jetcityimage

Investment Thesis

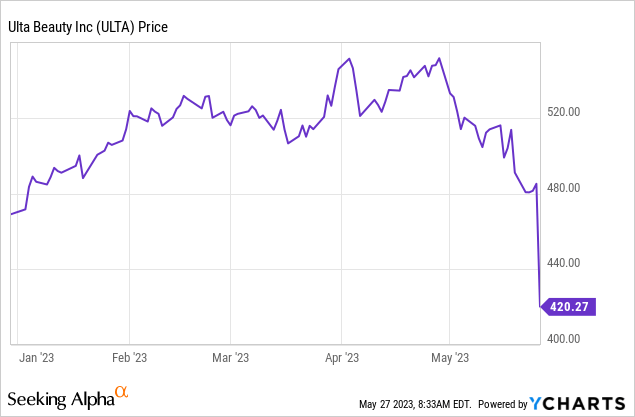

Ulta Beauty (NASDAQ:ULTA) has dropped nearly 25% in less than a month, as investors weigh on the company’s latest earnings report and the negative outlook from other retailers such as Foot Locker (FL). I believe the rapid decline actually presents a rare buying opportunity for the long-term compounder.

The latest earnings were solid with revenue up double digits despite facing the weakening consumer sentiment. There is some discussion in regards to the impact of theft but I believe this is a relatively easy and straightforward issue to fix. The company’s valuation is also very compelling, with multiples trading near historical lows. I believe the current price point should offer ample upside potential; therefore, I rate the company as a buy.

Q1 Earnings

Ulta Beauty announced its first-quarter earnings last week and the market reacted very negatively. However, I personally think that the print is solid when considering the current macro backdrop. The company reported revenue of $2.63 billion, up 12.3% YoY (year over year) compared to $2.35 billion. Cosmetics is by far the largest segment, contributing 44% of total revenue. This is followed by the Skincare and Haircare segments, which account for 19% and 18% of total revenue respectively.

Comparable sales accounted for 9.3% of the revenue growth while new store openings contributed the remaining 3%. The growth in comp sales was mainly driven by the 11% increase in transactions amid higher foot traffic, partially offset by a 1.5% decline in average transaction size.

Gross profit increased 12.1% YoY from $941 million to $1.05 billion, while the gross profit margin dipped 10 basis points from 40.1% to 40%, largely due to an unfavorable product mix. The bottom line was relatively weak due to the increase in spending. SG&A (selling, general, and administrative) expenses as a percentage of sales grew 180 basis points from 21.4% to 23.2%. This is due to increased marketing efforts, higher payroll expenses amid an increase in employees, and other investments.

This resulted in the net income up 4.7% YoY from $331.4 million to $347.1 million. The net income margin slipped 90 basis points from 14.1% to 13.2%. The diluted EPS increased 9.2% from $6.30 to $6.88, as share buybacks reduced the number of outstanding shares. The results are good enough in my opinion, especially with revenue up double digits. The bottom line was a bit underwhelming but the company could easily cut down on spending to boost it, hence I am not too concerned at the moment.

Inventory Shrinkage

Inventory shrinkage has been a trending topic among many retailers lately and Ulta Beauty is also being affected. The company recently reduced its operating margin guidance from the range of 14.7%-15% to 14.5%-14.8%, citing the rising number of theft and organized crime. However, I do not think this will be a long-term concern as the management team is already acting on it, primarily by increasing the number of security and employees, and better collaborating with local law enforcement. These efforts should be able to stop or at least slow down the shrinkage moving forward.

Scott Settersten, CFO, on inventory shrinkage:

As Dave shared earlier, we continue to experience a worsening trend of theft and organized retail crime. We are actively working to stabilize and mitigate these trends through investments in staffing, training, and fixtures, and we are working collaboratively with law enforcement and third-party organizations to address these challenges.

Attractive Valuation

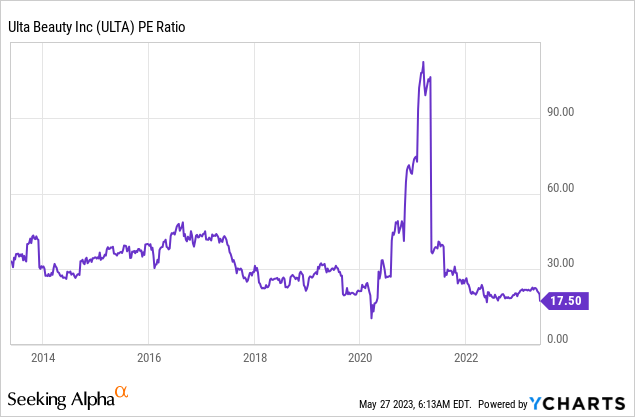

After the recent decline in share price, Ulta Beauty’s valuation is looking very attractive in my opinion. The company is trading at a PE ratio of just 17.5x, which is meaningfully below both its historical average and peers. From the first chart below, you can see that the current multiple is near the bottom of its historical range, only slightly above the unprecedented drop during the pandemic. This represents a significant discount of 46.6% compared to its 5-year average PE ratio of 32.8x.

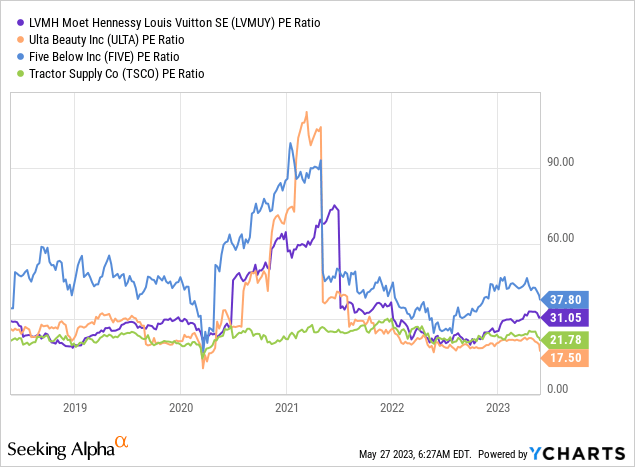

As shown in the second chart below, Ulta Beauty is also cheaper than other notable specialty retailers such as Tractor Supply (TSCO), Five Below (FIVE), and LVMH (OTCPK:LVMUY) (I am including LVMH as the company owns Sephora, which is Ulta’s largest competitor). The company is trading at a 42.1% discount compared to the peer group, which has an average PE ratio of 30.2x. I believe the huge valuation gap is unjustified as the company’s latest revenue growth of 12.3% is basically in line with peers’ average growth rate of 12.9%.

Investors Takeaway

Overall, I believe the market is overacting to the latest earnings by Ulta Beauty. Revenue growth was very solid considering the current backdrop and the bottom line still grew 5% despite higher spending. Inventory shrinkage is a concern in the near term but I do not think the impact will last too long, especially with more security-related initiatives being implemented.

The most notable risk at the moment is still the ongoing uncertainty in the economy. Due to the company’s business nature, it will no doubt be impacted if we enter a recession in the coming months. However, the discounted valuation should offer a solid margin of safety, and its potential downside should also be meaningfully less than peers. I believe the current risk-to-reward ratio is very compelling and I rate the company as a buy.

Be the first to comment