Vladimir Zapletin

Thesis

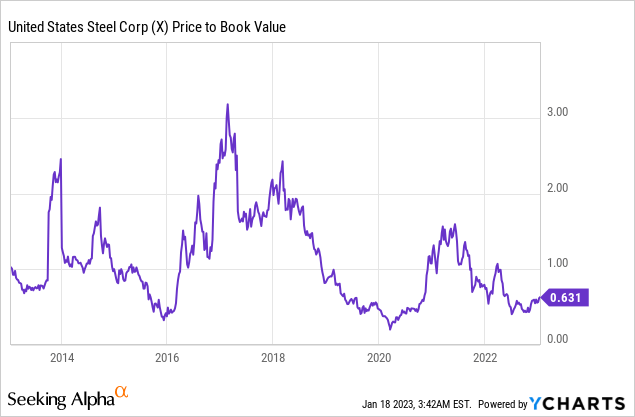

United States Steel (NYSE:X) is trading at just 0.64x book value despite having a dramatically improved balance sheet. They have done well to bring on line EAF capacity and have almost finished significant capex projects. Their vertical integration reduces their reliance on global trade partners and gives them more operational flexibility. U.S. Steel will have lower capex requirements once their current projects are completed and they will be able to increase dividends and buy back shares while the company is trading significantly below book value. For these reasons, we believe that U.S. Steel should trade at their book value of $44 a share.

