bingfengwu

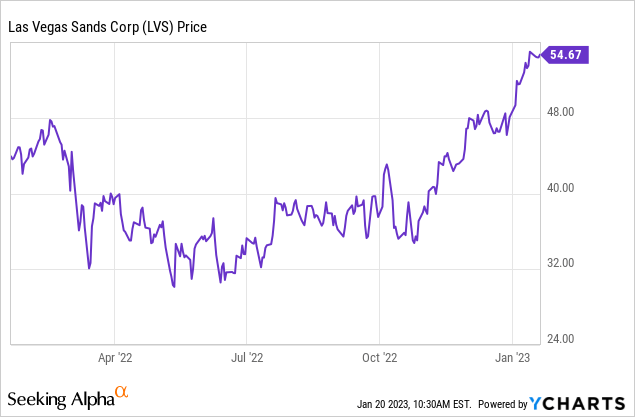

Above: The Venetian Macau poised and ready if Chinese New Year indicates a beginning to a sustained recovery. Las Vegas Sands Corp. controls 12,000 rooms in the city.

google

Above: Last August, LVS began its price recovery largely based on positive trends at its Singapore property. Now Macau will be tested.

“The big money is not in the buying and selling but in the waiting….” Charlie Munger.

For those who read or listen to transcriptions of earnings calls by most companies, the end result is usually elusive. You get some insight, but as for overall management responding to analyst questions – well-meaning as they may be – the answers are mostly the equivalent of coach-speak. NFL coaches in post-game pressers all speak the same impenetrable language: saying nothing by saying something. Win or lose, it all comes out the same, as if scripted by a media-savvy view etched in stone:

I’m proud of my guys. They left nothing on the field.

- We’ll just have to look at the film.

- We took care of business.

- We didn’t take care of business.

- We’ll have to work on that.

- Injuries are no excuse but they are what they are.

We could go on forever, but the few phrases above bear an uncanny resonance to most of the responses from too many managements at earnings calls. Add these few:

- We’re excited about (fill in the blank). They’re always excited about something few other people are excited about.

- Getting our arms around debt is a major priority.

- We’re seeing green shoots in that vertical.

Our point here is this: If all you get from earnings release sessions is coach-speak, where do you find places to penetrate past the pap to determine where the true alphas are buried? If at all, today’s massive flood tide of daily media on stocks has generally revealed most of what comprises ups or downs in the trading ranges of stocks. Investors, both institutions and individuals, live off conventional wisdom implicit in the continuing news flow about the stocks they own.

Adding to the empty investor blather are summits like Davos, which surely meets the test of massive bloviating of empty clichés, dreamlike trances about how the world works, and pathetic attendees in gluttonous pursuit of personal publicity within the political and financial communities.

The result here is the same-investors can’t really tease out what’s real from what’s a never-ending conventional wisdom about how markets may act in the years ahead. The idea, then, is to simply plumb the hard way and ask questions until some semblance of logic appears like an old Polaroid photo image. And make up your own mind.

Gaming executives get it right – mostly

By contrast, the earnings calls for gaming stocks in general break the mold. The senior executives are mostly forthcoming, rarely hide behind lame excuses, and make a real effort at transparency. For me, it’s the questioning that fails the test in that many analysts, understandably protecting access, throw successions of softballs at management. There are some fakers, for sure, but having been on both sides of the rostrum in earnings calls, I think the gaming people generally do a really good job in presenting a few fairytale cover-ups but stick to the hard truths they deal with every day.

Living as they do in an industry that by any measure is probably the single most regulated private business sector in the economy, management faces very little that is not known when they respond to analyst questions for “color.”

The eternal puzzle of Las Vegas Sands stock’s price history

There are few uncut gems hidden anymore. So the idea is this: find the cut gems that, for one reason or another, don’t sparkle enough in the financial media to bring on the price surges of their peers when industry news is good. Prime among them in the gaming sector is the shares of Las Vegas Sands Corp. (NYSE:LVS). As noted above, LVS is an “incher.” When the sector moves on headwind news, we see sharp upsides for stocks like Wynn Resorts, Ltd. (WYNN). The recent spike on Wynn owes a good part of it to the 6.2% position taken by Fertitta.

There are many reasons why LVS stock never seems to move in a sharp upside with some peers that most investors realize is ABC stuff. The perception is that it is, in effect, a private enterprise.

For openers, we all understand that the Adelson family and its foundation still hold over 56% of the outstanding shares. Sheldon Adelson’s widow, Dr. Miriam Adelson, is de facto the last word on the key decision: How much equity does the family wish to take off the table and when? Without question, that is one reason that the stock probably trades in a lower, narrower range than many of its inherently weaker peers.

