BING-JHEN HONG

TSMC (NYSE:TSM) increased its Foundry Revenues in Q3 2022 by 11.1% compared to -0.1% for Samsung Electronics (OTCPK:SSNLF) and Intel (INTC) by 40.2%.

TSMC’s share of the foundry sector increased from 53.4% to 56.1%, while Samsung’s share decreased from 16.4% to 15.5%. Intel’s share increased from 0.36% to 0.46%, according to The Information Network’s report entitled “Hot ICs: A Market Analysis of Artificial Intelligence (“AI”), 5G, Automotive, and Memory Chips.”

While TSMC is #1 and Samsung #2 in the foundry market, Intel’s acquisition of Tower in 2023 will move INTC to #7 just behind Huahong.

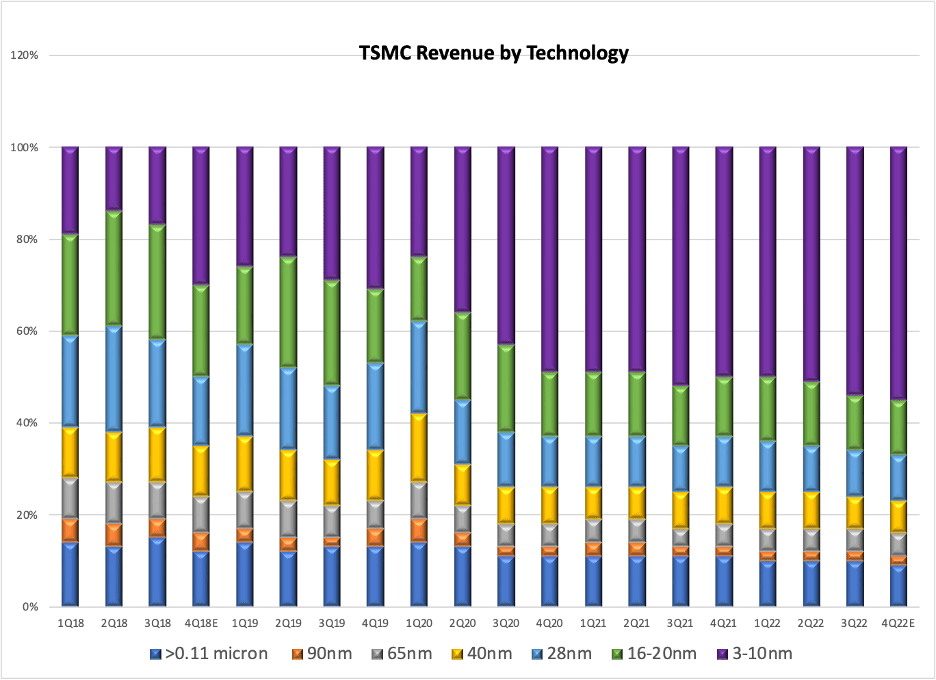

Chart 1 shows TSMC’s revenue by technology node between Q1 2019 and Q4 2022. Revenues from the 3-10nm nodes have been increasing, and in Q3 2022 represented 54% of total revenues (purple bar).

