Scott Olson

How Did We Get It Right?

In our last article, “Twitter Significant Upside Likely in 2 Years”, we called Twitter “Undervalued” on February 25th, 2022. We were not aware of Elon Musk’s acquisition plan at the time. We, however, coincidentally arrived at the same valuation with Musk’s offer for Twitter. We estimated Twitter’s fair market value should trade at $42 billion vs. Musk’s proposed $43 billion and Twitter’s market value at the time was $28 billion, or $53 per share vs. $54 per share and $34 per share, respectively.

“At 20.8% annual growth as forecasted by Analysts, Twitter should trade closer to 7x 2022 P/S, which translates to approximately $42 billion market capital, representing a potential 55% upside.”

We had the conviction to make the bold call – that Twitter was undervalued by more than 50% – because of three key reasons:

- Twitter was undervalued given its growth trajectory compared to its social media peers

- Twitter’s restructuring to a general manager (“GM”) model was poised to promote ownership and efficiency

- Twitter’s focus on revenue growth under CEO Parag Agrawal’s leadership

In the following analysis, we will very briefly revisit our arguments. For more detail on assumptions discussed, please feel free to visit our previous coverage.

Twitter was undervalued given its growth trajectory compared to its social media peers. Twitter’s 4.8x 2022 forward P/S multiple at the time of our previous coverage implied an annual growth rate of merely 3.5% vs. the mid-20% range guided by management and 20.8% consensus forecast by analysts. Under the consensus annual revenue growth forecast of 20.8%, Twitter should trade closer to a 7x 2022 sales multiple.

We did not assign an “overvalued” or “undervalued” rating based on numeric valuation comparison considerations alone. Our point is that Twitter was priced significantly cheaper compared to other social media stocks such as Snapchat (SNAP) and Match (MTCH) for each percentage of revenue growth that the company was supposed to deliver. We believed the following two points should serve as catalysts to materializing Twitter’s revenue potential:

1) Twitter’s restructuring to GM model was poised to bring more products and features to market with speed, which likely will allow the company to better understand and generate revenue from each monetizable daily active user (“mDAU”) despite adverse impacts to the delivery and tracking of performance digital ads brought by Apple’s (AAPL) App Tracking Transparency (“ATT”) framework.

2) A Revenue Focused Strategy: Twitter has long been criticized for its overemphasis in past years on being a pure social media platform instead of a profitable publicly traded company that can generate returns and value to shareholders. CEO Parag Agrawal promised to align the goals of the company with shareholders by redirecting focus on driving revenue growth.

An example would be the launch of several monetizable products, such as tips, newsletters, and communities , which aim to improve content creator’s ability to generate income. This allows Twitter to generate more revenue by 1) enabling income sharing from content creators, and 2) encouraging greater engagement from users, which then permits Twitter to deliver more relevant and lower funnel ads. These performance-oriented, lower funnel ads come at a higher price, and therefore, allow Twitter to generate greater higher revenue per mDAU.

In short, Twitter was cheap because investors had misunderstood the company’s growth profile by holding its past years of plateaued mDAU growth against the company. We believe however, because of new products in place, Twitter’s mDAU growth will accelerate moving forward, while also benefiting from the increased revenue per mDAU through other new and improved monetizable features. In other words, even if mDAU growth continues to plateau, Twitter will likely print above-consensus revenue as the company generates more revenue per existing mDAU.

What Do We Like and Not Like about Twitter’s Q2 2022 Results?

In the absence of an earnings call for Q2’22 because of the ongoing dispute pertaining to Musk’s potential acquisition of Twitter, we will be sharing our thoughts on the Q2’22 financial results disclosed.

Drawing on the foregoing discussion, we point to three key focus areas for Twitter – 1) mDAU growth, 2) revenue growth, and 3) revenue per mDAU. On the surface, the results from the three core performance metrics were lackluster during Q2’22. However, a deeper dive would unveil that the company remains on track in the turnaround process.

