miniseries

Investment Thesis

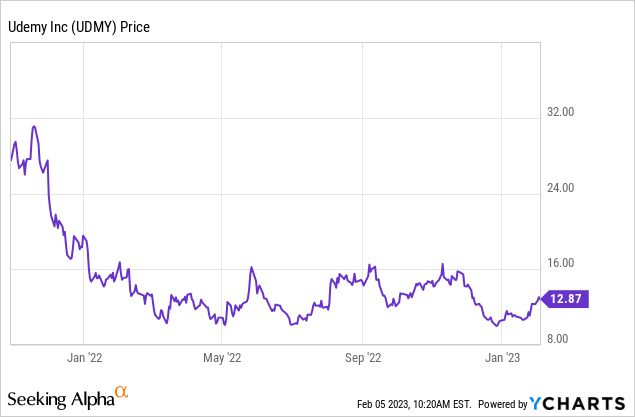

Udemy (NASDAQ:UDMY) went public at possibly the worst time. The company IPOd in October 2021 and shares have been dropping non-stop due to inflation worries, rising interest rates, and the lack of appetite for growth companies. It is currently trading at $12.87, down nearly 60% from its all-time high.

However, unlike the share price, fundamentals have not changed and the company continues to grow. Online learning is a massive and expanding market that is providing solid tailwinds thanks to numerous catalysts. Udemy Business is also seeing strong traction and continues to be a huge growth driver. The company is now trading at a compelling valuation with multiples meaningfully below its peers. I believe the current price level offers a good risk-to-reward ratio; therefore, I rate the company as a buy.

