Aranga87

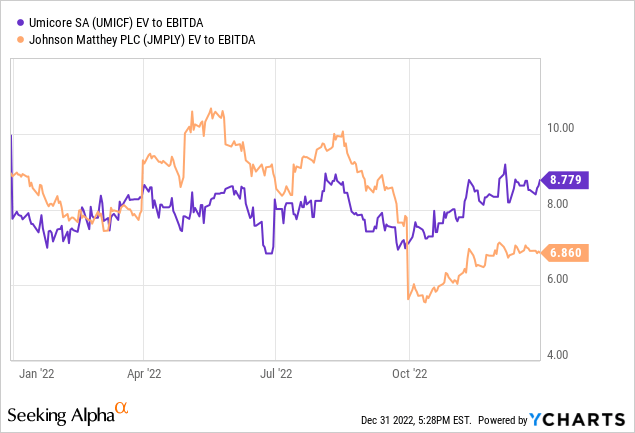

Since I last covered the stock, Umicore (OTCPK:UMICF) has delivered another win with the Volkswagen (OTCPK:VWAGY) battery JV; the recent strategic supply agreement highlights good progress toward its mid-term battery materials/battery recycling growth targets. The stock was flat on the news, however, reinforcing the view that these growth markets are becoming increasingly competitive. Given the company’s limited differentiation as well, I am hesitant to underwrite a strong ROCE outlook from these growth investments. At the current ~9x EV/EBITDA, the stock isn’t cheap relative to its growth outlook, nor to its closest peer Johnson Matthey Plc (OTCPK:JMPLF), which trades several turns lower. For now, I remain neutral pending improved visibility on the execution, as well as the demand trajectory for cathode battery materials ahead of the guided H2 2023 ramp-up.

Another Supply Deal for Umicore/PowerCo, but ROCE Bar Remains High

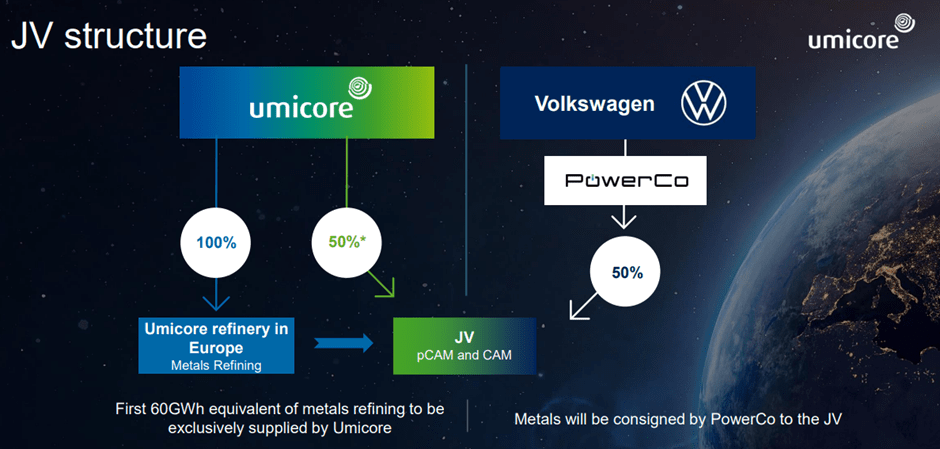

Umicore made impressive headway into its future growth goals in 2022. The joint venture with Volkswagen Group’s battery company PowerCo in September was a key milestone, paving the way for significantly increased battery materials production scale (~40GWh of battery cell capacity) by 2026. Management promised another big announcement for the year, and it delivered via the JV with a memorandum of understanding (MOU) for a strategic supply agreement in North America related to precursor and cathode materials. The deal terms outline supply to commence in 2027 before ramping up to 40GWh by 2030. The supply will likely come out of Umicore’s 80GWh capacity in the future Ontario plant, which, together with VW’s gigafactory buildout, should keep utilization high.

Umicore

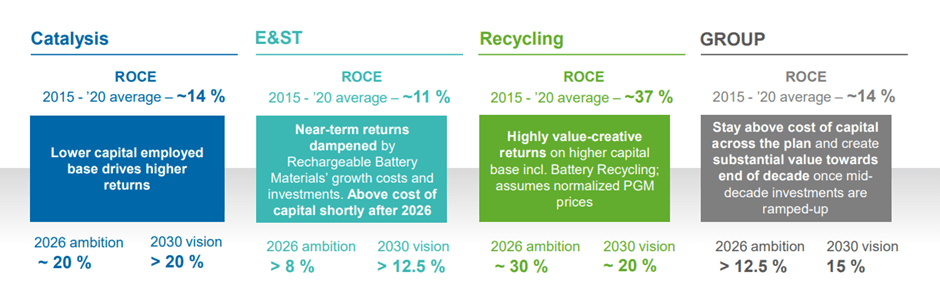

More broadly, the deal marks another step toward increasing Umicore’s competitiveness in the global EV supply chain. Relative to its lofty mid-term ROCE target of >12.5% (~20% for catalysis) per this year’s CMD, though, the company has a long way to go. For context, the company sustained pre-tax ROCEs in the low-teens % pre-2021, while the catalysis segment also sustained through-cycle ROCEs in the low-teens %.

