflation, increased competition in the market and operational efficiencies. Continued reduction in margins could cut into the company’s performance and ability to grow by limiting cash from operations. Lastly, insiders have sold more than they have bought this year. The CAO has sold a large portion of his stocks under market value. However, the company is growing and profitable, so although we should be cautious, there could be various reasons for the sale that took place.

Final thoughts

This company’s value lies in its diverse offerings, distribution, efficiency gains and growing customer base. It has heavily invested in automation, data and e-commerce technologies throughout the business. The company provides diverse offerings to retailers and is contracted with Whole Foods Market until 2027, guaranteeing secure sales. Although debt is still high, the company is managing its debts. Investors may want to take a bullish stance on this company while negative sentiment is in the air.

Be the first to comment