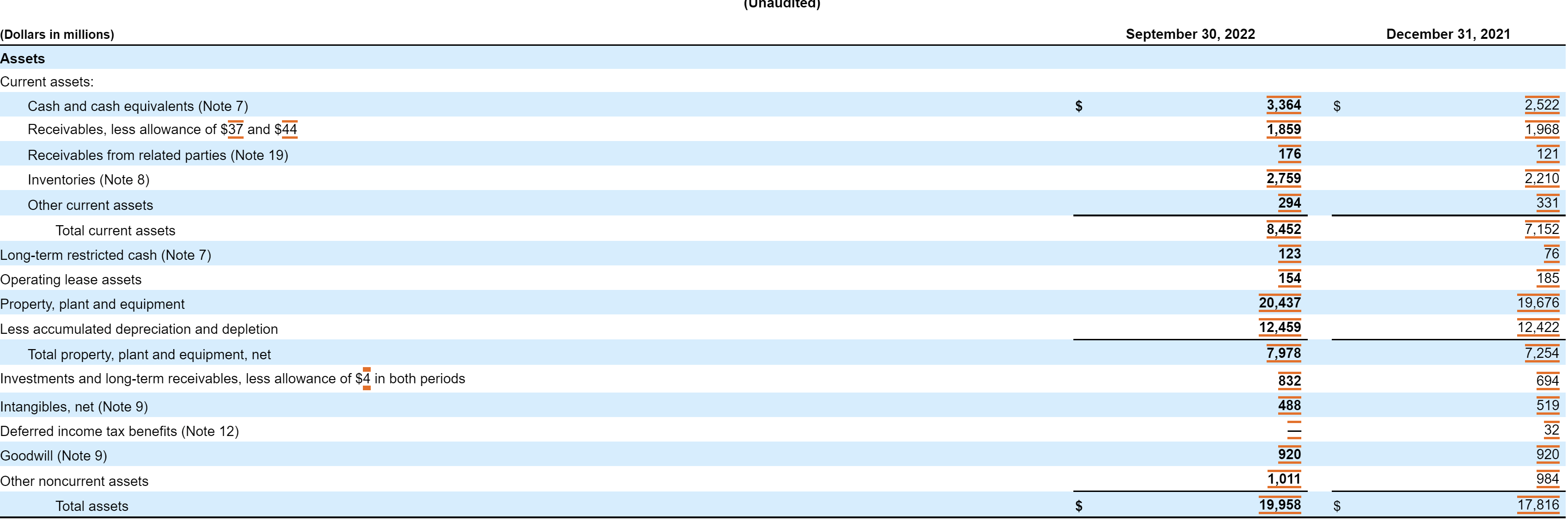

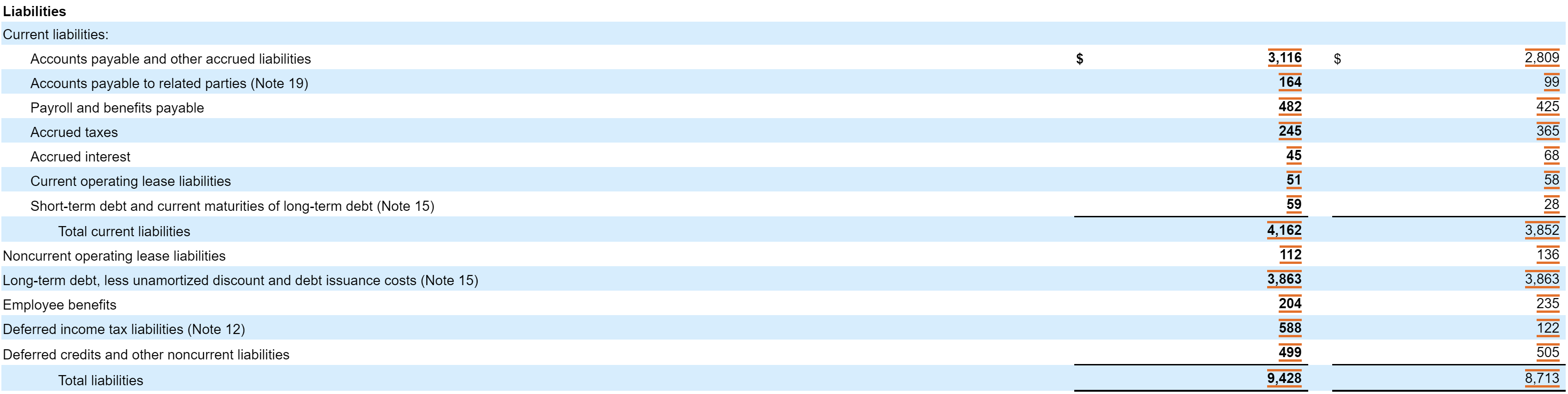

Strong Balance Sheet

U.S Steel has taken advantage of the temporary spike in HRC pricing to clean up their balance sheet. The company has net debt of just $499 million, which is remarkable considering many commodity companies carry high debt loads due to the nature of their business. Their low debt position significantly de-risks U.S. Steel and makes them more resilient to any economic downturns.

Assets (U.S. Steel Q3 Earnings Report) Liabilities (U.S. Steel Q3 Earnings Report)

EAF Capacity

According to their Q3 earnings presentation U.S. Steel is focused on:

Transitioning to a less capital- and carbon- intensive business model while becoming the best steel competitor.

One of the ways that U.S Steel is doing this is by building more EAF capacity. EAF stands for electric arc furnace. EAFs differ from the traditional blast furnaces in many ways.

Steel can be made from 100% scrap metal by using EAFs, leading to a reduced total energy requirement. Blast furnaces must be kept operational for long periods of time while EAFs can be started and stopped depending on demand. The usage of EAFs results in lower carbon dioxide emissions than blast furnaces. EAFs can theoretically be powered using 100% renewable energy.

Electric arc furnaces are an instrumental part of U.S Steel’s plan to become less capital and carbon intensive over time. As far as becoming the “best steel competitor” is concerned, companies that value environmental initiatives would rather do business with U.S. Steel than a steel company relying solely on blast furnaces. U.S. Steel also has more operational flexibility due to EAFs, which could potentially give their customers more flexibility in their own decision making.

