da-kuk

Dollar Dynamics in 2022

After rallying for much of 2022 on the back of aggressive Federal Reserve interest rate hikes, the U.S. dollar has sold off since its September peak. There is a voluminous academic literature, dating back at least to Fama (1984), which discusses how interest rate differentials forecast future relative currency returns. An additional dynamic is the contemporaneous relationship between a country’s interest rates and its currency. For developed economies, with little sovereign default risk, higher current (and anticipated) interest rates in country A appear to lead to contemporaneous currency appreciation of A relative to lower interest rate countries.

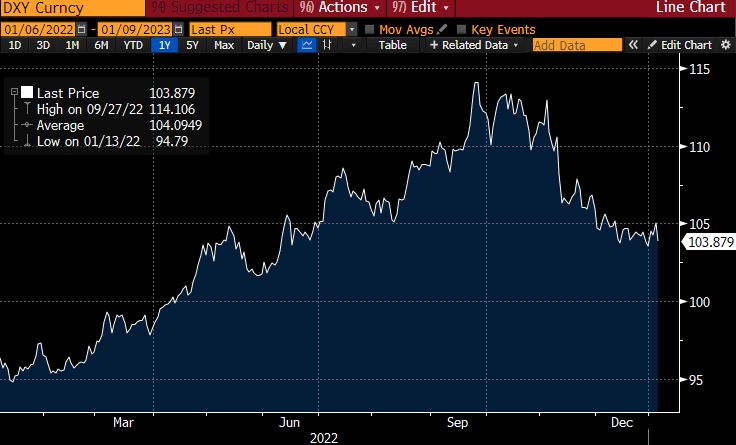

The trade-weighted dollar (Bloomberg)

Under this interpretation, the trade-weighted dollar (DXY) rallied because the Fed was the first of the major global central banks to tighten policy in response to inflationary pressures. As inflation started to come under control in the U.S., and as other global central banks began to tighten policy, the differential between U.S. rates and those of other developed markets began to shrink, and the dollar started to depreciate against a basket of global currencies. If the interest rate differential continues to favor other countries — higher rates there versus those in the U.S. — the dollar may continue to depreciate.

U.S. Versus International Stocks in 2022

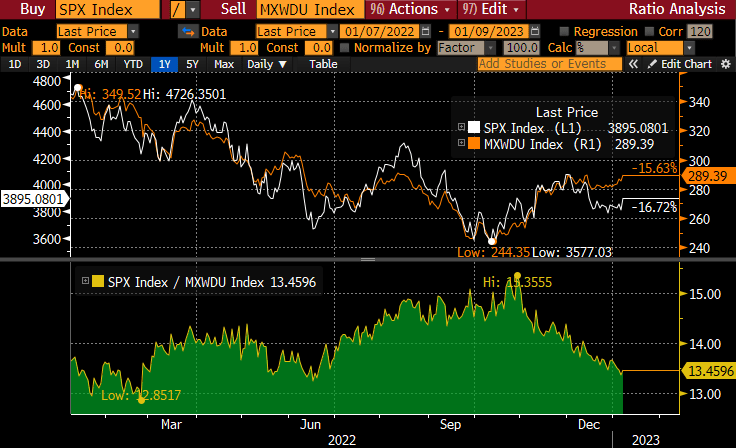

The relative performance of U.S. versus international stocks has mirrored the dollar’s path over the course of 2022. The next chart shows the S&P 500 (SPX) index and the iShares MSCI All-Country World Index ex-U.S. (ACWX), a globally diversified stock market index, expressed in U.S. dollar terms, which excludes all U.S. stocks. The ratio of the two indexes (bottom panel) shows that the S&P 500 outperformed international stocks in 2022 up until October, and since that time, U.S. stocks have been the laggard.

S&P 500 (SPX) versus MSCI World ex U.S. (MXWDU) index (Bloomberg)

Comparing the ratio of the two indexes (bottom panel) to the trade-weighted U.S. dollar suggests that the main driver of U.S. stock underperformance appears to dollar weakness. From the point of view of a U.S. investor, owning international stocks entails exposure to international stock price fluctuations in their domestic currencies, as well as to the exchange rate of those domestic currencies against the U.S. dollar. When the dollar depreciates against foreign currencies, this gives a tailwind to international stocks held by U.S. investors, because those stocks mechanically appreciate in dollar terms.