The following analysis will also illustrate why we believe many market participants have likely misunderstood Twitter’s outlook by placing an overemphasis on the company’s recent increase in costs that have reduced operating margins. Specifically, we will explore why we have expected reduced margin for Twitter since Q4’21.

1. mDAU:

For its latest Q2’22 earnings results, Twitter’s mDAU growth printed 14.6% to a total of 238 million.

Twitter mDAU growth has not historically been impacted by seasonality. The metric has been growing consistently at approximate 3% per quarter, or 19% per year from 2019 to 2021.

Twitter benefited significantly when the world went into lockdown due to Covid during Q2’20. It saw one of the most rapid mDAU growth on record at 33.8% when compared to the same quarter in 2019 at 13.9%. Twitter’s Q2’21 mDAU growth rate decelerated but continued to expand near its historical rate of 10.8%.

Twitter’s Q2’22 mDAU is a very positive result as it continues to defy investor’s previous expectations of close to no-growth for mDAU as discussed in earlier sections. The fact that mDAU grew 14.6% year-over-year in Q2’22, even after two preceding years of sustained high growth (average 22%), suggests that Twitter should no longer be viewed as an obsolete, influence-diminishing social media platform. Twitter mDAU grew from pre-Covid levels of 139 million in Q2’19 to 238 million in Q2’22. The incremental add of 100 million mDAU over the past three years is an impressive undertaking that shows acceleration, considering Twitter had previously taken more than a decade to reach 139 million mDAU.

2. Revenue Growth

Twitter reports revenues generated from two segments of operations: 1) advertising revenue, and 2) data licensing revenue.

i. Advertising revenue:

While Twitter’s mDAU growth is not affected by seasonality, revenue is, however. Historically, Twitter sees the strongest sales in Q2 and Q4 due to increased spending in ads during the summer and winter holiday season.

Twitter’s Q1’22 advertising revenue totaled $1.1 billion, which represents growth of 23.11% year-over-year or -21.8% quarter-over-quarter. The sequential advertising revenue decline in Q1’22 was primarily due to:

- Seasonality: Despite Q1’22 advertising revenues declining sequentially by -21.8%, it remains in line with historical trends due to the moderation in advertiser spending coming off of the Q4 holiday season. For example, revenue declined by -22% and -22.9% quarter-over-quarter, for Q1’21 and Q1’20, respectively.

- Sale of MoPub: Twitter completed its disposition of MoPub in January, which generated proceeds of approximately $1 billion that the company will use to self-finance investments in performance ads. The sale of MoPub came at the unfavorable impact of between $200 million to $250 million to annual revenues generated from both advertising and data licensing:

“So, we haven’t broken out MoPub versus MoPub Acquire, the old CrossInstall business. But just to walk you back to what we’ve shared in the past, it was about $188 million of 2020 revenue, about $218 million of 2021 revenue, $50 million going towards $60 million over the course of 2021. The details are in the letter. And we said in the past that 2022 would have been between $200 million and $250 million of revenue.”

For Q2’22, advertising revenue grew -2.76% quarter-over-quarter, and 2.14% year over year. In our interpretation, we attribute this underperformance to two reasons:

- The sale of MoPub: As mentioned earlier, the company tends to perform better in Q2 and Q4 in advertising revenue due to increased spending in ads during the summer and winter months. We will use a proxy to normalized year-over-year comparison post-disposition, since Twitter did not provide a breakdown of segment impacts from its latest sale of MoPub: Advertising revenue represents approximately 91.5% of Twitter’s total revenue. We take the mid-point of the guided impact from the MoPub disposition (between $200 million and $250 million), which is $225 million, and allocate 91.5% of it as a proxy for the pro forma post-disposition impact on advertising revenue. This equates to approximately $206 million. Subtracting the proxy $206 million from Q2’21 advertising revenue of $1.05 billion to compute the normalized year-over-year comparison for Q2’22 advertising revenue, the related figure actually grew approximately 27%, which is in line with previous years’ Q2 growth rate.

