Ceri Breeze/iStock Editorial via Getty Images

Investment Thesis: I take a bullish view on TUI AG given strong revenue growth and potential for an earnings rebound as operational issues across European airports are expected to lessen in Summer 2023.

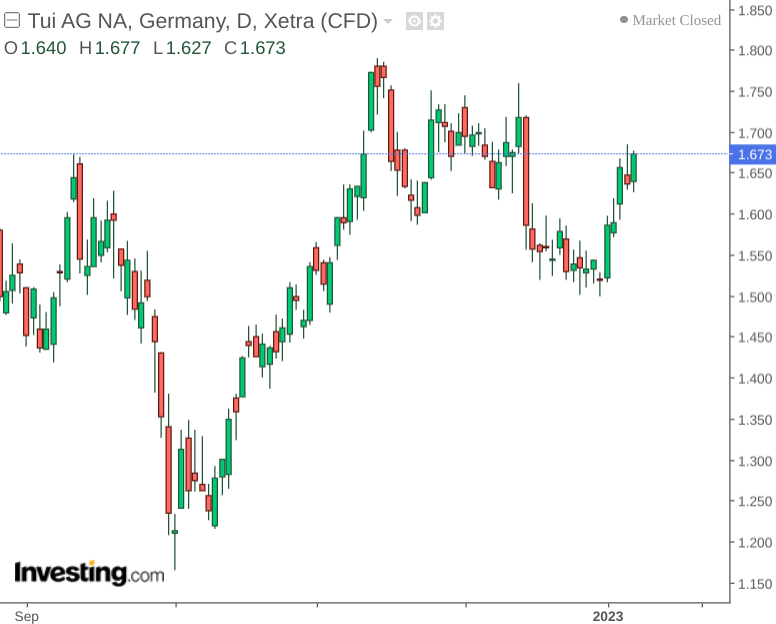

In a previous article back in September, I made the argument that TUI AG (OTCPK:TUIFF) may not see significant upside until mid-2023 as a result of travel demand in the winter months remaining too uncertain.

However, my outlook may have been overly pessimistic – as travel revenues have seen a strong increase even in the face of rising winter prices – while the stock has seen growth over the past few months:

investing.com

The purpose of this article is to investigate whether the upside we have been seeing in the stock can continue.

Performance

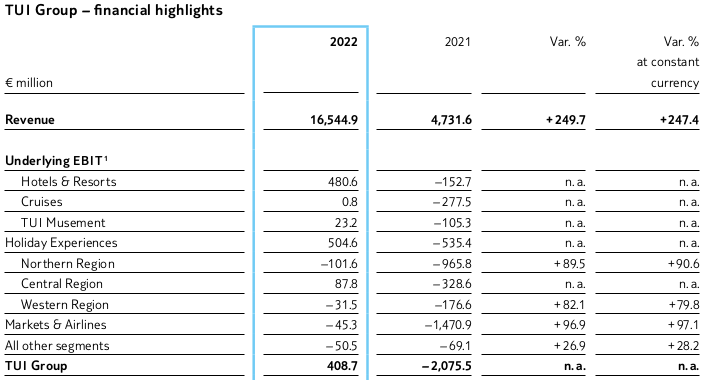

When looking at EBIT performance for TUI AG, we can see that while Holiday Experiences saw a strong rebound from 2021. With that being said, we can see that while the loss in EBIT has been greatly reduced – the Northern Region still saw a loss of over $100 million, with a loss of €31.5 million for the Western Region.

TUI AG Annual Report 2022

To clarify, the Northern Region refers to tour operator activities and airlines across the UK, Ireland, and the Nordics. The Western region comprises of Belgium, Netherlands and France, while the Central Region comprises of Germany, Austria, Switzerland, and Poland. As we can see – it is the Central Region that has returned to positive EBIT.

Across the Northern Region in particular, the company cites travel disruptions over the summer period – such as the cancellation of flights from Manchester over June – as being a contributor to the loss experienced across this segment.

However, it is notable that aside from a sharp increase in revenue of nearly 250% from that of 2021 – the Northern Region showed the largest percentage growth in revenue at nearly 700%:

TUI AG Annual Report 2022

Given that we have seen strong revenue growth – I take the view that the upcoming summer season could plausibly bring EBIT back into positive territory over the summer months.

While airports across the UK are still facing issues due to strike action and major hubs such as Amsterdam’s Schiphol Airport continue to impose passenger caps – TUI AG has taken action to mitigate this by redeploying flights from Amsterdam to Brussels last October while current strike action in the UK does not appear to have caused as much disruption as previously anticipated.

Moreover, with winter prices up by 23% for the current winter season as compared to the same period in 2018-19, I take the view that demand will continue to remain vibrant in spite of inflationary pressures.

Financials

When looking at the company’s balance sheet metrics and comparing that of September 2019 to September 2022 – we can see that the company’s quick ratio has fallen over this period – indicating that TUI AG has less ability to meet its current liabilities using existing liquid assets.

| Sep 2019 | Sep 2022 | |

| Current assets | 4313.5 | 3903.8 |

| Inventories | 114.7 | 56.1 |

| Current liabilities | 6857.6 | 8168.6 |

| Quick ratio | 0.61 | 0.47 |

Source: Figures sourced from TUI AG 2022 Annual Report. Figures provided in € millions except the quick ratio. Quick ratio calculated by author as current assets less inventories all over current liabilities.

Additionally, we can see that the proportion of non-current liabilities (or long-term debt) relative to total assets has also increased.

| Sep 2019 | Sep 2022 | |

| Non-current liabilities | 2940 | 4543.8 |

| Total assets | 16270.9 | 15255.5 |

| Non-current liabilities to total assets ratio | 18.07% | 29.78% |

Source: Figures sourced from TUI AG 2022 Annual Report. Figures provided in € millions except the non-current liabilities to total assets ratio. Non-current liabilities to total assets ratio calculated by author.

Looking Forward

Given recent results, the fact that revenues have continued to see strong growth in the face of rising prices and travel disruptions is quite encouraging. Holidaymakers are keen to travel, and it is clear that demand continues to remain vibrant in spite of macroeconomic pressures.

I am cautiously optimistic that operational disruptions across airports in Europe will be less this summer – as staffing levels across the industry start to normalise and TUI redeploys its flights to less congested bases as necessary.

In my view, the main risk at this time is that travel demand for Summer 2023 is lower than anticipated or continued operational difficulties mean lower earnings growth. However, I take a bullish view on the stock in spite of these risks given recent performance.

Conclusion

To conclude, I take the view that TUI AG is in a good position to capitalise on strong travel demand in spite of ongoing macroeconomic pressures. For this reason, I take a bullish view on the stock.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment