PonyWang

Article Thesis

Taiwan Semiconductor Manufacturing Company Limited (NYSE:TSM) will announce its earnings results in a couple of days from now. In this report, we will look at what investors can expect from the company and at TSM stock’s outlook in the foreseeable future.

Investors Fear A Semiconductor Downturn

During the initial phase of the pandemic, semiconductors were rare. There were several contributing factors to that. First, there were some supply chain disruptions due to lockdowns and other COVID measures. Then, consumers increased their purchases of all kinds of tech products and gadgets – flush with cash thanks to stimulus payments, consumers bought more phones, personal computers, smart home equipment, and so on.

The combination of these factors resulted in an imbalanced supply-demand picture for semiconductors, which is why prices went up, which naturally was great for semiconductor producers and sellers. Some additional factors, such as rising cryptocurrency prices that made mining cryptocurrencies more profitable, further boosted the short-term demand picture for at least some kinds of chips, such as GPUs.

But with inflation rising and fiscal stimulus payments declining, consumers have become less inclined to spend on electronics and tech products. Their disposable income has declined, on average, as they need to spend more on the necessities such as shelter, food, and energy. At the same time, rising interest rates have made it more likely that we will experience an economic downturn, which is why business and enterprise customers have become more reluctant to spend heavily on new tech investments, which has also hurt semiconductor demand to some degree.

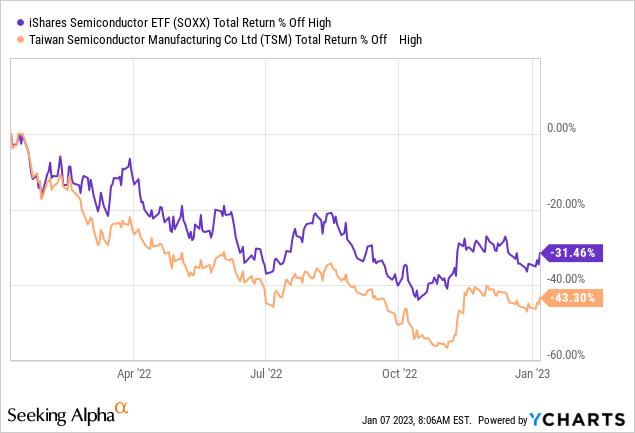

Overall, that is why investors have soured on semiconductor stocks, as showcased by the following chart:

Over the last year, the Semiconductor ETF (SOXX) has declined by around one-third, while Taiwan Semiconductor Manufacturing Co has declined by an even wider 43% over the same time frame. Around two months ago, prices for both the ETF and TSM were even lower, but they have recovered some of their losses since then.

TSM’s wider-than-average share price decline started early on in 2022. I do believe that this is tied to geopolitical risks. When the war in Ukraine started, investors became more worried about a potential escalation of the Taiwan conflict, and TSM was sold based on that, which is why it has underperformed the wider semiconductor industry since then.

While the worries about the world economy and geopolitical risks in Taiwan are not fictitious, TSM’s underlying performance has been very strong in the recent past.

TSM: Performing Very Well

So far this year, Taiwan Semiconductor Manufacturing has shown highly compelling business growth:

Seeking Alpha

Revenue was up by more than 30% during each of the first three quarters of the current year, beating estimates every time. Also, importantly, TSM was more profitable than the analyst community had expected, beating earnings per share estimates by more than 5% on average in this time frame.

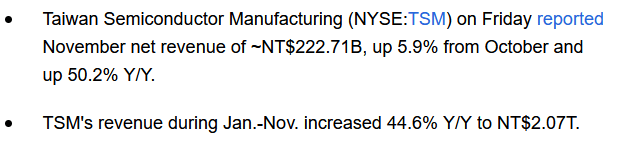

Since Taiwan Semiconductor Manufacturing Company announces its monthly sales figures, we have solid clues about what its Q4 sales performance looked like. Seeking Alpha reported the following sales figures for the months of October and November:

Seeking Alpha Seeking Alpha

Year-over-year growth was very strong in the company’s local currency, New Taiwan Dollar. Revenue growth averaged 53% over those two months. Since revenue growth was higher in November relative to October, one might assume that revenue growth during December was even better, but there is no guarantee for that, of course. I believe the average of the two prior months is a solid base case for the December sales performance, which would get us to a ~53% growth rate in NT$. The NT$ has gotten weaker versus the US Dollar over the last year, however, as have most other currencies around the world. The NT$ has lost around 11% versus the USD over the last year, thus growth of ~53% in Taiwan’s local currency would translate to a growth rate of around 36% (1.53 * 0.89) in US Dollars, all else equal.