- Global economic slowdown: As previously discussed, Twitter’s strategy going forward is to improve revenue growth through delivering more relevant performance-oriented ads. Twitter’s goal was to improve its current performance ads vs. brand ads mix from 30/70 to 50/50. However, at the current stage, Twitter’s ad mix remains brand heavy. SMBs, which are more recession-prone and budget-conscious, usually favor brand ads. Meanwhile, agencies and corporate clients generally place a heavier preference for performance ads. As such, we attribute some of Twitter’s Q2’22 advertising revenue weakness to added broad-based near-term macro headwinds that have placed an unfavorable impact on the company’s current brand ads heavy mix.

ii. Data licensing revenue:

Data licensing revenue following the disposition of MoPub consists of less than 10% of Twitter’s total sales. In Q1’22 and Q2’22, data licensing segment revenues totaled $94.4 million and $100.1 million, representing a -5% and 7% increase year-over-year, respectively. We believe that close to 50% of -$43 million Q1’22 weakness, -$21 million, can be attributed to the remaining 10% of MoPub disposition-related impacts (again, 10% of mid-point impact, or $225 million).

3. Revenue % per mDAU:

One of the bullish theses we had for Twitter was that even if mDAU growth continues to plateau, the company will still be able to grow its topline more meaningfully than investors had anticipated as long as the company continues to extract more revenue per mDAU through the shift towards performance ads and adoption of various other monetization tools.

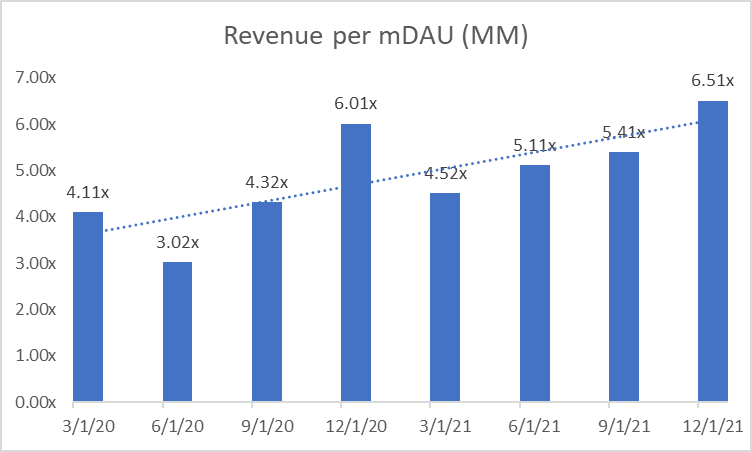

Since Covid, Twitter has continued to deliver on increasing monetization in revenue per mDAU. Advertising revenue percentage to mDAU (in millions) improved from: 4.11x to 3.02x to 4.32x to 6.01x to 4.52x to 5.11x to 5.41x to 6.51x for Q1 20’, Q2 20’, Q3 20’, Q4 20’, Q1 21’, Q2 21’, Q3 21’, Q4 21’, respectively. It is clear that while there are seasonality impacts, Twitter is able to extract meaningfully improved revenues for each one million mDAUs – for instance, Q4’21’s 6.51x represents an 8% improvement on revenue compared to Q4’20’s 6.01x.

Twitter Revenue per mDAU (MM) (Twitter Financial Statements)

However, in the most recent quarter, we observed a sustained downturn in revenue % per mDAU – Q2’22’s 4.52x represented an approximate -12% decline compared to same quarter in the prior year. This accordingly reinforces our discussion in the earlier section that companies are reducing advertising budgets due to various macroeconomic challenges.

Cost Increases

There are several analyses on Seeking Alpha that have raised concerns over Twitter’s deteriorating fundamental performance. Specifically, there has been a heightened focus on the increase in several cost items (e.g. R&D, G&A, etc.) for Twitter during Q2’22, while its top-line plateaued.

For example, while Twitter revenue contracted by -2.03% in Q2’22, its R&D costs increased by 22.3%, from -$372 million Q1’22 to -$454.9 million Q2’22.