Rapidly Expanding Market

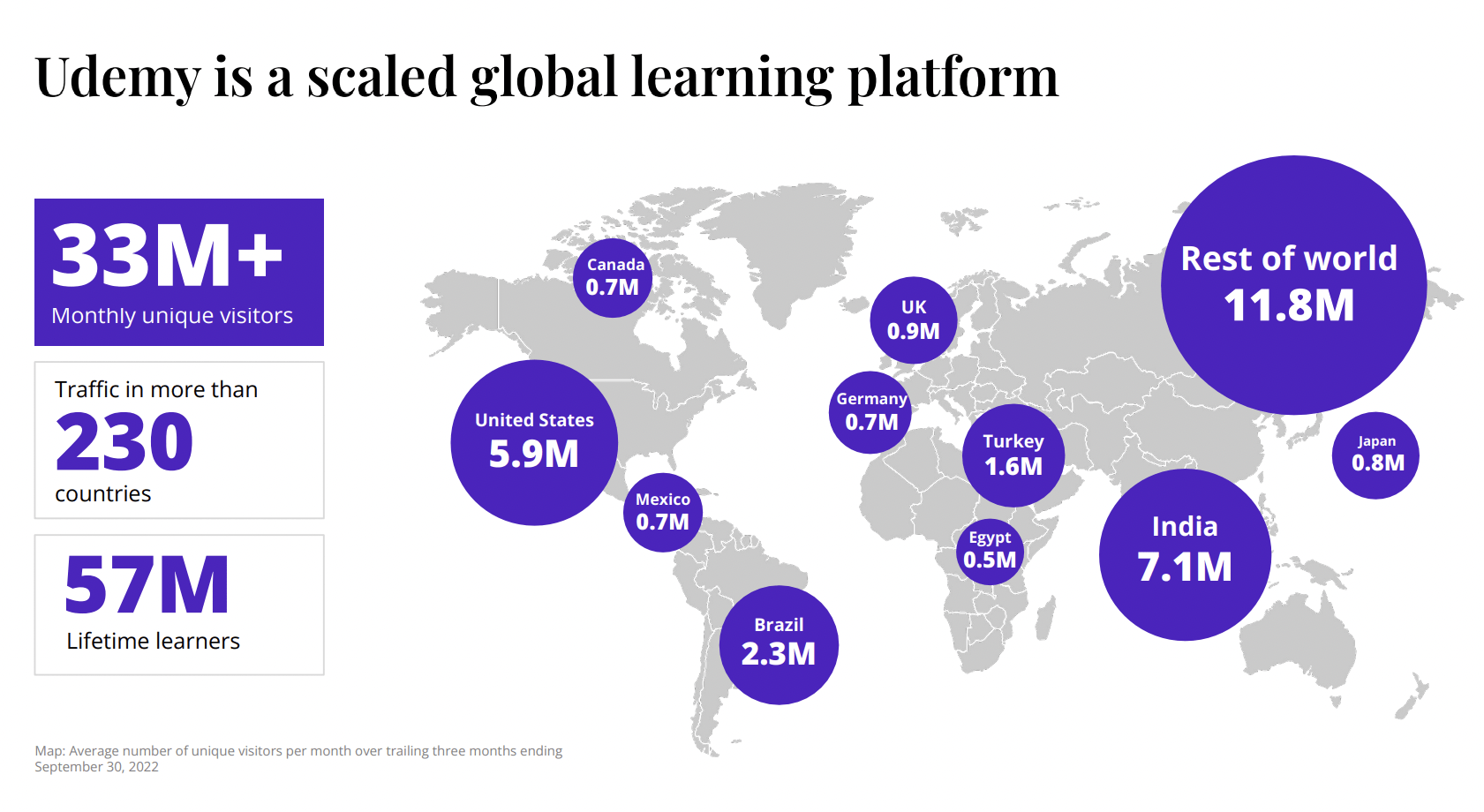

For those unfamiliar with the company, Udemy is an online learning platform founded back in 2010. The company offers a broad selection of courses ranging from coding to music for an affordable price, which often starts at as low as $16.99. It currently has over 200,000 courses in 75+ languages with 57 million lifetime learners. Online learning has gained a lot of traction in the past few years thanks to the pandemic, which forced everyone to stay at home and substantially increased the adoption rate of new communication tools.

Online learning is a huge and fast-growing market. According to Allied Market Research, the TAM (total addressable market) for global online learning is forecasted to grow from $197 billion in 2020 to $840.1 billion by 2030, representing an impressive CAGR (compounded annual growth rate) of 17.5%. For instance, the current penetration rate of Udemy is only less than 1%. Therefore, despite having multiple players in the industry, I believe there is more than enough room for Udemy to grow.

Udemy

There are multiple catalysts driving this expansion. For starters, education is very expensive in a lot of countries and online learning offers a much more affordable alternative, especially for specialized skills. Besides, people who live in remote locations may not be able to attend face-to-face classes or there simply aren’t any learning opportunities nearby. Thanks to much more accessible and reliable internet infrastructures, online learning is the most convenient and viable option.

