JHVEPhoto/iStock Editorial via Getty Images

“Merger”

I learned a long time ago to pay close attention to what bank CEOs tell investors during earnings calls and in annual reports.

Truist Financial Corporation (NYSE:TFC) has a key word: “MERGER.”

Since announcing the BB&T – SunTrust “transformational merger of equals” that “creates the premier financial institution” in the country on February 7, 2019, the word “merger” has been uttered 530 times during 15 subsequent earnings calls.

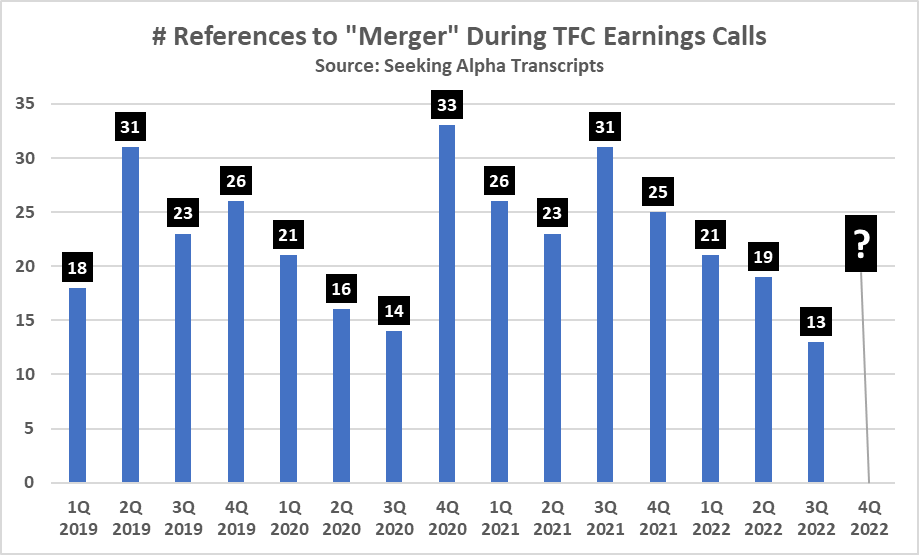

Check out the bar graph which reflects the number of times “merger” has been referenced since Q1 2019.

Several key numbers stand out:

- The good news: Since Q3 2021, there has been a steady decline in the number of “merger” references.

- Merger references fell during 2020 in the midst of COVID fears; likely, the COVID distraction slowed merger progress.

- 2021 witnessed 113 references to merger compared to 53 during the first three quarters of 2022.

You can bet that I will be counting “merger” references when Truist hosts its 4Q 2022 earnings call on January 19.

Merger References (Seeking Alpha Transcripts)

Stock Price Performance since Feb. 7, 2019

Since the merger was announced on February 7, 2019, Truist share price has declined -5.6%.

To put the price decline in context, Truist modestly trails the SPDR S&P Regional Banking ETF (KRE) which is up only 9.1% during the same time.

Obviously, the regional banking sector is out of favor, and therefore, Truist’s share price problem is linked to not only its large merger but also the sector.

The Challenge with (Relatively) Large Bank Mergers

A couple of years ago, the Risk Management Association, which is an industry group comprised of 2,000 North America banks, asked me to write an M&A Due Diligence Handbook in addition to an analysis of US bank mergers from 2015-2019.

The analysis of US bank mergers from 2015-2019 yielded several insights:

- Acquiring banks’ share prices as a group underperformed non-acquiring banks over 1, 2, and 3 years.

- However, not all acquiring banks underperformed peers. Those that proved most able to improve stock price were in almost all cases banks involved in mergers with banks just a fraction of the size of the acquiring bank. Often those mergers were in-market, but not in all cases.

- Underperforming banks tended to be acquiring banks engaged in a relatively large acquisition (as measured by assets). Said another way, the larger the asset size of the acquired bank as a percentage of the asset size of the acquirer, the lower the subsequent share price performance. This truth transcends small community banks to large regional banks.