Sharing the capex burden with PowerCo will help, though the 50/50 revenue split, despite Umicore taking on full operational responsibility, does dilute the return potential somewhat. And while take-or-pay offtake commitments are in place for a substantial portion of the capacity, these are non-exclusive, and both sides have the flexibility to negotiate alternatives. Going forward, all eyes will be on execution within the cathode battery materials business, with Umicore’s ability to unlock scale and efficiencies key in driving a superior return profile.

Umicore

A Challenging Outlook Amid Normalizing Metals Prices

In the near term, the biggest headwind remains precious metals prices, which continue to trend lower YoY. The decline looks set to extend into the coming quarters as well, given the emerging signs of weakness in global demand. Of note, manufacturing PMIs have been moderating, while easing supply chain tightness has led to supply/demand coming back into balance over the past year. This implies Umicore will need to contend with a moderation in chemical prices and narrowing spreads from the recent upcycle, implying earnings downside ahead.

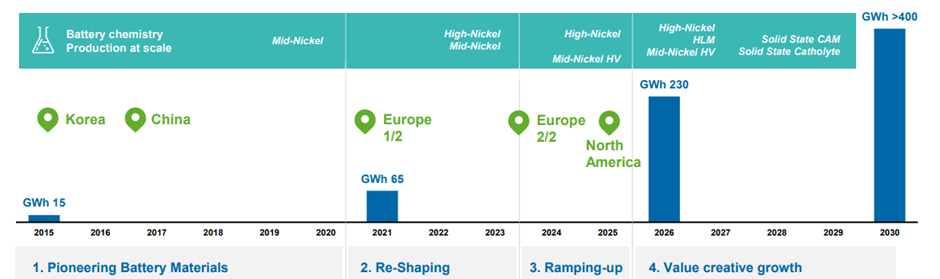

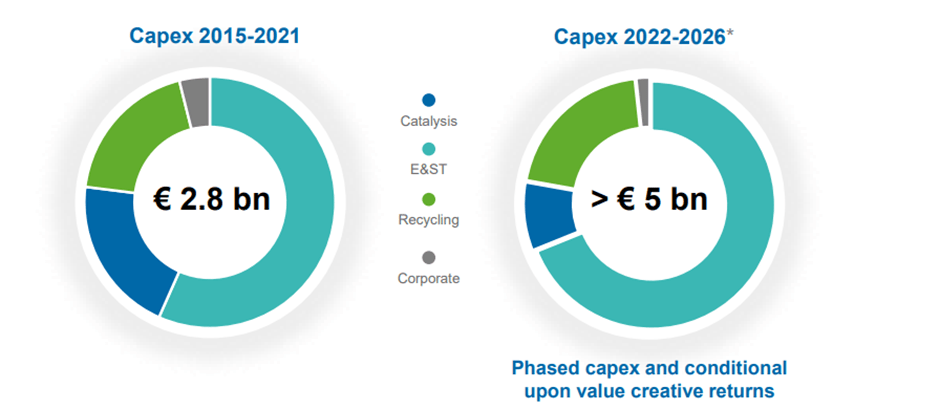

Yet, Umicore still expects a volume ramp-up from H2 2023 in its cathode active battery materials business. Hitting this milestone is a key part of its ‘Umicore 2030 – RISE’ strategy, which is guided to drive revenues to more than double through 2030 on ambitious expansion plans. The plan was put together in a different interest rate environment, though, so the front-loaded capex outlay of >EUR5bn over the next five years could see delays or downward revisions ahead. With competition also a key factor amid narrowing industry margins, I am concerned about the viability of the planned expansion. Pending better visibility into the execution and news flow regarding order take-up by EV battery manufacturers, I would be cautious about underwriting the growth plan.

Umicore

EV Transition Journey Remains Fraught with Risk

Over the long run, the company’s progress in the battery materials/battery recycling growth area is commendable, but the level of competitive intensity here is high. As reflected in key peer Johnson Matthey’s valuation de-rating in recent months, the market is asking serious questions about the return potential from these growth investments, particularly relative to higher financing costs. For Umicore, balancing the funding needed for the transition to EVs with the future deceleration in its legacy auto catalyst and platinum group metal refining/recycling businesses (>60% of the overall contribution) will be tricky.

Not only will the auto catalyst business see weaker volumes as the EV transition gains traction, but with new internal combustion engine (ICE) platforms also set to decline significantly, Umicore could see a structurally more competitive environment and, by extension, increased pricing pressure as well. While the liquidity position should be enough to get over the near-term hurdles, I wouldn’t rule out the possibility of a capital raise sooner rather than later, particularly if the company sticks to its significant >EUR5bn capex target.

Umicore

Staying Neutral Despite Another Deal Win

Umicore has scored a few contract and MoU wins in recent months, most notably via the Volkswagen JV, but the ROIC implications are less clear, in my view. The company’s growth markets are competitive, and with limited differentiation heading into a period of macro uncertainty, achieving the mid-term targets in battery materials/recycling could prove challenging. So while the JV structure should help alleviate the capex burden, the prospect of below-par returns on significant growth investments could lead to funding risks down the line.

At the current relative premium to key peer Johnson Matthey, the stock isn’t cheap either. Pending better visibility into the execution progress and the cathode battery materials demand trend heading into the H2 2023 ramp-up, I would remain sidelined.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment