Thomas Barwick

Investment Thesis: I take a bullish view on Tripadvisor given strong revenue growth and an attractive EV/EBITDA ratio.

In a previous article back in February 2021, I made the argument that while Tripadvisor (NASDAQ:TRIP) could have significant growth prospects ahead – the market was potentially too optimistic on the stock at the time – particularly that price was increasingly divorced from fundamentals.

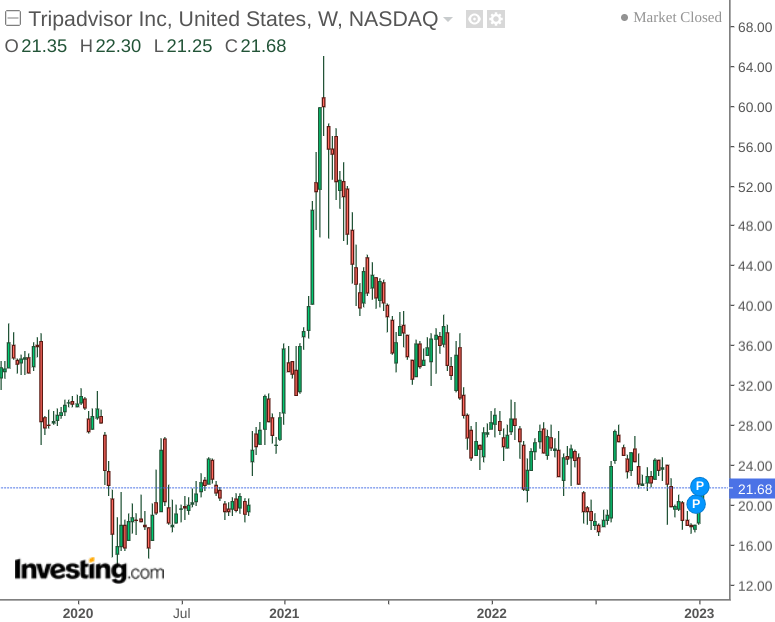

After seeing a significant post-COVID recovery, Tripadvisor subsequently saw sharp downside heading into 2022 and has failed to make significant gains since then:

investing.com

The purpose of this article is to assess whether Tripadvisor could conceivably see a rebound in upside from here.

Performance

When comparing revenue performance for Q3 2019 and Q3 2022 – with the former period being used as a baseline for pre-COVID performance – we can see that total revenue has now exceeded that seen in September 2019.

Q3 2019 Revenues

Tripadvisor: Q3 2019 Financial Results

Q3 2022 Revenues

Tripadvisor: Q3 2022 Financial Results

When looking at a comparison of the quick ratio for the aforementioned two periods, we can see that while the quick ratio has decreased slightly – the ratio still remains well above 1 – indicating that TripAdvisor can more than adequately service its current liabilities using its existing liquid assets. The quick ratio was calculated as cash and cash equivalents plus short-term marketable securities plus accounts receivable all over current liabilities.

| Sep 2019 | Sep 2022 | |

| Cash and cash equivalents | 838 | 1066 |

| Short-term marketable securities | 95 | 0 |

| Accounts receivable | 218 | 205 |

| Current liabilities | 468 | 573 |

| Quick ratio | 2.46 | 2.22 |

Source: Figures sourced from Tripadvisor Q3 2019 and Q3 2022 Financial Results. Figures provided in USD millions, except the quick ratio. Quick ratio calculated by author.

For December 2021, TripAdvisor had a long-term debt of $833 million. By September 2022, this had increased marginally to $836 million. While it is encouraging that TripAdvisor has not had to incur significantly greater long-term debt loads to fund its operations – it would be preferable to see a decrease in this metric. Indeed, I take the view that investors will look for evidence that TripAdvisor can in fact decrease its long-term debt given the growth in revenue and earnings that we have been seeing.

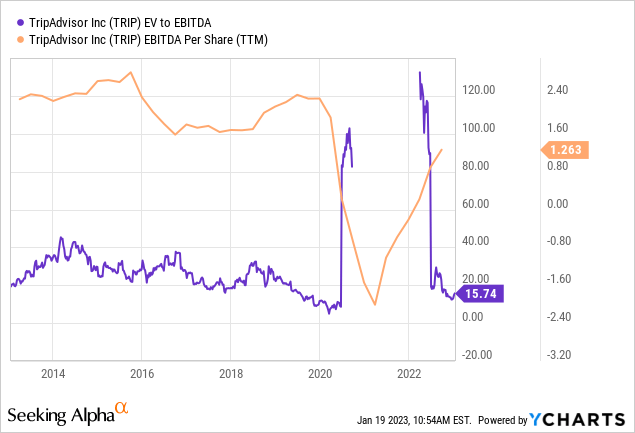

Additionally, when looking at the company’s EV to EBITDA ratio, we can see that the ratio has descended back to levels seen before 2020 – while EBITDA per share has seen a strong rebound.

ycharts.com

In this regard, I take the view that given the company’s EV to EBITDA ratio along with recent performance – Tripadvisor may be undervalued at this point.

Looking Forward

Going forward, I take the view that the trajectory for the stock in the more immediate term will be driven by macroeconomic conditions. With fears of a global recession this year, it might be a possibility that the strong rebound in revenue to 2019 levels may be peaking. Indeed, if revenue growth in subsequent quarters comes in below expectations – then further downside in the stock cannot be ruled out.

Additionally, while the company’s short-term cash position has been encouraging – investors are likely to pay attention to whether Tripadvisor can utilize recent revenue growth to reduce the long-term debt load accrued since the pandemic.

Conclusion

To conclude, Tripadvisor has seen a strong rebound in revenues and its short-term cash position is quite impressive. Moreover, the stock seems to be attractively valued from an earnings standpoint.

The main concern for Tripadvisor at this point is whether the rebound in revenue growth can continue – or whether economic conditions and a potential fizzling out of the post-COVID recovery in travel demand will limit further growth.

With that being said, I take the view that the stock could have significant upside potential in the case that revenue growth continues, and travel demand has not shown a particular slowdown in the face of rising prices.

For these reasons, I take a bullish view on Tripadvisor.

Be the first to comment