But instead of fundamental deterioration, we attribute Twitter operating cost increases to the two strategic reasons below:

1) Poorly timed expansion. The company made plans in Q4’21 to increase headcount by 20% in order to improve performance ads capacity, with the ultimate goal to increase revenue per mDAU. However, the 2022 global economic slowdown has caught Twitter, alongside its peers, by surprise. In other words, non-operational headwinds have contributed additional pressure on the company’s near-term margin expansion trajectory.

We expect total cost and expenses to grow in the mid-20% range in 2022 versus 2021, excluding 2021’s onetime items with the number of buys that we see the opportunity to drive faster growth in revenue or mDAU. Expenses in 2022 are expected to ramp in absolute dollars over the course of the year as we invest with headcount growth of approximately 20% and a focus on R&D. We’re pleased with the decisions we’ve made to reallocate resources and to make trade-off decisions to hold expense growth to these levels.

2) Lag in revenue following the reallocation of resources of MoPub. Instead of selling the company’s talent along with MoPub, Twitter has decided to keep the cohort of employees and allocate them to other areas of business within the company. It was expected that sales would lag behind costs in the upcoming immediate quarters.

And just to remind folks what we’ve talked about here in the past, we did this to reallocate our resources to higher priority work where we think there’s a better payoff over time, ads on Twitter. And in doing that, we’ve already reallocated the people, but the revenue lags the work that the people do. And so, we don’t expect to make up all of that $200 million to $250 million this year. But we do expect to make up the effective run rate of MoPub plus MoPub Acquire in 2023, which is why there are no changes to those long-term goals that we’ve laid out.

Our point is that while Twitter underperformed operating margin expectations for Q2’22, it was not due to internal fundamental deterioration as many investors have feared. Instead, the near-term impact to Twitter’s bottom-line underperformance can be viewed in two folds: 1) non-operational challenges due to broad-based macro headwinds and uncertainties over coming months, and 2) pre-planned increase in spending, which was already guided in previous quarters, to support Twitter’s shift in corporate strategy towards driving revenue growth through new monetization features discussed.

Moving forward, we expect Twitter to temporarily underperform peers in margins due to ongoing macro headwinds, as well as strategically frontloaded investments into growth and continued revenue lag from resources reallocation.

It is possible for the company to follow other tech companies’ footsteps in pausing hiring or reducing headcount as well to reduce exposure to macro-related pressure on its margins once the potential Musk acquisition is settled. However, we expect the company to maintain its talent profile at status quo in the meantime to prevent interference from the ongoing dispute against Musk’s potential pull-out from the deal.