Chart 1

TSMC

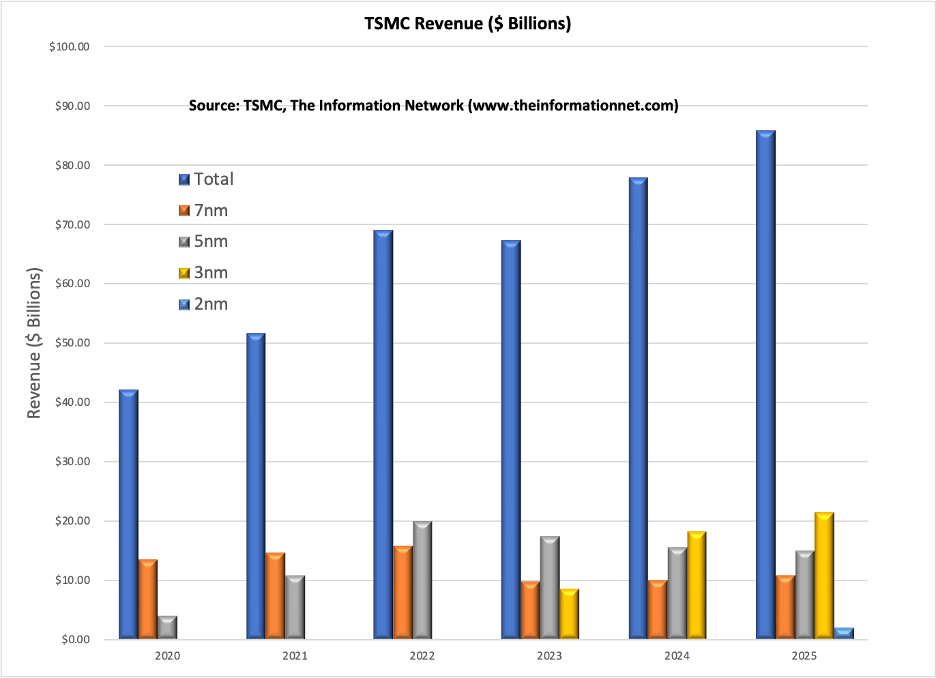

Chart 2 breaks out the 3-10nm node range into revenues by year for TSMC. Chips at the 7nm began generating revenues in 2018 but will peak in 2022 as the 5nm node takes over. Chips at the 3nm node will generate revenues in 2023 while 2-nm node chips will enter the market in 2025.

Chart 2

The Information Network

As it relates to Chart 2 above:

- I forecast that 7nm revenue will drop 38% YoY in 2023 following an increase of 8% in 2022, primarily because of the slowdown and inventory correction in smartphones and PCs. N7 revenues in 2024 will increase just 2%, largely because of a slowdown in the semiconductor market brought about by macro factors and oversupply from excessive capex spend in 2020-2021.

- I forecast 5nm revenue growth to drop -13% in 2023 YoY following an 83% increase in 2022, due to reduction of inventory from major customers at this node including Apple (AAPL) and Hewlett Packard (HPE). Revenues are expected to drop in 2024 due to process node migration to 3nm, keeping in mind that the 5nm node has been in production since 2020.

- I forecast 3nm revenue to start production in 2023 and represent 24% of the sub 7nm segment, as 7nm drops to 28% and 5nm to 48% of the $36 billion segment. Key customers for the 3nm node are Apple’s A17 (iPhone) and M3 (“Mac”) processors. Note that TSMC’s first-generation N3 node will be used for primarily by Apple. TSMC’s second-generation N3E will feature an improved process window, resulting in faster time to yield, increased yields, higher performance, and lower power. The N3E node should begin production in 2H 2023.

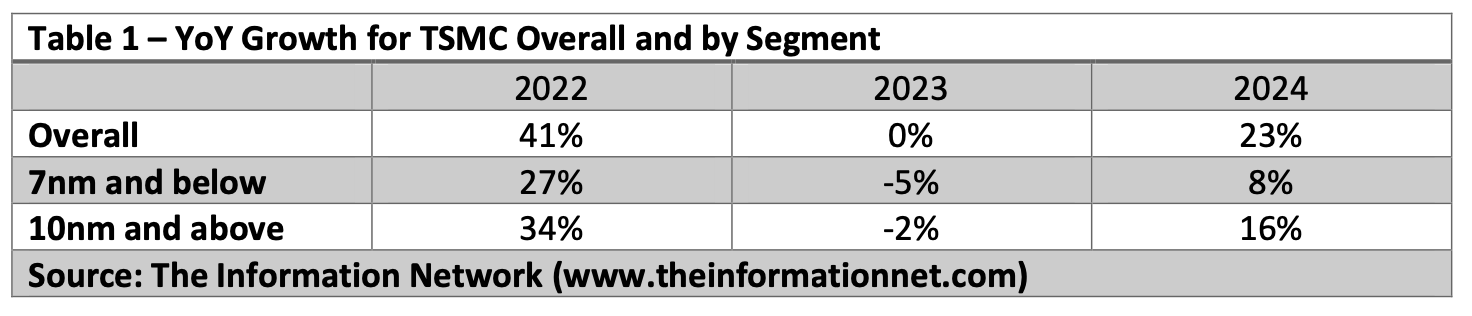

Table 1 summarizes my forecast for TSMC revenue growth from 2022-2024.

