Albert_Karimov

One of the most significant trends over the past three years was the sharp rise in natural gas prices. Natural gas is the US’s single largest electricity fuel source, so higher prices caused electricity, and inflation in general, to rise dramatically. The natural gas bull market was fueled by 2020 supply cuts and a significant increase in US exports to Europe due to the end of Russian fuel sources to the region. Last year, US natural gas prices were over three times higher than they were during most of the decade prior, while European prices rose by over 10X from 2020 to the 2022 peak.

The natural gas bull market has seemingly ended abruptly in recent months, with the Henry Hub price now back to early 2021 levels. The commodity is now within the “normal” trading range it held before the 2021-2022 spike. Prices have declined amid a mix of essential market changes. For one, the US and European winter weather has been abnormally warm, leading to much lower demand for natural gas. Current US storage levels are back within normal seasonal levels, while European storage is abnormally high despite the lack of Russian imports. With European gas inventories strong and prices down, US LNG export demand will likely slow, bringing even more supply to the US market.

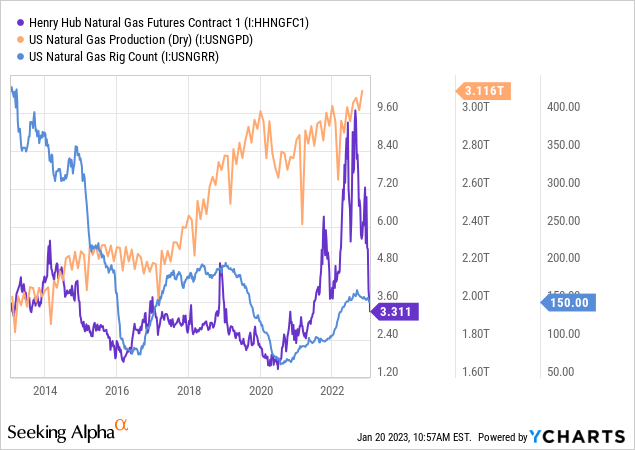

Domestic natural gas production has recovered much more quickly than other fossil fuels. The natural gas rig count increased last year, bringing US production to a new record level. With prices now much lower and close to production cost breakevens, the rig count is falling quickly – signaling a potential decline in US output. Prices are expected to increase by next year, so natural gas futures contracts a year from today are significantly more expensive than spot prices. While natural gas may recover, the immense “contango” may lead to rapid deterioration in the value of popular natural gas funds like the United States Natural Gas ETF (NYSEARCA:UNG).

Will The Natural Gas Bull Market Return?

Last year, I published two bearish reports on natural gas and the related ETF UNG. In June, I wrote “UNG: Stalling Gas Exports May Bring Natural Gas Back To 2021 Levels“, and the fund has been down 53% since then. Later, after prices popped back up, I published “UNG: Why The European Gas Crisis Is Unlikely To Impact The U.S. Market,” with UNG declining 61% since then. The core thesis in those articles was that natural gas prices were too high compared to the storage deficit, which existed but was relatively small. Further, while the US market has been lifted by European demand, only so much US LNG can flow to Europe due to physical limitations, so US prices will unlikely converge toward European levels (unless Europe’s decline). The thesis appears to have proven correct, as speculative fervor has left the market, causing prices to plummet. See below:

US natural gas production recovered quickly from the 2020 declines, with output well above pre-pandemic levels. That trend is led by the US natural gas rig count, which informs us how many new natural gas wells are being drilled. Notably, the rig count must be over ~100-150 for production to increase since many new wells are drilled to replace lost output on old wells. New gas or oil well production levels decline quickly during their first two years so that figure can fluctuate greatly.

Notably, the total number of active natural gas rigs has started to decline after natural gas reached a peak price last year. Most producers will struggle to profit if natural gas prices drop close to $3/MMBTU; drilling activity often plummets when natural gas prices reach such lows. Further, because the energy market has seen higher labor tightening in recent years, parts shortages, and a sharp rise in financing costs, I believe the breakeven level is likely significantly higher today than it was in 2019 when that estimate was made. Thus, I think we will soon see a decline in the natural gas rig count and stagnation in total output as oil and gas companies switch back to “conservation mode.”