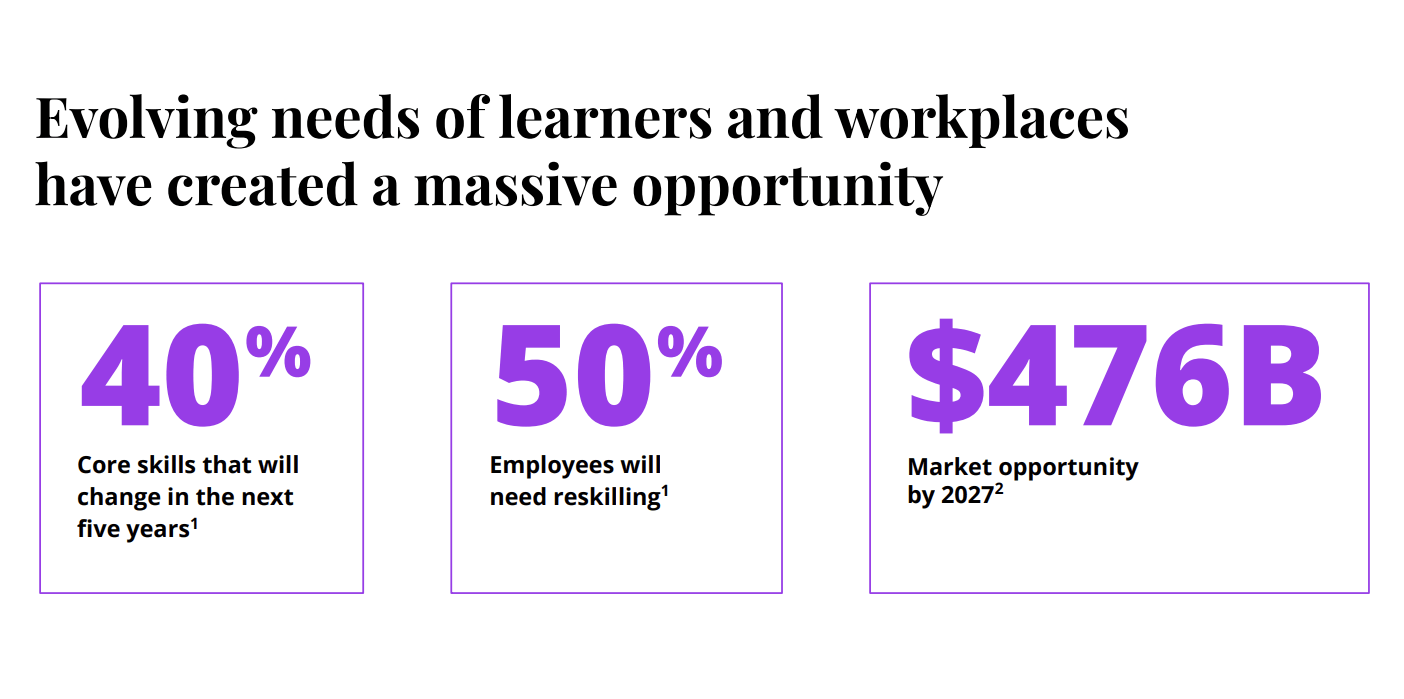

Digital transformation also changed the requirements for many jobs and increased the demand for lesser-known skills like coding. With emerging generative AI tools such as ChatGPT, employees might also want to equip themselves with more skills to increase their competitiveness. According to Udemy, it is estimated that 50% of employees will need re-skilling and 40% of core skills will change in the next five years. I believe these catalysts will continue to support the expansion and provide tailwinds for the company.

