jaanalisette

The Information Technology sector has climbed to its best relative level to the S&P 500 since late August. Firms from a variety of industries in the sector have announced plans to cut headcounts, and those headlines have often been met with buying from investors. We have another example today. Let’s dig into Twilio ahead of its Q4 earnings report.

Tech’s Monster 2023 Bounceback

Stockcharts.com

According to Bank of America Global Research, Twilio (NYSE:TWLO) is a customer engagement platform that allows developers to incorporate communication and data capabilities, including voice, messaging, video, and authentication into software applications, via Application Programming Interfaces (APIs). Twilio sells its products primarily by focusing on and servicing software developers.

The San Francisco-based $11.1 billion market cap IT Services industry company within the Information Technology sector does not have positive trailing 12-month GAAP earnings and does not pay a dividend, according to The Wall Street Journal.

Just today, the company announced a 17% reduction in its workforce. Shares naturally rose following that cost-cutting move, as has been the case with so many tech stocks this year. The restructuring effort comes as macro conditions deteriorate for the firm. BofA sees the move as accretive to earnings, but they remain somewhat bearish on the stock, though they did raise their target to $65.

On valuation, analysts at BofA see operating earnings having fallen a staggering 84% in 2022, but then slowly recovering through 2024. The Bloomberg consensus forecast is significantly more sanguine as it shows operating EPS turning into the black this year. With a high EV/EBITDA ratio, I like to look at the historical price-to-sales ratio to get a sense of relative pricing.

What I find attractive here is that TWLO’s forward P/S is now under 3 versus a five-year historical trailing ratio averaging more than 16. Three times revenues is a small price to pay for this decent growing stock even with a poor macro backdrop. Moreover, Twilio is expected to be free cash flow positive for FY 2023.

Twilio: Earnings, Valuation, Free Cash Flow Forecasts

BofA Global Research

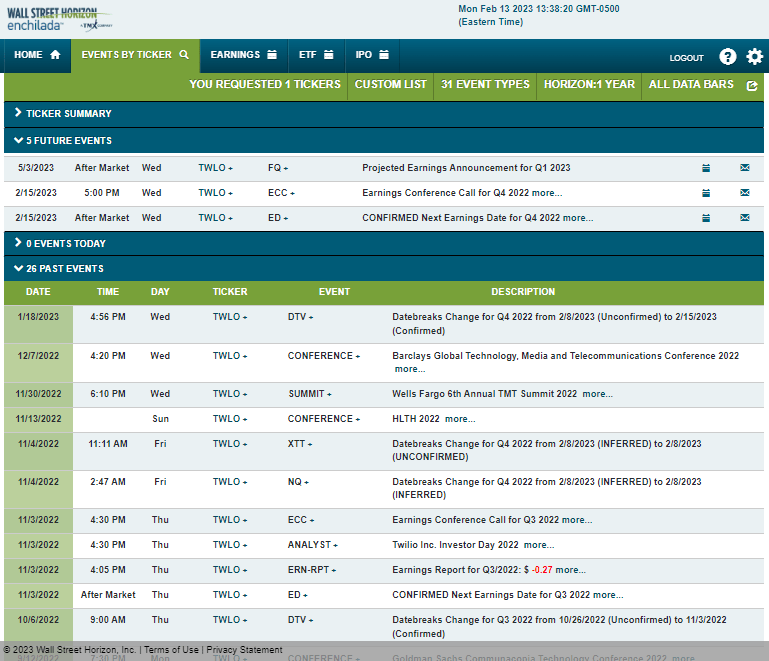

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q4 2022 earnings date of Wednesday, Feb. 15, after market close with a conference call immediately after numbers hit the tape. You can listen live here. It’s the only volatility catalyst I spot on the calendar.