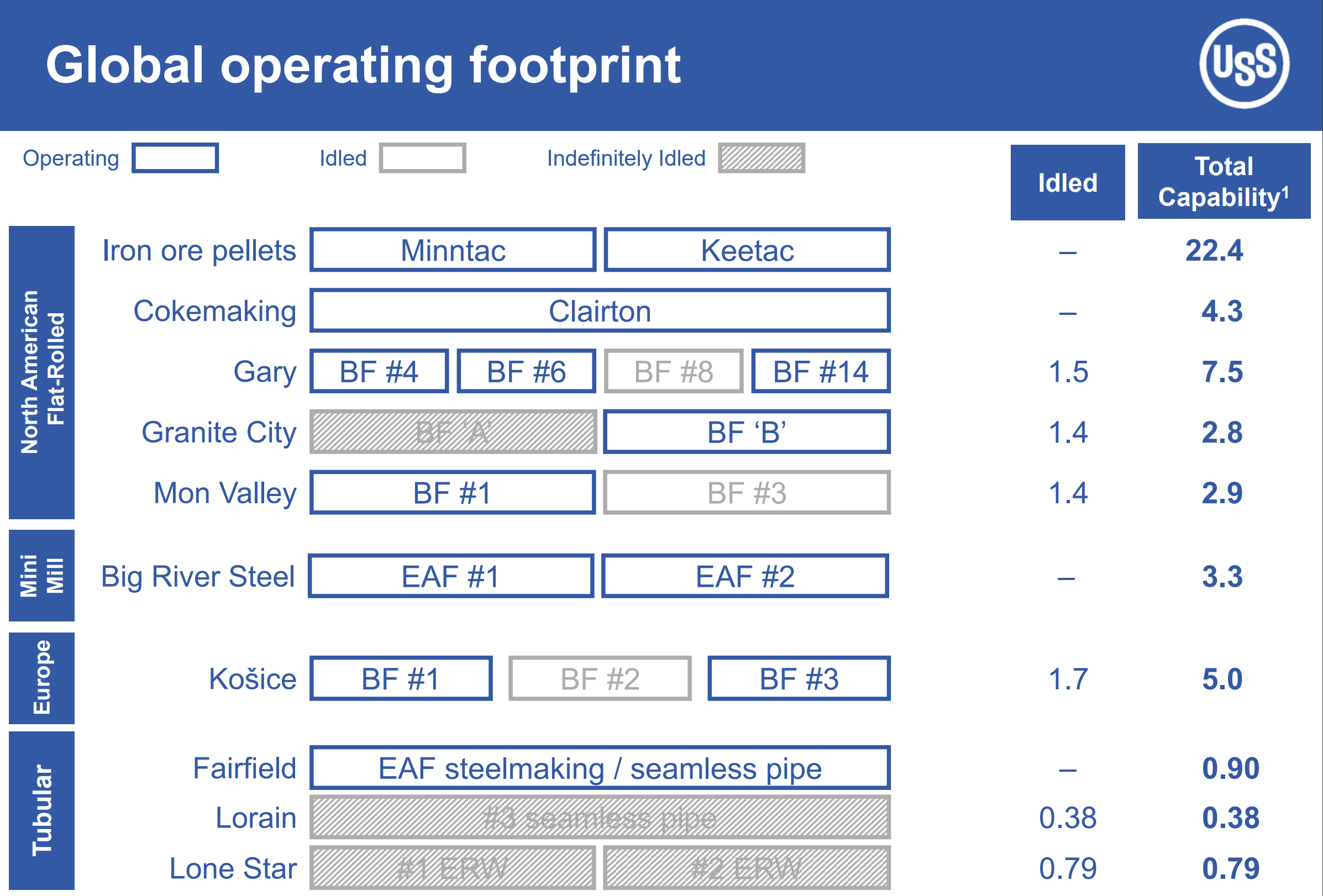

Global Operating Footprint (U.S. Steel Q3 Earnings Presentation)