Udemy

Udemy Business

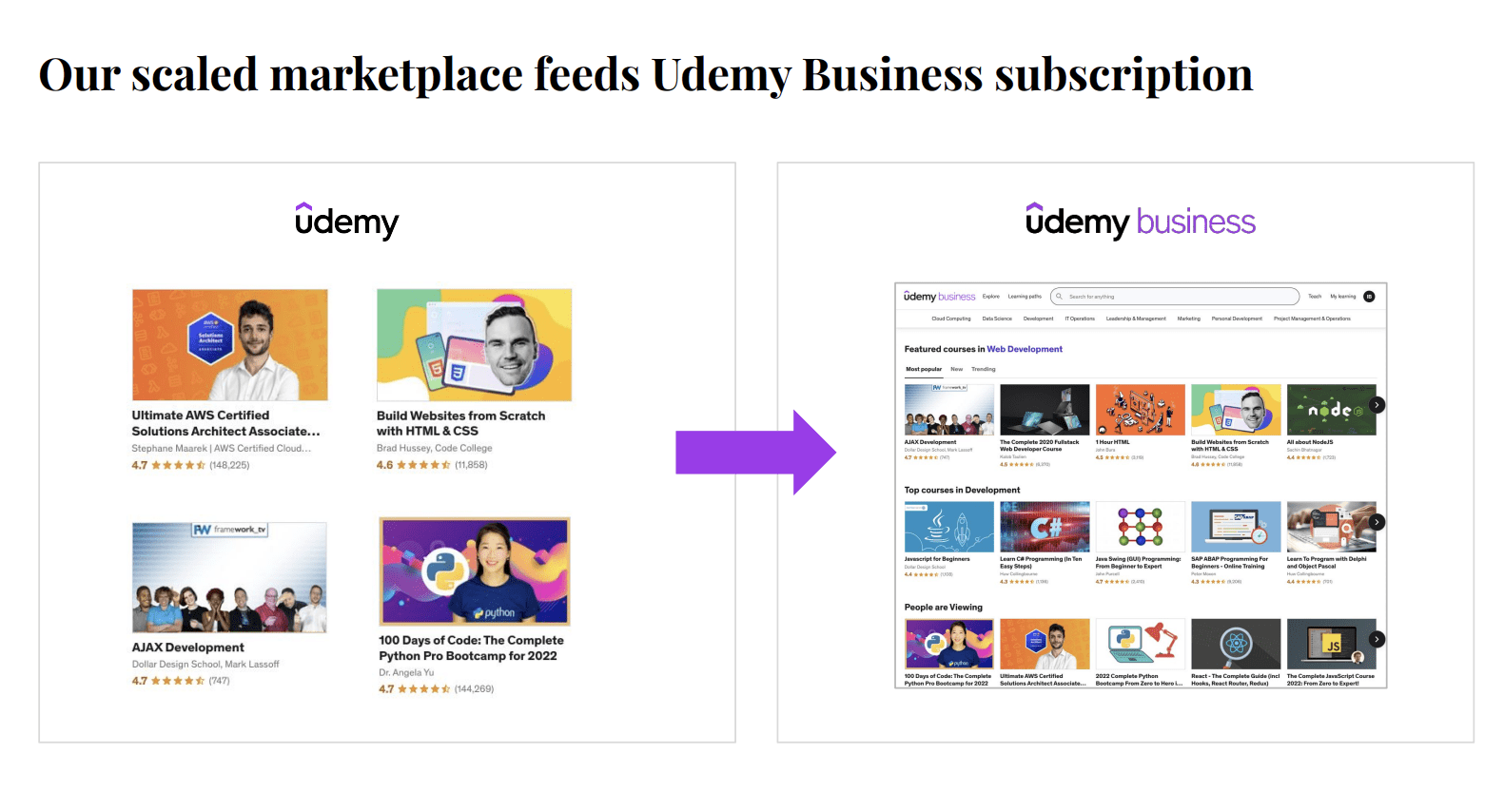

Udemy Business is a subscription product for businesses that give their employee unlimited access to 19,000+ Udemy’s top courses. It comes in different plans such as self-serve, guided, immersive, and cohort learning. The product is seeing strong demand as it allows companies to flexibly train or re-skill employees according to their respective situations. It is also much cheaper and easier than hiring new employees considering the tight labor market and wage inflation. It already onboarded multiple blue-chip customers such as PepsiCo (PEP), Citi (C), Cigna (CI), and more.

Udemy Business significantly strengthens the company. Unlike most normal courses that are purchased individually, Udemy Business operates with a SaaS (subscription as a service) model. This substantially increases margins and revenue stability as payments are recurring. It also presents “land and expand” opportunities with seat expansion or further product upsell. It mostly targets enterprise clients therefore the churn rate is much lower compared to individual buyers as well. I believe the transition to a SaaS-based model should warrant the company with a higher multiple.

The segment has been seeing strong success and driving growth. While the revenue of the consumer segment dipped by 6% in Q3 due to the weakening economy, revenue from Udemy Business actually grew by over 67%, demonstrating the strong resilience of enterprise customers. The number of customers was up over 40% to 13,437 and the net dollar retention rate was 117%. Gross margins improved 190 basis points to 67.2% and ARR (annual recurring revenue) amounted to $350.4 million. The segment now accounts for over 50% of total revenue. I believe Udemy Business will continue to be a huge growth driver moving forward.

Udemy

Investors Takeaway

I believe Udemy is currently mispriced. The company has a large and growing addressable market that provides it with tailwinds while Udemy Business is a strong growth driver with expanding margins. Yet, the market is not valuing its potential accordingly. After the massive drop in share price, the company’s valuation is quite compressed. It is currently trading at a PS ratio of just 3.05x which is very cheap (I am using the PS ratio as the company is not yet profitable). The multiple is way below online education peers such as Coursera (COUR) and Duolingo (DUOL), which are trading at 4.69x and 11.53x, respectively. This represents a whopping 53.8% discount compared to Coursera yet they are actually growing revenue at similar rates. I believe the valuation gap should start to close if Udemy continues to execute which will offer solid upside potential. The huge discount also offers some margin of safety as a lot of pessimism is likely priced in already. I like the risk-to-reward ratio at current price levels; therefore, I rate the company as a buy.

Be the first to comment