Valuation Analysis

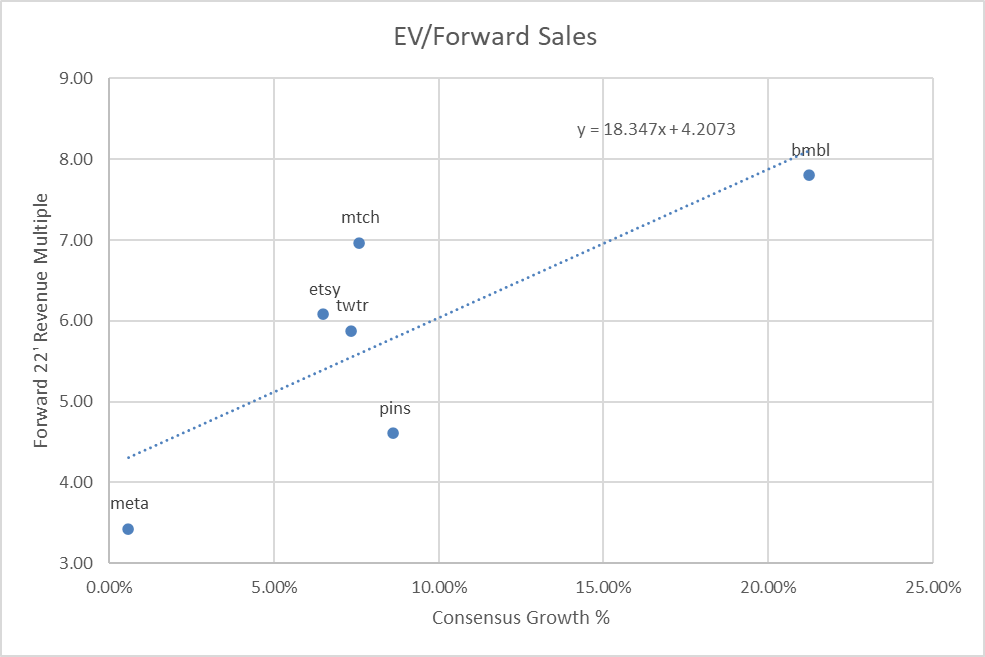

Market consensus expects Twitter to deliver revenue of $5.5 billion for FY ’22, or growth rate 7.3%. Market expectations continue to significantly underrun the mid-20% growth range guided by management. At its $5.45 billion enterprise value, it implies Twitter is trading at 5.9x forward EV/Sales multiple.

By extracting and plotting several social media platform peers’ consensus growth estimates and their respective FY ’22 revenue multiples on scatterplot, we find that these social media companies demonstrate a strong linear relationship in their consensus growth expectation and forward trading multiples.

In contrast from our previous findings that Twitter is trading below each percentage of revenue growth it was poised to deliver, the company is now trading above its fair market value because of the merger arbitrage opportunity between Twitter’s current market value vs. Musk’s proposed acquisition price. In our view, the company should trade closer to 5.5x ’22 sales, which translates to $30bn enterprise value, or -6% less compared to Friday’s close.

At its current market price, we no longer think Twitter offers a good risk/reward as an investment opportunity. The company remains on track for its turnaround, and upon deeper dive, its fundamental is better than it seems on the surface. But we acknowledge current macro headwinds (e.g., reduced budgets for ads) and the ongoing acquisition process have clouded the outlook of the company.

Twitter Peer Comp (Author)

Risks

While we think Twitter no longer offers an attractive risk/reward opportunity at $40, we have identified several risks beyond the current pending Musk potential acquisitions for investors who are holding Twitter as a long-term investment.

- The company may cease to remain relevant in the face of competition from short-form medias. Short-form media has emerged as the fastest social media trend through platforms such as TikTok and Reels (META). There Is a chance that short-form media platforms will succeed in outcompeting Twitter in user acquisition and product engagement, which will hurt Twitter’s future ability in growing and monetizing its mDAU as intended.

- The company profitability could be severely impacted by macro headwinds should global economic activities continue to slow. As mentioned earlier, Twitter generates more than 90% of consolidated revenue from its advertising segment. If global economic activities continue to slow, we expect Twitter’s advertising revenue to decline significantly.

Conclusion

While Twitter’s top- and bottom-line declines observed in Q2’22 were difficult for investors to digest, a deeper dive would reveal that the company is continuing business as usual. From a top-line perspective, declines normalized for its recent MoPub disposition are consistent with seasonality trends observed in previous years, underscoring Twitter’s positive progress still in maintaining resilient revenue per mDAU expansion in the face of increasing macro uncertainties. Meanwhile, from a bottom-line perspective, margin compression normalized for macro headwinds remain consistent with pre-planned increases to operating expenses to support Twitter’s shift in corporate strategy. In other words, there has not been any material downside deterioration to the company’s fundamentals outside of what was strategically planned and what is outside of the company’s control (i.e. non-operational external challenges).

However, we acknowledge that the risk/reward profile for Twitter as an investment at current levels is no longer as attractive as when we initiated coverage on the stock earlier in the year due to changes to the broader market climate in recent months. The evolving dispute with Musk on his pending acquisition of the company has also added uncertainty to the company’s forward outlook. Looking ahead, Twitter’s ability to execute its shift in corporate strategy towards expanding revenue per mDAU will be critical to restoring market confidence in the stock’s long-term potential.

Be the first to comment