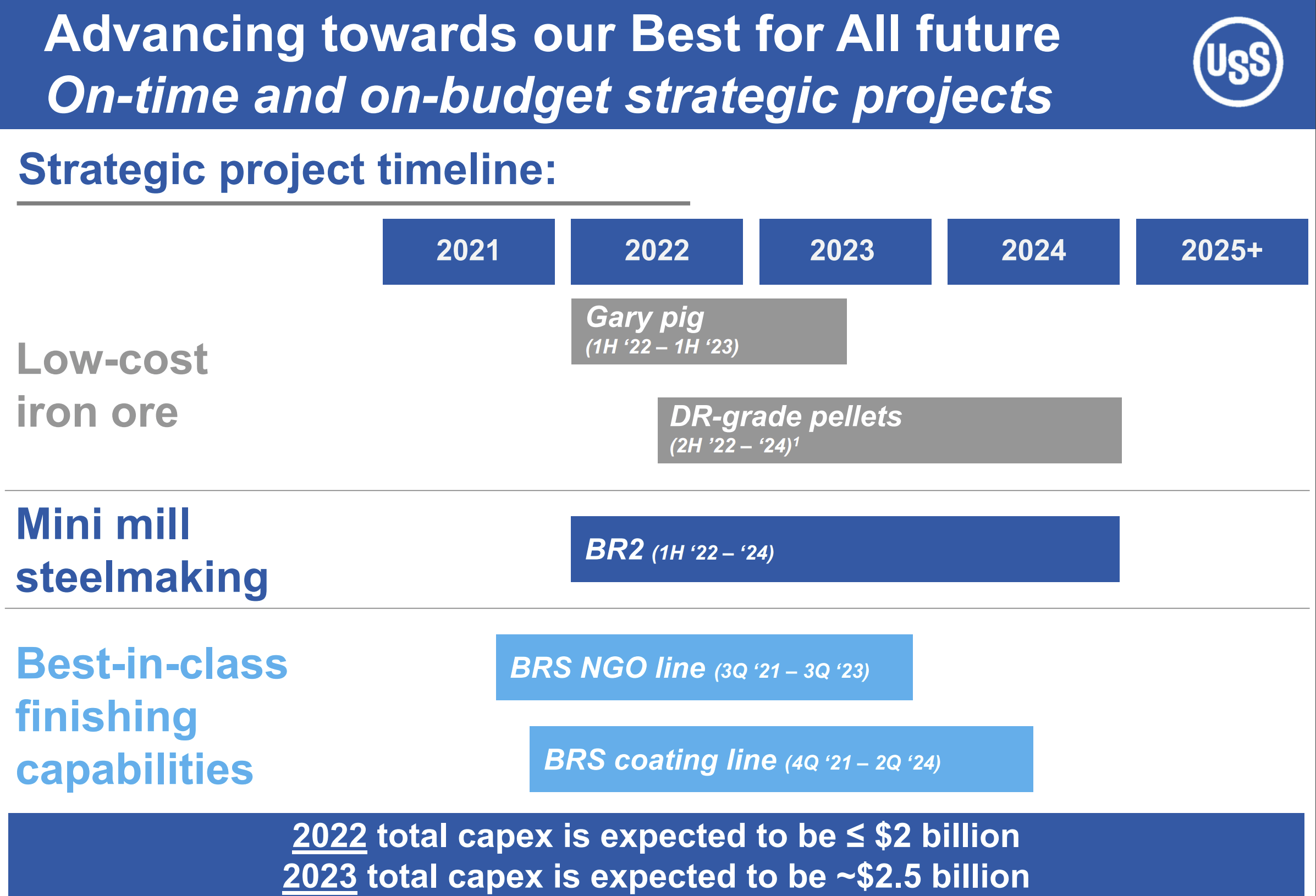

Finishing up Capex

U.S. Steel utilized the short-term spike in HRC pricing to not only strengthen their balance sheet, but also to implement capex spending plans that will improve their future operations.

Capex Plans (U.S. Steel Q3 Earnings Presentation)

