Albert_Karimov

The North American natural gas market has been on a wild ride over the past three years. Global pandemic-related production cuts and the war in Europe caused prices to surge to decade highs as many feared a considerable shortage. After peaking around $9.4/MMBTU last fall, I published “UNG: Why The European Gas Crisis Is Unlikely To Impact The U.S. Market,” warning market fundamentals did not appear to support the elevated natural gas price. Since then, the commodity has crashed to around $2.45/MMBTU, with the futures ETF The United States Natural Gas ETF, LP (NYSEARCA:UNG) falling 70% since the bearish article was published.

More recently, when natural gas was at $3.3/MMBTU, I published a neutral article warning that prices may remain low for some time titled “UNG: Expect ‘Lower For Longer’ Natural Gas As Europe Avoids ‘Cold Winter.'” Three weeks ago, my view was not necessarily that natural gas prices would fall further but would likely remain below ~$4. However, with natural gas back at extreme lows, most producers will not be able to make a profit and, therefore, will likely race to reduce production. The natural gas market is very tight, so a reduced output could cause the shortage to return. Thus, with UNG and natural gas at extreme lows, I believe a decent dip-buying opportunity today could result in a bull market. However, with significant contango and weather-related uncertainties, caution is still advised.

Why Natural Gas Is Likely Bottoming

For most of the past year, I have not been particularly bullish on natural gas since the market appeared to have excessive speculative fervor surrounding the European energy crisis. The controversial destruction of the Nord Stream pipeline has made Europe’s situation direr. However, warm weather and ample exports from the Middle East (albeit at extremely high prices) stopped the shortage from worsening over winter. Still, with the US exporting LNG at capacity, the carry-over impact to the North American natural gas market is limited.

Further, with European prices much lower, US LNG exports are slipping, exacerbating the potential glut in the US. I believe this issue is the chief cause of the most recent decline in the US natural gas price. The upcoming reopening of the Freeport LNG plant could offset that issue, but the impact may be limited now that Europe’s gas price is ~80% below peak levels.

Crucially, many producers cannot profit when natural gas is below $3/MMBTU. There is significant variability of breakeven costs geographically, and higher crude oil prices can offset low natural gas since they are often produced together. However, with crude oil also below $80, crude oil may be on the verge of becoming unprofitable. Further, I believe historical breakeven estimates are likely below actual levels since inflation and labor shortages (which are significant for energy) have caused production costs to snowball. Thus, it looks pretty likely that most energy producers are facing losses, particularly those focused on natural gas.

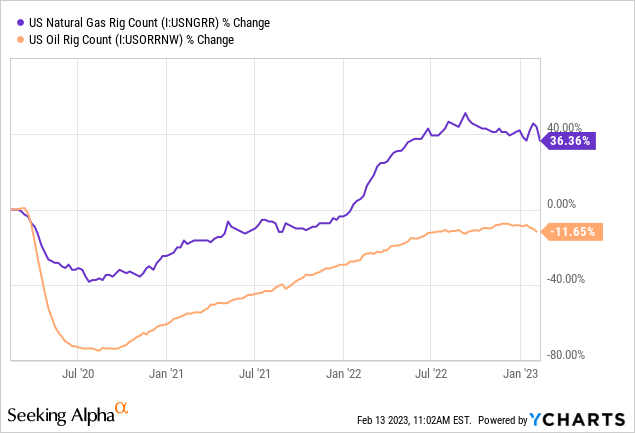

Last year, excessively high natural gas prices and the shortage concern surrounding Europe caused natural gas producers to increase output dramatically. As explained in my previous UNG article, US natural gas production rose well above pre-COVID levels, while crude oil production remains well below 2019. Significantly, the natural gas and crude oil rig count are declining as prices tumble toward unprofitable levels. See below:

Today, the natural gas market is slightly glut, while crude oil is relatively neutral. However, Russia recently acted to cut output by 500K barrels per day, likely pushing the global market back into a slight shortage. That said, US crude and natural gas prices remain too low for most producers, causing them to reduce their rig count.

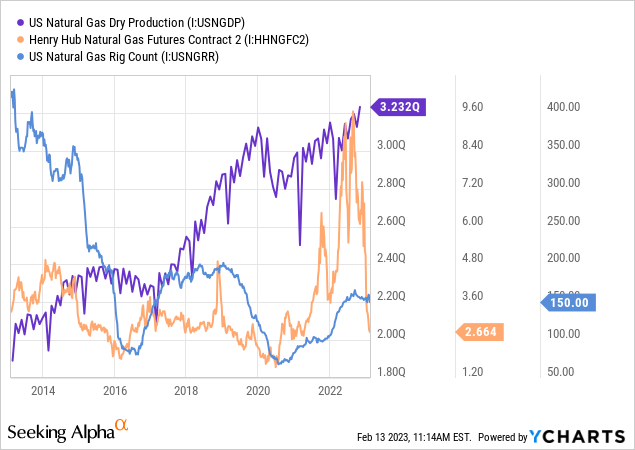

In my view, most US energy producers are extremely conservative today due to immense losses from the past decade’s glut. Most have high financial debt due to negative cash-flows from 2014-2019 and have challenges receiving financing due to banks’ ESG goals. Thus, in light of potential unprofitability, I expect most US oil and gas producers will rush to lower their rig count to maintain cash flows. At this point, it is unlikely producers will shut off wells as they did in 2020 but allow well output to deplete (which occurs rapidly during their first two years) without a supply of newly drilled wells. Most likely, that should cause a negative production trend similar to 2015-2017, which eventually resulted in a price spike. See below:

After prices crashed in 2014, the natural gas rig count began to decline. At that time, natural gas production had to decline for about a year before natural gas prices rose back to profitable levels in 2017. Further, natural gas prices did decline for a period while the rig count and output were falling. Thus, it is not necessarily guaranteed that natural gas will reverse higher as the rig count falls – it may take some time before the market falls back into a shortage dynamic.

One significant difference between the 2015-2017 market and today as that natural gas, and the global energy market as a whole, is far more fickle today. In 2015, the market underwent an immense change as the “shale revolution” greatly increased production capacity. Today, the market is at the end of that revolution as production costs rise and sources of cheap gas become more scarce. Further, the inventory of “Drilled but Uncompleted” wells has dried up after immense use since 2020, which allowed energy companies to expand production without drilling. Thus, today’s rig count is likely already below the necessary replacement rate, meaning associated production declines may be more significant and rapid.

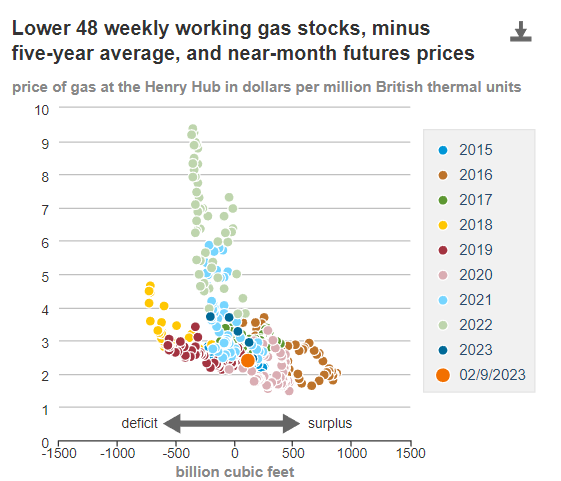

Finally, the price of natural gas is relatively low given the minor glut today, particularly considering it will likely be short-lived. Historically, we can expect gas to be $2-$4 when excess inventory is near zero, but it can rise to $3-$5 if a slight deficit returns. See the relationship below:

Natural gas price vs. excess (deficit) storage (Energy Information Agency)

Natural gas is currently priced for a relatively significant glut. In my view, the output situation, the negative shift in US weather patterns, and the upcoming reopening of Freeport may act to push the market back into a shortage. At this point, I do not believe the shortage will be significant enough to justify a >$3.50/MMBTU gas price, but it dramatically skews natural gas’s potential toward the upside, given its seriously depressed price.

Understanding UNG’s Contango Risks

If investors could bet on the spot price of Henry Hub natural gas, it would be a no-brainer buying opportunity today. While gas may fall lower, I believe it is generally unlikely given the likely production cuts that would occur as long as gas is below breakeven levels. In my view, we will most likely see gas fluctuate around the $2.5-$3.5 range for most of this year unless exogenous factors significantly impact the market (which they often do). If the rig count falls enough, a higher price may eventually occur – particularly if Europe’s LNG demand rises back to US capacity levels.

The chief issue with UNG today is the massive contango in the natural gas futures curve. Natural gas’s spot price is around $2.45, but the February 2024 future price is currently $4.11 – nearly 70% higher. This is a staggering degree of contango in the curve, implying a large glut in the market today that is not expected to last more than a few months. However, this means front-month futures will likely decline in value as they reach maturity. The current estimated “drag” is around 40%, meaning UNG will decline around that much if natural gas remains around current levels. I suspect natural gas will rise as anticipated in the futures curve, but UNG has a tremendous embedded carry cost until that happens.

Overall, while I believe natural gas is oversold and has most likely reached its bottom, I would be very cautious about buying UNG right now due to its contango risk. Contango is the primary reason UNG has lost virtually all its value since its inception. Thus, I am neutral on UNG overall but may become bullish if the contango clears up. Oil and gas producer stocks, such as those in the ETF (XOP), maybe a better bet today since they’re likely discounted. However, even those firms carry elevated risk since they could become unprofitable if energy prices do not rebound soon.

Be the first to comment