This isn’t the full story, however, if the weakening dollar is a consequence of a Fed that is likely to start easing, or at least become less restrictive, sooner than other global central banks. Such easing would allow the U.S. economy grow more quickly than international peers. If this happens, then the growth of U.S. corporate earnings will also outpace the earnings growth of international firms.

The State of the Global Central Bank Hiking Cycle

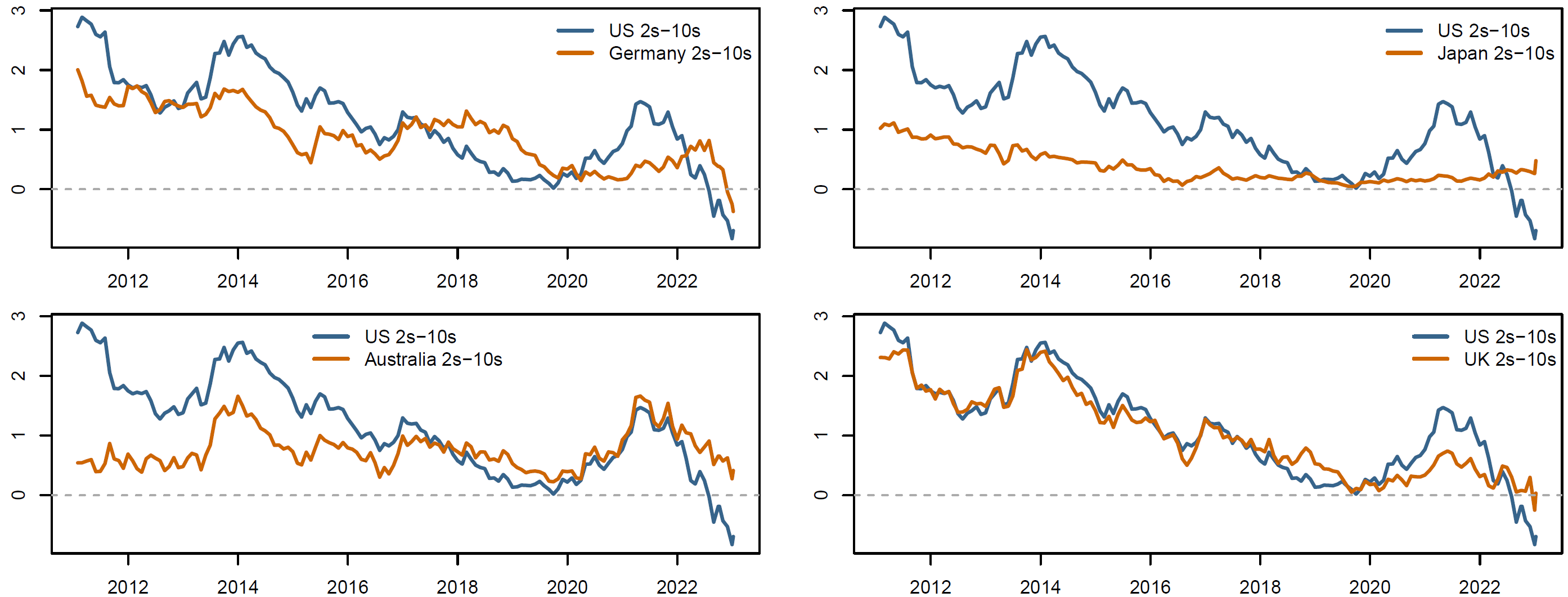

To get a sense of where global central banks stand in their tightening cycle, the next figure shows the U.S. 2s-10s curve (10-year government bond yields minus 2-year government bond yields) alongside those from the U.K., Germany, Australia, and Japan. The U.S. 2s-10s curve is considerably more inverted than the 2s-10s curves of these other countries.

U.S. and global 2s-10s curves (QuantStreet, Bloomberg)

2-year rates reflect anticipation of short-term central bank policy, whereas 10-year rates reflect longer term growth and inflation expectations. When the 2-year rate is far above the 10-year rate, monetary policy is highly restrictive. As the figure shows, the Fed has already done much more of the tightening work than its global peers have.

