benedek

Apartment REITs are among the best positioned for an inflationary environment due to their short term leases, and yet many of them have fallen materially over the past year. Presenting decent opportunities for value-minded investors.

This includes Camden Property Trust (NYSE:CPT), which as seen below, is down by 32% over the past year, and trades far closer to its 52-week low than its high of $175. In this article, I highlight why now presents a good long-term buying opportunity on this high-quality REIT.

CPT Stock (Seeking Alpha)

Why CPT?

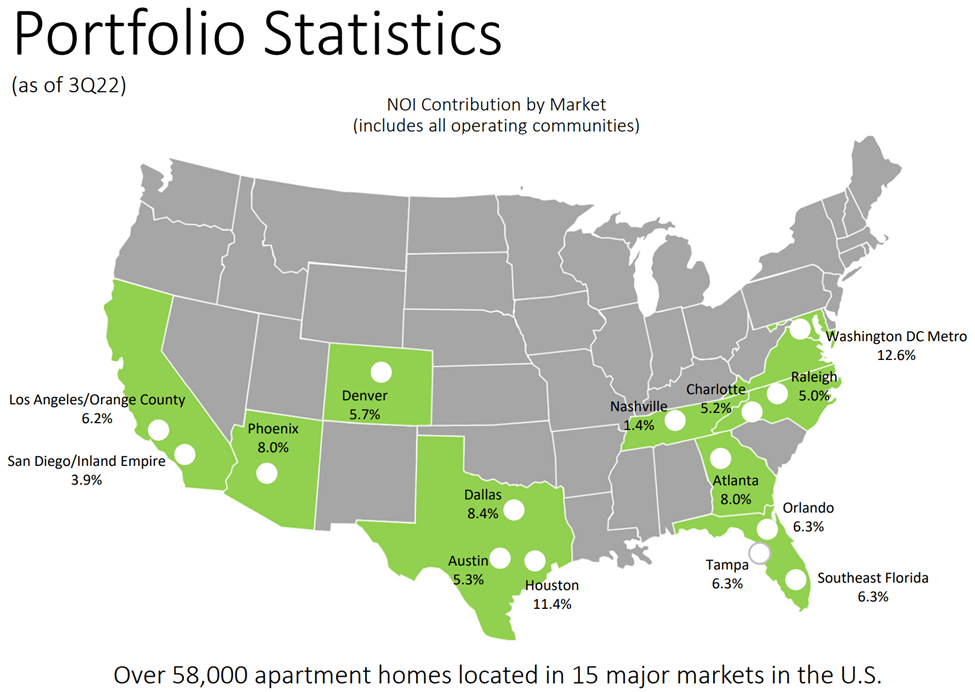

Camden Property Trust is a premier Apartment REIT that’s a member of the S&P 500 (SPY) Index. It owns a high-quality portfolio of 171 properties containing 58K apartment homes across the U.S. It’s led by CEO Ric Campo, who’s been with CPT for over 30 years, since its pre-IPO period.

Unlike large peers AvalonBay Communities (AVB) and Equity Residential (EQR), CPT is primarily focused around secondary markets, where it sees less competition for deals. As shown below, CPT has healthy exposure to the growing Sunbelt region of the U.S., which is attracting a high number of retirees seeking warmer climates.

CPT Property Locations (Investor Presentation)

Meanwhile, CPT’s underlying portfolio is healthy with a 96.6% occupancy rate during the third quarter, down just 60 basis points over the prior year period. At the same time, tenant demand appears to be rather strong, with a blended lease (new and renewal leases) spread of 9.7%.

Notably, CPT is also seeing strong operating leverage. This is reflected by same property revenue growing by 12% YoY during the third quarter, far outpacing the 4% expense growth that it saw over the same time period. this resulted robust 16% net operating income growth at the same property level.