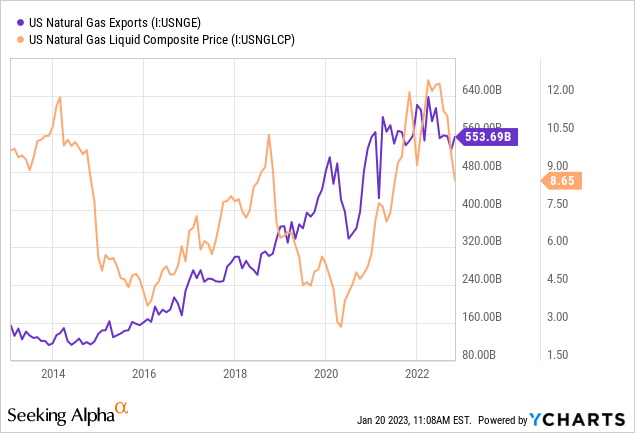

With European gas also back at 2021 “pre-war” prices, US exports to the region may begin to wane. There is an initial indication of this trend in US exports and the LNG price. See below:

Over the past year, Europe’s Russian natural gas imports have declined from over 40% of its total to essentially zero, while Middle Eastern and US imports have entirely made up for the shortfall. More Russian gas has been sent to Asia, which generally receives gas from the US and the Middle East; flows have essentially switched directions, with no change in overall supply levels in each region. As long as prices are sufficiently high, it seems this trade situation will persist. However, since European prices are plummeting, total US natural gas exports may decrease since prices must be significantly different to make (costly) LNG exports.

Overall, I believe the macroeconomic situation indicates a stagnation in US natural gas production due to falling drilling activity; however, total US supply levels may still rise higher due to the potential impact on exports. That said, the large Freeport LNG facility is now back online after months of downtime, potentially marginally increasing exports in the short term. This economic situation is a mixed bag for US natural gas and could eventually cause a rebound in prices, but I doubt this will occur any time soon without an abrupt change in European or US supply levels.

UNG May Decline Even If Gas Stagnates

Warm weather and higher production have caused US natural gas prices to decline to pre-pandemic levels. Today’s storage levels are almost exactly at their average seasonal level. Over the past decade, natural gas ranged from $2-$4 when prices were at seasonal averages (no deficits or glut). With production levels high and winter remaining abnormally warm, the natural gas market may return to a slight surplus over the coming months. Thus, I expect gas to stay below $4 and potentially decline below $3 if US natural gas exports decline due to lower international LNG prices.

However, low prices will force natural gas producers to reduce drilling in the long run. This may occur very quickly today if breakevens are higher than before 2020, as I suspect. Additionally, while the Russia-Ukraine situation may normalize, potentially aiding European prices, it is also possible that the problem will become more extreme. Further escalation in that war could cause European prices to rebound, indirectly assisting US prices. That said, with US natural gas exports near capacity, exports appear more likely to decline than rise.

I do not expect natural gas spot prices to fluctuate significantly from current levels. Eventually, the market may return to shortage dynamics due to the potential impact on the US rig count. Does this mean UNG is a dip-buying opportunity? In my opinion, not – for one key reason; Feb 2024 natural gas futures are priced at $4.53/MMBTU while Feb 2023 futures are trading at $3.36. This vast $1.17, or ~35%, price difference signifies immense “contango” in the market.

Contango is a significant risk for futures ETF investors in commodities since the ETF must buy futures at above-spot prices, making it likely those contracts will decline in value as they near maturity. That is why UNG has lost over 99% of its value since its inception. With the commodity seeing huge contango, UNG will likely lose a third of its value if spot prices remain flat by next year. Of course, if the natural gas market returns to a shortage and reverts to “backwardation” (higher spot prices than futures), then UNG could be a solid bet as it generates a “roll yield.” However, while I am not overwhelmingly bearish on UNG nor natural gas, I believe most investors would be wise to avoid the ETF today due to the high probability of relatively rapid contango decay.

Be the first to comment