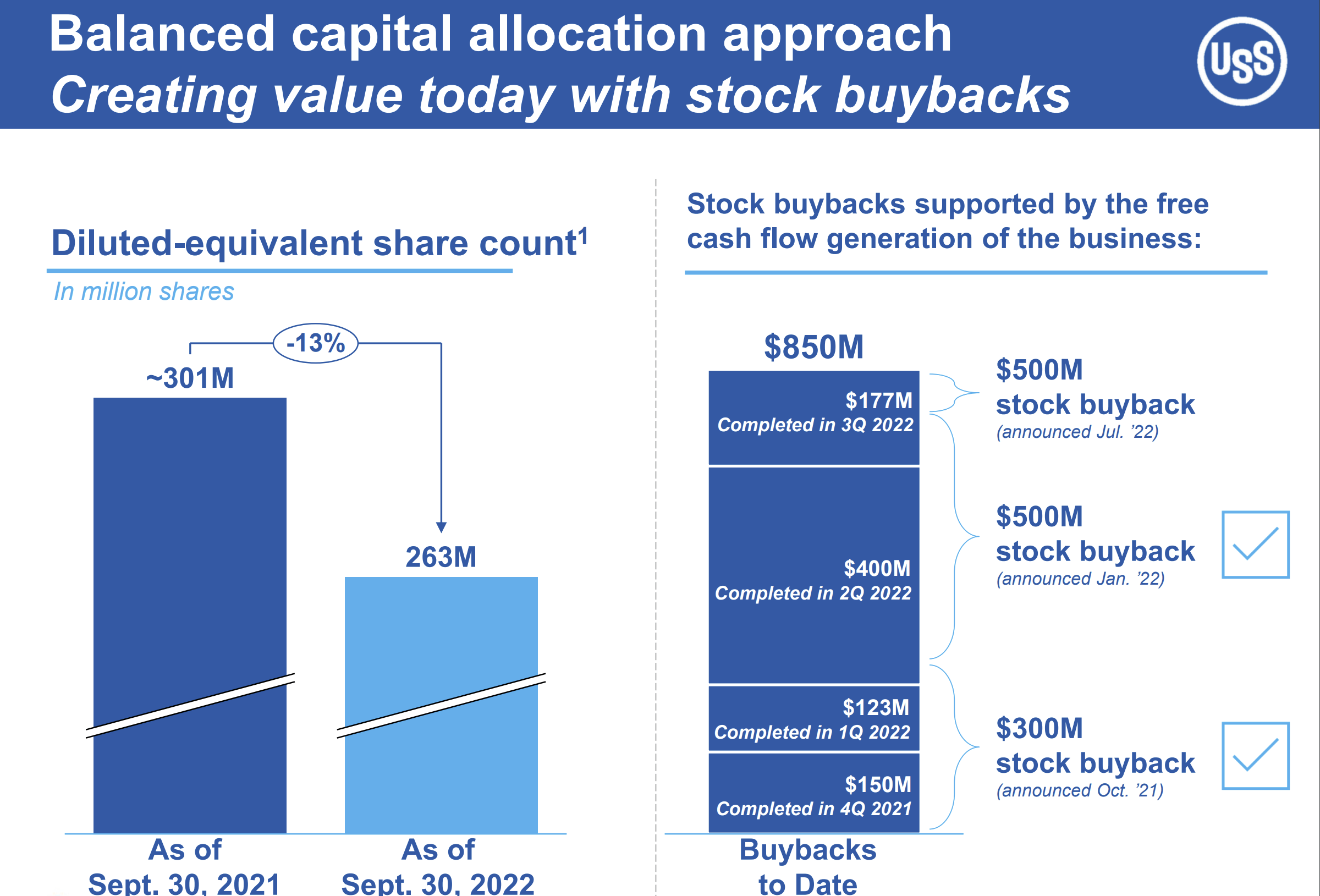

Once this capex is finished U.S. Steel will be in a stronger position to return more cash to shareholders through increased dividends and share buybacks. Now is an especially good opportunity to buy back shares due to the company trading well below book value and the company has been doing just that.

Buyback Information (U.S. Steel Q3 Earnings Presentation)

Vertical Integration

U.S. Steel has extensive mining, steelmaking, and finishing operations. They have managed to capture a large part of the steel value chain and as a result have a lower reliance on outside partners. This improves their operational consistency and flexibility. Customers could view this as a reason to do business with U.S. Steel and may even be willing to pay a premium to do so, granting them a durable competitive advantage.

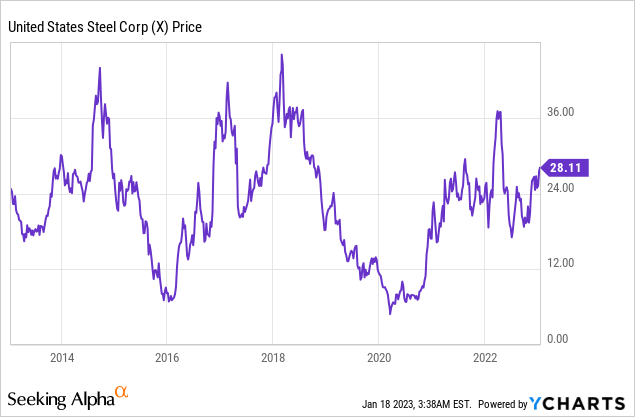

Price Action

U.S. Steel has been a bit of a disappointing performer over the past decade from a stock price perspective. So why should now be the time that U.S. Steel gets appreciation from Wall Street? We believe that the U.S. Steel of today is much better than the U.S. Steel of the past couple of years. The company has fixed their balance sheet and has set themselves up for success going forward through their strategic planning and choice of capital expenditures.