The Information Network

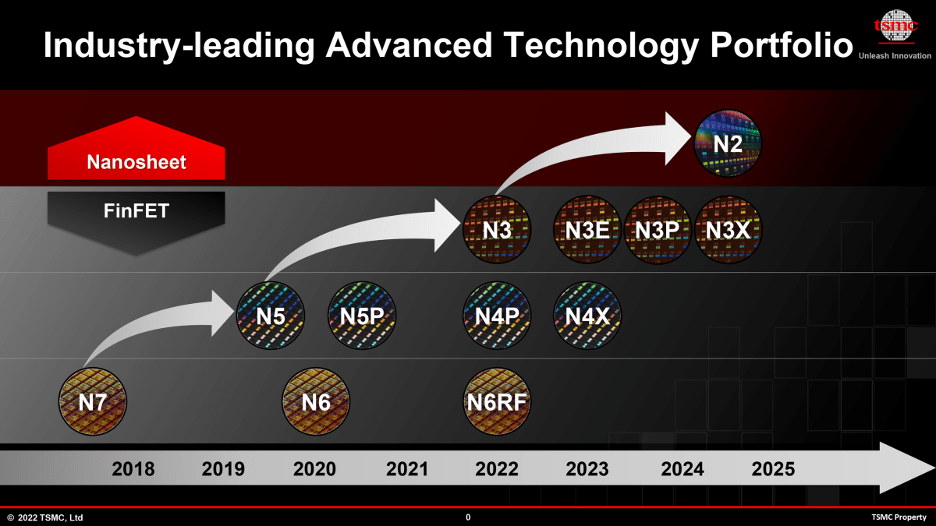

TSMC plans to introduce five 3nm class process technologies in the next two or three years, as illustrated in Chart 3.

Chart 3

TSMC

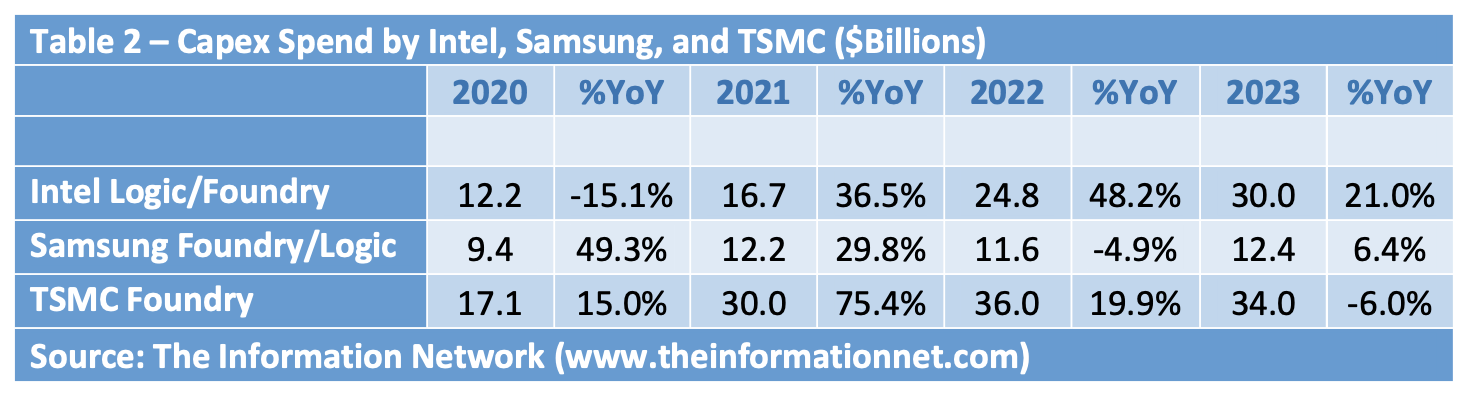

Capex Spend

Capex spend is a combination of building and fab equipment in roughly a 50:50 ratio. Shown in Table 2 are capex spend plans for TSMC, Intel, and Samsung between 2020 and 2023. Samsung’s capex is for foundry only and does not include DRAM or NAND capex.

The Information Network

In 2021, TSMC was the biggest spender, with capex at $17.1 billion, an increase of 75.4% from 2020, growing 19.9% in 2022. Samsung capex increased 49.3% in 2020 to $9.4 billion. In 2022, Intel is forecast to increase capex 48.2%.

Nevertheless, between 2020 and 2023, TSMC’s capex spend is higher each year than competitors Intel and Samsung, even after reducing capex YoY n 2023. This increased spend will result in increased fab capacity and increased chip output.

Node Transitions

Competition among the three companies making <7nm chips will be dependent on the technological features of its products coming from chip design and node transition roadmaps. Table 3 below shows the technology roadmap for TSMC, Samsung, and Intel between 2020 and 2025.

The Information Network

TSMC

Due to end market weakness in smartphone and PCs and with its customer’s products scheduled delays starting 4Q this year, the N7, N6 capacity utilization, will not be as high as it has been in the past three years.

According to TSMC’s CEO C. C. Wei

“Our N3 is on track for volume production later this quarter with good year. We expect a smooth ramp in 2023, driven by both HPC and smartphone applications. Our customers’ demand for N3 exceeds our ability to supply partially due to the ongoing tool delivery issues, and we expect N3 to be fully utilized in 2023.