Let’s face it: pre-pandemic, LVS yielded 4.5% in dividends in an economy where savers were lucky to get 1.5% on CDs and not a helluva lot more in good municipal or corporate bonds. “Hooray for dividends” was the clarion call of Sheldon. Why not, considering the size of the check he was writing for himself?

An industry friend, who knew Sheldon Adelson (d.2021) well, told me on several occasions that some board members had repeatedly urged Sheldon to take equity off the table. One of their rationales was the belief that if a greater portion of the outstanding fell into retail and institutional hands, the trading volume would rise and the very powerful story of LVS would resonate louder in the sector. And that, they believed, would result in better price discovery over time.

google

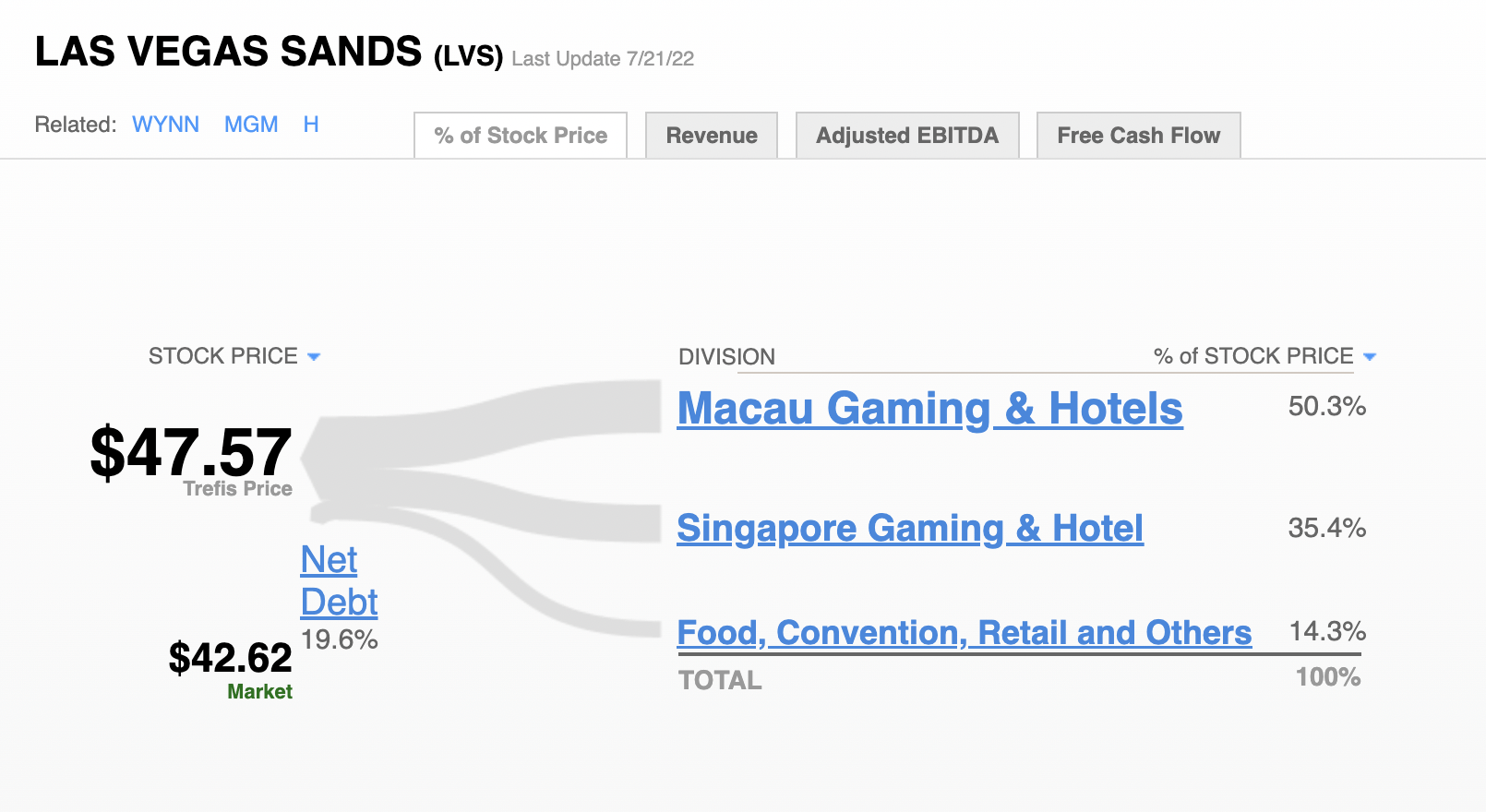

Above: As of last summer, here is the value breakdown as contributors to the LVS stock price by revenue stream. It is likely to remain in the same ratios now.