Corporate Event Risk Calendar

Wall Street Horizon

The Options Angle

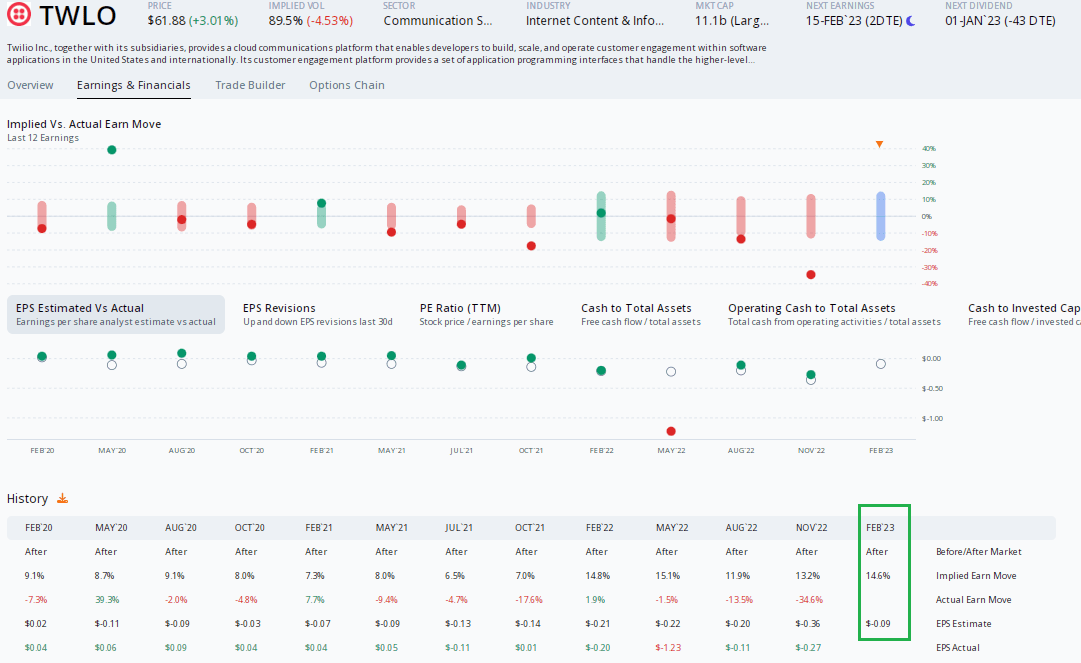

Digging into the upcoming earnings report, data from Option Research & Technology Services (ORATS) show a consensus EPS figure of a loss of $0.09. That would be a material improvement from $0.20 of per-share losses reported in the same quarter last year. What’s bullish for TWLO longs here is that the stock has topped analyst earnings forecasts in 11 of the 12 quarters. Unfortunately, though, the stock has traded lower post-earnings in eight of the last 10 earnings reports. So, overall, it’s not a good look.

In terms of the expected stock price swing when analyzing the at-the-money straddle expiring soonest after the upcoming earnings report, ORATS data show a high 14.5% implied move. With a handful of big moves lately, a double-digit percentage change appears priced right to me, so only high-risk traders should play TWLO through options this week.

TWLO: Weak Earnings Reaction History

ORATS

The Technical Take

With a much-improved P/S ratio and free cash flow that should be positive this year, how does the chart look? Notice in the graph below that shares put in a major capitulation-like low back in November after reporting poor earnings for Q3. The stock then bounced and consolidated before marching higher this year. I see resistance in the mid to high $60s – take a look at how that area has been significant since late 2018. It’s also the March 2020 COVID low.

What’s more, the falling 200-day moving average will soon come into play there. If we can get a close above the 200-day and $70 or so, then a move up to the low $80s could be quickly in play. Longer-term resistance is seen in the low $150s. $54 is support.

TWLO: Capitulation Bottom, Pausing at Resistance But Strong RSI Momentum

Stockcharts.com

The Bottom Line

TWLO may have completed its massive downtrend if that capitulation signature is the right conjecture, but there’s still work to do by the bulls. Trading at just 3x forward sales, it’s a much more reasonable valuation. Today’s resizing move is a sign of management prudence, too. I’m a soft buy on the stock going into the Q4 report, but a poor earnings reaction history is a near-term risk.

Be the first to comment