N3E will further extend our N3 family with the enhanced performance, power and yield, and offer complete platform support for both smartphone and HPC applications. N3E development is progressing ahead of plan, and volume production is now scheduled for second half 2023.”

Samsung

Samsung Foundry’s 3GAE (3nm-class, gate-all-around early) uses gate-all-around transistors, whereas TSMC’s N3 (3nm-class) still relies on FinFET transistors.

The company’s second-generation 3 nm gate-all-around (3GAP) technology is now set to arrive sometime in 2024. Meanwhile, Samsung Foundry intends to be ready with its 2 nm node in 2025, and with its 1.4 nm-branded fabrication process in 2027.

Intel

Intel has a goal of achieving five nodes in four years. Meteor Lake is built on Intel’s 7nm chip production node, otherwise known as Intel 4. Granite Rapids will be upgraded from Intel 4 to the Intel 3 process in H2 2023. Arrow Lake will follow in H1 2024 on the Intel 20A. Chips on the Intel 18A are scheduled for H2 2024.

Intel 4 and 3 are its first nodes deploying EUV and will represent a major step forward in terms of transistor performance per watt and density. The Intel 20A, due for manufacturing introduction in the first half of 2024, remains the big technological jump. It simultaneously introduces a new transistor architecture-RibbonFET (more generally called gate-all-around or nanosheet transistors)-and PowerVia backside power delivery.

Investor Takeaway

According to my analysis, strong growth for TSMC going forward is also dependent on fab construction. Importantly, the move to the smallest technology nodes at foundries wouldn’t be possible without ASML’s (ASML) EUV technology (extreme ultraviolet). I estimate that between 2015 and 2022, TSMC purchased 101 EUV lithography systems from ASML, while Samsung purchased 31 and Intel 26 systems.

Below are fab plans for TSMC, Samsung, and Intel.

TSMC

- Fab 15 phases 5, 6, and 7 – Taiwan (7nm EUV)

- Fab 18 phase 1, 2, and 3 – Taiwan (5nm with EUV)

- Fab 18 phases 4, 5, and 6 – Taiwan (3nm EUV)

- Fab 20 phases 1, 2, 3, and 4 – Taiwan (2nm planning)

- Fab 21 – Arizona (5nm EUV)

Samsung

- V1 – South Korea (7nm to 3nm future)

- Taylor, Texas (under construction)

- P3 – South Korea (4nm EUV)

Intel

Intel has three development fabs and nine production fabs with EUV capabilities:

- D1X phases 1, 2, and 3 – Oregon (development)

- Fab 42 – Arizona (EUV capable)

- Fab 52 – Arizona (under construction)

- Fab 62 – Arizona (under construction)

- Fab 34 – Ireland (recently installed)

- Fab 38 – Israel (under construction)

- Silicon Heartland 1 and 2 – Ohio (planning)

- Silicon Junction 1 and 2 – Germany (planning)

TSMC has a clear lead based on several metrics, but Samsung is six months ahead in node migration. Samsung will slowly close the technology gap with its transition to advanced logic architectures, including GAA and MBCFET at 3nm. The 50% lower power consumption and 35% overall higher performance of GAA will be a catalyst for the migration of customers to Samsung provided capacity is available. But the capacity gap will remain.

However, Samsung has been losing customers to TSMC recently. Nvidia (NVDA) chose the Samsung 8nm node for the RTX 30 range, but Nvidia has dropped them because of low yields in favor of TSMC’s 4nm process for its high-end RTX 40 series

Also, Qualcomm (QCOM) Snapdragon’s recent high-end APs have been problematic in the past few years from overheating, which were built on Samsung 5nm and 4nm processes. Qualcomm switched from Samsung to TSMC for manufacturing, claiming a 30% efficiency gain and 10% CPU clock speed improvements across the board as a result. The refreshed chipset, built on TSMC’s 4nm process node, also gains a 10% GPU clock speed boost and an apparent 20% boost to performance-per-watt.

TSMC is my #1 semiconductor stock for 2023. Macro headwinds will impact the company, but less than other foundries and significantly less than memory companies. TSMC is still a solid long-term investment as it dominates the foundry model.

TSMC will benefit from the U.S. Chips act, although I estimate operating margins will be lower for chips made in Arizona than those made in Taiwan.

On the opposite note, U.S. sanctions on China have significantly impacted TSMC, which was the largest supplier of sanctioned Huawei. While the new norm is slower revenue growth, these sanctions are proving fruitless and only catalyzing the resolve of Chinese manufacturers to ramp to ‘Made in China 2025’ goals.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment