Brycia James

In very surprising news, Nike (NKE) discussed on their recent earnings report how inventory levels at the giant athletic footwear company were now out of control. The news is somewhat shocking considering how well Under Armour (NYSE:UA, NYSE:UAA) navigated the supply chain crisis with flat to down inventory levels. My investment thesis is ultra Bullish with the stock trading at COVID lows.

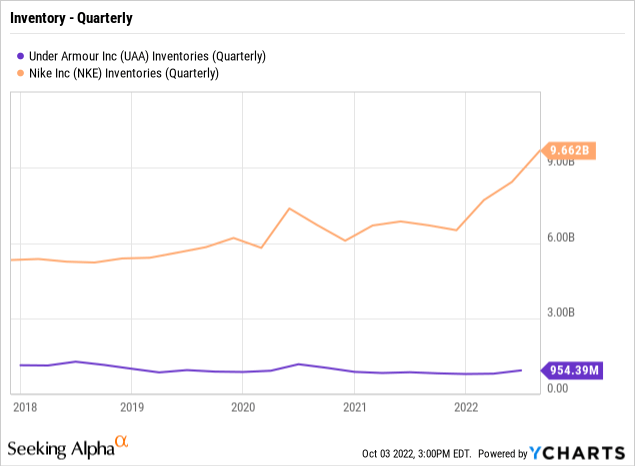

Shocking Inventory Picture

Over the last couple of years, Under Armour had made huge progress in improving margins and managing inventory levels to generate solid profits. The COVID impacts on the supply chain pressured gross margins over the last year to hide a lot of those improvements.

The athletic apparel retailer recently reported quarterly inventories of $954 billion, flat from 2019 levels with revenues up 13%. Under Armour appeared in a solid inventory position considering the management team decided to constrain and cancel orders, even at the cost of lower sales due to a lack of product in certain areas.

For this reason, the inventory news out of Nike following FQ1’23 results was shocking to the market. The athletic footwear giant reported inventories for the period ending August jumped 44% YoY to $9.7 billion. The company now has inventories 50% above 2019 levels.

The combination of late delivery of prior season orders and a surprise early delivery of holiday orders has led to the rapid surge in inventories. On the FQ1’23 earnings call, CFO Matthew Friend was clear the issue was mismatched ordering with still strong demand:

In September, month-to-date retail sales are up double digits versus the prior year, following a strong back-to-school season. However, our North America inventory grew 65% versus the prior year, with in-transit inventory growing approximately 85%.

In essence, double ordering pressured the supply chain to catch up with orders, not actual demand. On the earnings call, Nike confirmed shipping times are down substantially, which should lower elevated freight costs:

Earlier ordering by retailers, driven by strong consumer demand and less predictable delivery timelines, had led to elevated inventory levels broadly across consumer goods. Then transit times began to rapidly improve with signals that further improvement may be coming.

The good news is that the supply chain issue is improving. The Los Angeles/Long Beach ports no longer have a massive backlog and the WSJ confirmed Trans-Pacific container costs are down substantially from last year. In fact, each container now costs $15,100 less and demand is collapsing during the seasonally strong holiday period due to retailers like Nike ordering early.

A Better 2023 Ahead

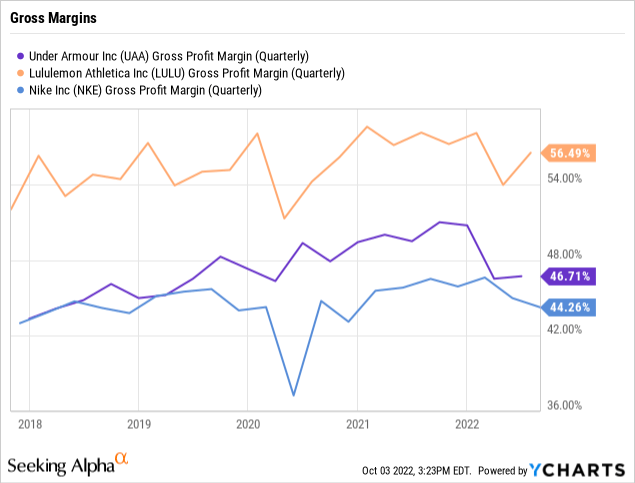

As highlighted prior, Under Armour topped 50% gross margins during 2021 and was on pace to sustainable strong margins. The company had separated the business from Nike back into a premium tier with higher margins.

The whole sector has seen margins pressured with Nike just reporting last quarter margins down 220 basis points at 44.3%. Under Armour is still forecasts above those levels with guidance for the new fiscal year at ~45.6%.

The key here is that the normalized supply chain and inventory markets in the next fiscal year sets Under Armour back up to recapture the rebound. The stock traded above $20 when margins topped 50% with a strong trajectory towards a sustainable level between Nike and Lululemon Athletica (LULU).

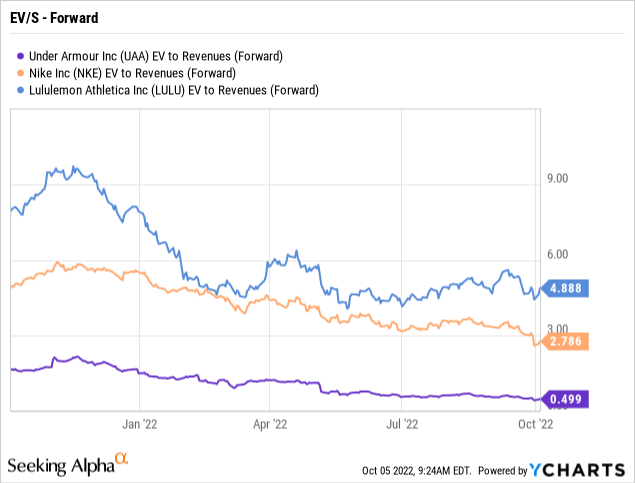

The stock was recently mis-valued for a firm with solid growth rates and margins above Nike. Each dollar of sales at Lululemon is worth nearly double the amount of such sales at Nike while each dollar of sales at Under Armour is near worthless compared to this peer group.

If valued similar to Nike, Under Armour would trade at $41 now. Nike was even traded at much higher multiples during the last few years suggesting this multiple is more of a depressed level, yet Under Armour would still trade at double the recent COVID levels.

Takeaway

The key investor takeaway is that one can argue Under Armour has handled this period better and higher margins would warrant a larger forward EV/S multiple for the athletic apparel company. The market hasn’t fully recognized the turnaround of the company.

Investors should use this gift with the stock trading far below market multiples.

Be the first to comment