I recall a dinner I once had with Barron Hilton (d.2019) way back in the day. He told me he was frustrated by the trading range of Hilton (HLT) shares. Part of the reason, he believed, was that the charitable foundation created by his father, Conrad Hilton, which held 27% of the shares, complicated the trading patterns of the stock. Ironically, after Barron’s death, his son sued the foundation for the right to buy at the acquired price of $65m for the huge block when it was worth $495m. Conrad Hilton died in 1979, leaving the hotel de facto to his foundation. The trading range of the stock over time and various key decisions were impacted by that holding.

Barron Hilton told me he wanted to expand the gaming portion of Hilton Hotels but that the foundation presented too many legal issues that made many deals more difficult. Clearly, he did not want to hurt the charity foundation, but he continued to believe that, among other reasons, the foundation block made it harder for investors to get their arms around a true value.

Eventually, the company did buy the block. But it took until 1996 for Hilton to increase its gaming footprint in a $2b deal to buy the then-Bally’s Park Place casinos in Nevada and Atlantic City. Bally’s (one of my alma maters) was a tangled web woven by many circumstances beyond the foundation block. But the foundation had blunted market valuations.

Adelson’s Foundation and family hold 56.8% of LVS shares, institutions another 41.08%, essentially locking up one pathway to a better understanding of the true value of the shares. At what point Dr. Adelson and her advisors might decide to begin taking equity off the table beyond the $6.2b sale last year of the Vegas assets is unknown. The proceeds of that sale essentially sit in the $5.8b cash position of the company.

Thus far, LVS is still dealing with the covid disaster’s impact on its Macau and Singapore casinos. It was assumed by now that Adelson’s successors would have identified opportunities either in Asia or the U.S. to put that cash to work. That position would be further enhanced if the foundation had a plan to make a series of sequential sales of its equity over time. It’s what Kirk Kerkorian did with his MGM Resorts International (MGM) holdings.

The lingering uncertainties of covid contagion in Asia keep something of a dark cloud over many possible acquisitions or ground-up development plans for markets beyond Macau and Singapore. Most recently, a promising door was opened by a decision by Thailand legislators to legalize casinos. LVS would be on the forefront of possible licensees. But that is a development that could be five years away.

New York may come into the LVS crosshairs

Much closer to reality for Las Vegas Sands Corp.’s future is a pending deal to take a long-term lease on the Nassau Veteran’s Memorial Colosseum’s 80-acre site on New York’s Long Island. The legislature has authorized three new downstate licenses to be issued. LVS’s site choice makes great sense. The two Long Island counties plus NYC’s Queens, all within an hour’s drive or less from the site, present an addressable population of 4.17m. It is large enough for Las Vegas Sands Corp. to really show their stuff in developing an integrated resort comparable to Wynn’s Encore in Boston or MGM’s Maryland property.

It is a continuing fallacy in the thinking about casinos in the nation’s biggest market to use distance to Manhattan, or Manhattan itself, as the measure for viability. A center city casino would immediately have to deal with horrific traffic congestion, rising crime, and the entire list of urban ills that plague northeastern cities. Manhattan’s i.6m resident population used to swell to three times that amount when people still came to work in offices and factories every day. The pandemic has effectively emptied out much of that workforce. The proposals from other possible licensees are within the five boroughs or very close. None are as attractive as the LVS plan.

This is a long way off, but the Las Vegas Sands Corp. plan clearly looks like a massive undertaking. Our estimate, baking in an inflation rate in construction costs, looks like anywhere from $3.8b to $5b sunk cost. Assuming LVS at some point will also begin seriously sniffing out post-pandemic Asia, the question arises as to how in theory could it finance two such projects? We raise this question because it has been a matter of corporate faith that any development LVS does would contain a significantly large percentage of equity vs. debt. Sheldon had for years reiterated his position of building with dominant equity rather than debt. If one or both such expansions do materialize while Asia is still in a covid recovery mode, the prospect of moving big chunks of equity from the foundation to the company in order to stay true to Adelson’s legacy begins to get very real.

LVS could unload 50% of foundation shares even at its present market cap of $41.5b for purposes of context at the current $54.69 per share. Such a transaction could literally totally finance virtual debt-free development projects in Asia and New York simultaneously. However, we don’t see current management undertaking so massive an expansion at once. We believe that if LVS were awarded a New York license that it would be the preferred development project.