Valuation

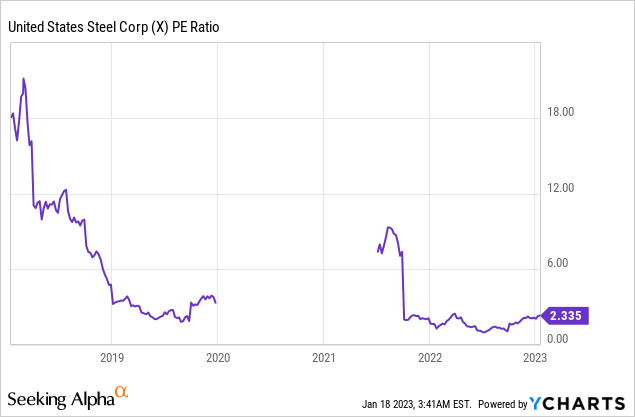

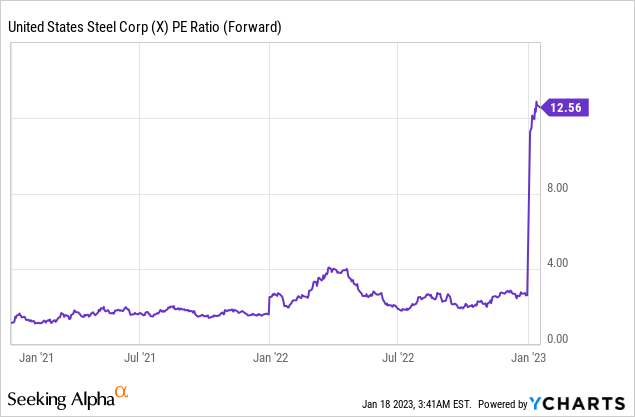

Valuing cyclical commodity companies on a PE basis isn’t particularly useful, however on this metric U.S. Steel looks cheap relative to the market and its own recent history. Earnings are expected to come down over the next year as HRC contract pricing continues to normalize.

We believe that U.S. Steel should trade at its book value of $44 per share. Their strong balance sheet and improved operating position will make them more resilient to macroeconomic pressures and help to shield them from the inevitable downdraft in the cyclical steel industry. The company should be finished with major capex after their current projects are completed and will be able to return more cash to shareholders through increased dividends and/or buybacks.

Risks

U.S. Steel may get outcompeted by other steel companies. This is always a possibility, but U.S. Steel has made an effort to differentiate themselves from other North American steel companies and this should provide them some level of competitive advantage.

Steel companies may get into a price war and U.S. Steel’s margins would be negatively impacted as a result. This is always a risk in highly-competitive commodity markets such as the steel industry, but the nature of supply contracts in the steel industry make a drastic price war relatively unlikely to occur.

The global economy could enter a prolonged contraction, causing HRC pricing to nosedive. This would be terrible for all steel companies and likely result in deep operating losses. Blast furnaces take a long time to restart, so companies typically keep them running even when steel prices are low which results in heavy short-term losses. Since U.S. Steel uses both blast furnaces and EAFs their exposure to this risk is lower than some other steel companies that rely solely on blast furnaces. They can idle their EAFs and mini-mills depending on levels of demand and profitability as well as what type of feedstock is available at the lowest cost.

The risks with companies in commodity industries are materially different than many other sectors of the economy and investors should be prepared for significant volatility. That being said, we view the risk/reward here as being favorable and see somewhat of a floor on the stock price due to the company trading at a PB of 0.64.

Key Takeaway

We believe that the current discount in U.S. Steel is unwarranted and that the company should trade at its book value of $44 per share. The company boasts a strong balance sheet and has done well to position themselves for future success through strategic capital investments. They will be able to return a significant amount of capital to shareholders over the coming years. As long as investors are willing to embrace the volatility that comes with investing in a commodity company, we view the overall risk/reward to be favorable at these levels.

Be the first to comment