Importantly, CPT carries a very strong A- rated balance sheet, with a net debt to adjusted EBITDA ratio of just 4.2x, sitting well under the 6.0x level that rating agencies generally consider to be safe. Its weighted average interest rate is just 3.7% and it’s also well positioned for a rising rate environment, with 94% of its debt being locked in at fixed rates. The majority of CPT’s debt (86%) is unsecured and it has full availability under its $1.5 billion unsecured line of credit.

The strong balance sheet goes a long way in supporting its 7 properties currently under development, which provides another source of incremental growth beyond rental increases. Upon completion, this would raise CPT’s total property count by 4% to 178 properties

Risks to CPT include potential for new supply in its core markets. However, management thinks that it should still be able to raise rents, as highlighted during the last conference call:

Sure, supply in ’23 is definitely going to be out there. And with decent job growth and migration to our markets, we think that’s going to continue. And so we should be able to continue to raise rents during that period barring some big economic issue obviously that could be out there on the horizon. But we feel pretty good about the number of units that we observed in 2022 and think that 2023 should be a decent year even with the supply coming in.

And 2023 is going to be a really good year. I think, even in a slowing market we’re still going to have decent rent growth. And I think we have a great embedded start for the year, so when you start thinking about cash flow growth in 2023, it’s going to be better than it is on average, but probably a lot slower than 2022, but that should have some benefit in terms of keeping values from falling dramatically more than they have already.

Importantly, CPT now yields 3.3%, and the dividend is well covered by a 48% payout. CPT raised its dividend by 13% last year and while I wouldn’t expect as big of an increase this year, I would expect it to be above CPT’s historical growth rate of around 5%.

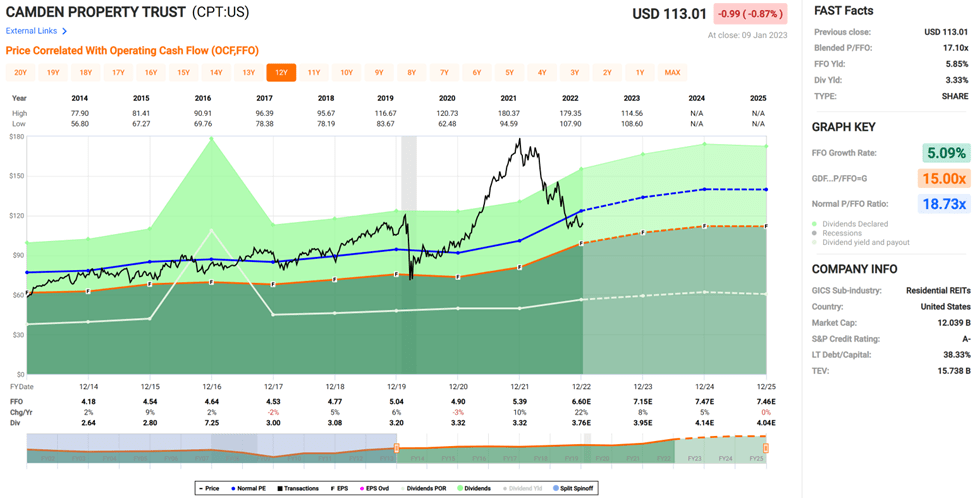

Lastly, I see value in the stock at the current price of $112.76 with a forward P/FFO of 17.1, sitting below its normal P/FFO of 18.7 over the past decade. As such, I find CPT to be reasonably attractive considering its strong fundamentals and forward growth prospects. Analysts have a consensus Buy rating on the stock with an average price target of $137, implying a potential 24% total return including dividends.

CPT Valuation (FAST Graphs)

Investor Takeaway

Camden Property Trust is a high-quality Apartment REIT with robust fundamentals, attractive risk/reward profile and growing dividend. Its underlying portfolio is healthy and tenant demand appears to be strong, and it maintains a very strong balance sheet to support properties under development. The stock trades at a reasonable valuation and pays a very well covered dividend, making it a sound buy for long-term income and growth investors alike.

Be the first to comment