The trading history of LVS stock reflects a multitude of people and events which have sent mixed signals to investors. As noted, the majority held by Dr. Adelson to an extent is seen as a barrier to an upside by many investors. LVS stock reached a five-year high in June of 2018 of $76, right after the recovery from the wreckage of the 2015 crackdowns by regulators. Contrast that to the 5-year high of Wynn of $196 in the same period. Clearly, as we have noted before, Wynn has always traded at a premium because of founder and former CEO Steve Wynn’s unique managerial talents.

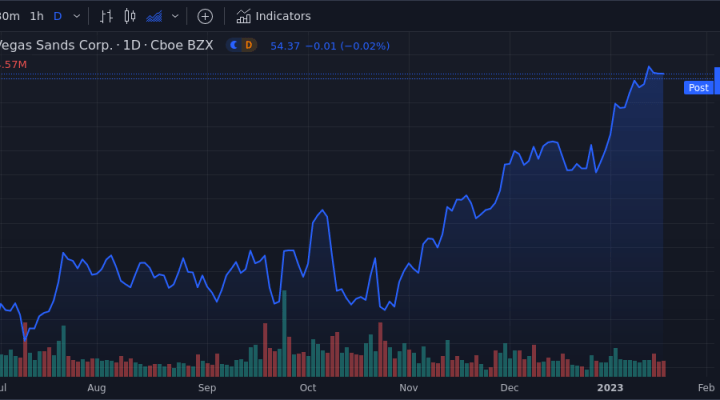

In five days (January 25), LVS will hold its earnings call. Estimates of either a miss, meet, or beat are all over the place at this writing. The street expects ($0.10) EPS. While representing a 54.6% y/y improvement in a turbulent Asian market, the street is likely to focus on net revenues estimated at $1.2b, which would represent a 19.6% y/y gain.

No matter what the number is, the underlying prospects for LVS stock in the intermediate term must include conviction among institutional investors that the long-awaited beginning of a post-zero covid turnaround has arrived. One immediate signal will come from next week’s Chinese New Year numbers. They will show sharp increases y/y but hardly scratch the 1.2m arrivals in baseline 2019. Best case estimates now are 175,000.

When recovery does come and is sustained, bear in mind that LVS has the largest room capacity in Macau, totaling 12,000. It has proven nimble in marketing to the mass segment of the market, which is where the recovery will come first.

No matter what the latest results show, we still believe the trading sentiment on LVS stock will adhere to long-past patterns which tend to impede its true upside due to the Adelson foundation and family holdings. But we also believe that change may be closer than investors believe.

Dr. Adelson is 73 and understandably concerned about the resumption of dividend flows at some point, perhaps by 3Q of this year. CEO Rob Goldstein is 65 and has steered a steady ship since his appointment. Below him is the successor presumptive, Patrick Dumont, COO, the son-in-law of Dr. Adelson, who was CFO and comes from a Wall Street background. The question is whether an equity sale would result in Goldstein staying on board, or taking a big cash haul and retiring. Also, Dr. Adelson’s holdings, in a way, preserve the position of her son-in-law, who some see as Goldstein’s successor – if the family doesn’t sell a share.

Our sense now is that the stars are beginning to align which may see LVS making a key decision to begin unloading some of its equity if and when a firm commitment to either New York or Asian expansion comes to roost at the door of the Board. The 52-week range of $28.88-$55.34 will slosh around until Asian recovery gets more clarity in the months ahead. But the breakthrough to a range that we believe will establish new, higher average ground for LVS stock will come if and when the Adelson family begins to sell off shares for tax or other purposes. Again, this might be nearer than anyone thinks.

It would be a price that truly reflects LVS’s value as a global leader with a strong balance sheet, a cost-conscious management, and the flexibility to expand when and where the right opportunity arrives. And the key propellant of such a breakthrough would be the sale of equity over a given duration.

It’s an easy sequence: Sell off family/foundation equity, raise huge cash pile, invest in a major IR development heavily financed with equity, generate powerfully accretive EBITDA equals a stock whose average value runs well above $100 to $140 a share.

The takeaway

No matter what the earnings or revenue numbers are next week, we see LVS as among the strongest buys in the sector. Clearly, these are the numbers that always drive the valuations of stocks. We don’t deny that. The consensus price target (“PT”) is around its current price, suggesting that analysts believe the stock is fully valued now. Using standard metrics, it is. But, as we quoted Charlie Munger above, making money in the market is mostly about waiting.

Our Las Vegas Sands Corp. PT by 2Q, assuming no move to sell equity by the family, is $67. If the family decides to begin selling its holdings, you are looking at a $100 Las Vegas Sands Corp. stock in an easy glide.

Be the first to comment