- My White Paper for the RMA included a data-driven analysis of the factors most influencing underperformance. Readers of the analysis were surprised to learn that the chief issue was not the acquiring bank’s failure to meet expected expense cuts. In fact, in almost in every case, acquiring banks met expense cut targets. The key challenge, it turned out, was not expenses but revenue. Banks involved in big mergers frequently struggle to maintain revenue of not only the acquired bank, but also its own revenue stream.

Truist 3Q 2022 Earnings Call Merger Discussion

It is possible Truist has turned the corner. Here is evidence:

- Q3 earnings call included the lowest number of references (13) to “merger” since the BB&T-SunTrust merger was announced.

- The CEO indicated during the call that “Merger calls diminished again, and our remaining decommissioning activities are mostly complete and be finalized by year-end.”

- The CEO went on to say: “The final merger costs expected in the fourth quarter are primarily related to our decommissioning efforts, which, as I mentioned, will conclude by year-end. The completion of merger activities is a monumental move forward that will reflect a seamless client experience, simplify our narrative, enhance our earnings quality, improve capital and help us realize industry-leading returns.”

Since the October 18, 2022, earnings call, Truist shares have advanced 5.4% compared to a -6.3% decline in the regional bank ETF. The recent price momentum may indicate growing investor confidence.

What I Want to Know During 4Q Call

Seven Questions

- Is the merger definitively complete? Is the merger now in the rear-view mirror?

- Are there no more “one-time” costs?

- How is Revenue and Loan Volume holding up? FDIC data show Truist’s loan book up only 3% since Q4 2019 compared to an average increase of 22.5% for U.S. Bancorp (USB), Capital One Financial Corp (COF), PNC Financial Services Group, Inc. (PNC), and Citizens Financial Group, Inc. (CFG).

- Is Truist gaining back momentum in C&I lending lost since 2019? Truist’s C&I book up 8% since Q4 2019 compared to an average increase of 28% for USBank, Capital One, PNC, and Citizens.

- Credit Quality? Not too long ago, I heard rumors that Truist was cutting corners on some parts of its consumer lending book, so I want to see how credit holds up. Provision will be a key area of focus for me. That said, Card loans are down 22% since Q4 2019. Is the decline deliberate management of the bank’s risk profile or a function of lost market share? The Auto book is up 28% for the same period, which is second highest growth rate to only Capital One which is up 32%; conservative PNC is down -10%. Is the big growth in Auto an elevated risk in a weakening economy?

- Funding Costs (for bank subsidiary) are incredibly important. FDIC data showed Truist to have Q3 2022 funding cost of 37 bps which compares favorably to Capital One (126 bps), Citizens (40 bps), USBank (54 bps), PNC (43 bps). Clearly, funding costs are up in Q4, but by how much? Impact on net interest margin is a critical factor.

- Talent? Investors were told that a major motivation for the merger was related to a need to attract and retain talent, especially those skilled in next generation technology, data management, and risk. This same motivation justified the expensive move of the bank’s headquarters to Charlotte. Is Truist winning the war for talent?

- How about Customer Satisfaction? How is customer retention?

My Plan

I must be confident that Truist is on the path to generating sturdy and reliable returns exceeding its cost of capital which I estimate to be ~10%. There is no question that Truist has failed to earn back its cost of capital since the merger was announced.

My plan is to read the January 19 earnings numbers and transcript and report back on these pages. If I like what I hear, I will be a buyer of shares. If I do not, I will explain my concerns and conditions for investment.

If I owned TFC shares today, I would HOLD for now.

Caveat

The foregoing is my opinion which I share for the purpose of getting feedback and questions that challenge my ideas and assumptions.

Every investor needs to do his/her own due diligence before investing as well as determine their risk profile. I am risk-averse, preferring to invest in the nation’s best banks which reliably earn returns exceeding cost of capital.

Be the first to comment