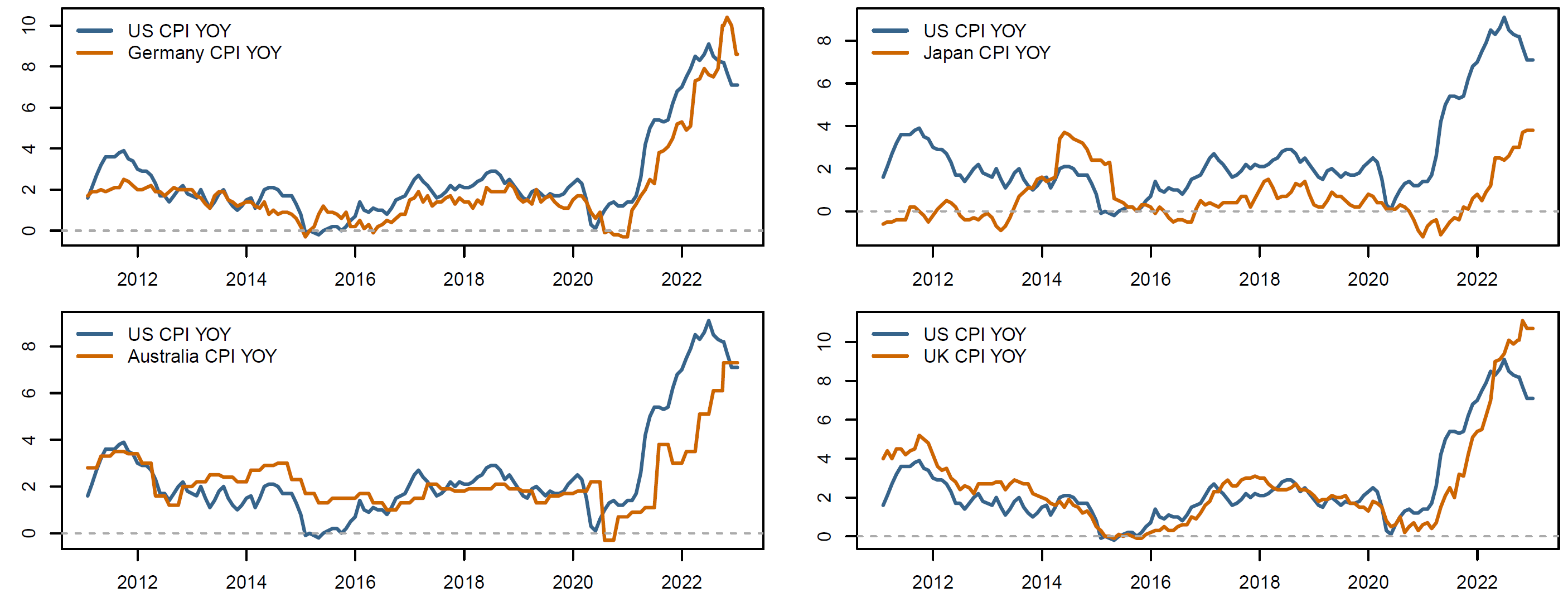

The other important dynamic is that U.S. year-over-year CPI inflation has turned down, whereas the comparable inflation measures in other countries continue to increase, or at least decrease less quickly.

U.S. and global last year-over-year inflation (QuantStreet, Bloomberg)

The takeaway is that the U.S. is several months or quarters ahead of other countries in its battle against inflation. This suggests that U.S. monetary policy will likely start to ease ahead of other countries, which in turn means U.S. economic growth is likely to accelerate sooner than growth in U.K., Germany, Japan, and Australia.

Back to Stocks

When U.S. investors buy international stocks, they have exposure to three return drivers: (a) the exchange rate of the U.S. dollar against international currencies; (b) the price multiple (e.g., P/E) of international stocks; and (c) the earnings (E) of international stocks. If, because of relative monetary policy trends, the dollar continues to depreciate against foreign currencies, (a) by itself will cause the dollar price of foreign stocks to increase.

Let’s assume that P/Es of U.S. and foreign stocks will not change in the year ahead (it is also possible with lower relative rates, the P/E channel will also favor U.S. stocks). The relative performance between these two asset classes will then be determined by (a) versus (c). Will U.S. corporate earnings growth relative to that of international stocks outpace the depreciation of the U.S. dollar? First, some people (e.g., Goldman (GS) and JPMorgan (JPM)) believe that the U.S. dollar won’t depreciate further in 2023. Second, based on the relative positioning of the U.S. in the global economic cycle, it seems likely that the Fed will begin easing well ahead of other central banks, which will allow U.S. economic and earnings growth to outpace that of other developed market economies.

Betting on U.S. stocks relative to their global peers means betting on U.S. relative earnings growth outpacing the rate of U.S. dollar depreciation. This seems like a bet worth making.

Be the first to comment