Since we know Taiwan Semiconductor Manufacturing Company’s sales during the previous year’s fourth quarter of $15.9 billion, we can guesstimate that sales could have come in around $21.6 billion for the fourth quarter of 2022. The current analyst consensus estimate is slightly less than that, at $20.8 billion – it looks like analysts have baked in a considerable decline in the company’s sales growth rate for December. It should be noted that analysts have a history of underestimating TSM’s revenue performance, thus it would not be too surprising to see TSM’s sales come in ahead of the expected $20.8 billion. When we average the number I got to using the October and November growth rate and the analyst consensus estimate, we get to $21.2 billion in revenue for the fourth quarter. That would be ahead of Wall Street estimates by $400 million, which is pretty close to the average revenue beat of $370 million that TSM has delivered over the previous three quarters.

I thus believe that there is a good chance that TSM’s revenue will come in slightly ahead of $21 billion for the fourth quarter, which would be another revenue beat and which would make for a highly compelling revenue growth rate of more than 30%. That revenue growth would be achieved despite the ongoing economic downturn and despite the market’s worries about a semiconductor glut. But since TSM benefits from price increases that it negotiated with the companies it manufactures chips for, and since its market position as the preeminent foundry in the world has gotten only stronger, the company looks like it is weathering the current macro issues very well.

Looking at profits, analysts are currently expecting that TSM will report earnings per share of $1.76 for the fourth quarter. That would be down slightly from $1.79 during the third quarter. Since it is expected that TSM will record solid revenue growth on a sequential basis, I do believe that it is unlikely that profits went down. As a company with high fixed costs, TSM tends to benefit from revenue growth as that allows for operating leverage, which increases its profitability. A combination of rising revenues and declining profits thus does not look like the most likely scenario to me, but it is still possible, of course.

When we consider that analysts also have a history of underestimating TSM’s profits, an earnings beat versus the forecasted small sequential EPS decline seems quite possible to me. I believe that there is a good chance that earnings per share will come in at $1.80 or higher for the fourth quarter. Ultimately, a couple of cents do not matter overly much, however – long-term oriented investors should not sweat too much even if TSM were to miss estimates by a couple of cents.

TSM: Inexpensive Due To China Fears

No matter whether TSM beats estimates again, it is pretty clear that the company had a great fiscal 2022, delivering massive growth despite the semiconductor slowdown that has gotten a lot of attention.

In the long run, the demand for chips will grow considerably, I believe. Megatrends such as digitalization, the internet of things, autonomous driving, AR and VR, cloud computing, and so on will drive demand for chips for many years. TSM is one of the best-positioned companies to benefit from broad market growth – thanks to its leading position in the foundry space, it benefits from market growth, no matter which fabless semiconductor company shows the best growth rate.

And yet, TSM trades at only 12x net profits, based on forecasted earnings per share of $6.53 for fiscal 2022. That’s a pretty low earnings multiple for a company that is growing at a 30% clip, which can be explained by two things. First, the market anticipates that growth will slow down in 2023, which seems quite possible, especially when we get a harsher recession. On top of that, the market also worries about TSM’s exposure to a potential escalation of the Taiwan conflict. While it is pretty clear that TSM would be highly exposed to a potential war on Taiwan, I do believe (and hope) that this is unlikely. And even if a war were to break out, many non-Taiwanese companies would be hit extremely hard as well. Global semiconductor supply chains would be hit massively, and Western companies selling a large amount of goods in China, such as Apple (AAPL) or Tesla (TSLA), would suffer as well. So while investors should not neglect geopolitical risks when investing in TSM, I do not believe that investors should be paralyzed by these fears.

Takeaway

TSM is a great company with a strong market position. In the long run, the company should benefit from market growth, and its investments outside of Taiwan, such as in Arizona, could make it more attractive for those worrying about the Taiwan conflict. I do believe that another revenue and earnings beat is likely when TSM reports its Q4 results on January 12. While risks shouldn’t be ignored, I believe the potential rewards of investing in this giant at just 12x net profits outweigh the risks, which is why I am bullish on TSM.

Be the first to comment