imaginima

VAALCO Energy, Inc. (EGY) is buying TransGlobe Energy Corporation (NASDAQ:TGA) in a stock-for-stock strategic business combination. VAALCO will acquire each TransGlobe share for 0.6727 of a VAALCO share of common stock

If VAALCO Energy stock holds, this implies $3.8 in value per TransGlobe share. The spread looks to be at around 6.44%. My guess is this transaction will take between 100 and 170 days to clear. Most likely somewhere around 137 days. It seems like a transaction that’s highly probable to clear (think odds of 95%~). The expected return for a transaction at these prices could be into the double digits.

The valuations on both sides are fairly undemanding (more about that later). I think the downside risk on TGA is limited. In fact, I happened to hold a small position in TGA before the deal was announced. A position I acquired at higher prices as I thought the valuation looked undemanding at that level.

For every 100 shares of TGA one goes long, one needs to hedge by selling ~67 shares of EGY. There is not a lot of market risk in a transaction like that because it is both long/short in equal amounts.

However, if the deal goes awry, there is still quite a bit of downside. Some of the worst scenarios are one where an activist comes in and tries to prevent EGY from completing the acquisition. In that case, EGY would reverse the pressure on its share price (already 15%) and TGA drops back down to the pre-deal price (also 12% down). In that case, the arbitrageur is losing a lot of money on a position that looked to have little risk. These things do happen, so keep that in mind when getting involved.

Valuation levels TGA and peers (Seeking Alpha)

To me, this wasn’t an arbitrage, to begin with. I already liked TGA stock at these valuations, to begin with. I pulled up a valuation table of TGA and peers from Seeking Alpha; the stock was trading at 2.6x earnings, 1.45x EBITDA and barely above book value. It had a market cap of $230 million and net cash of some ~$30 million.

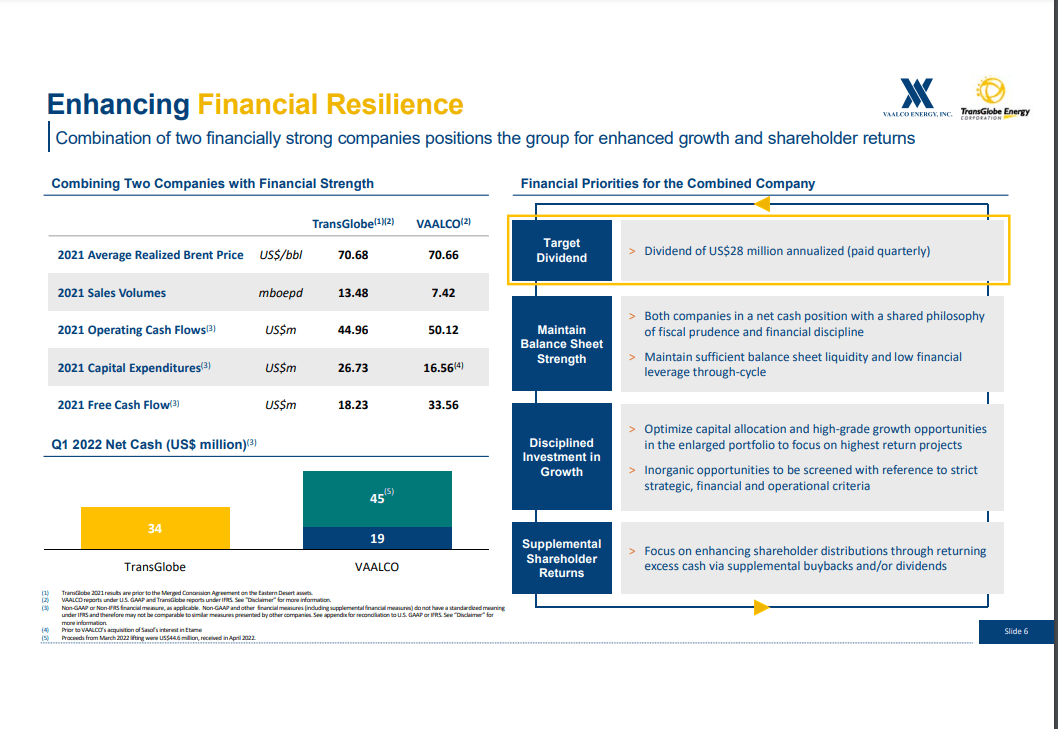

The combined company is more clearly an Africa-focused company. I’m usually not buying into scale advantages much for E&P producers with production sites that aren’t connected, but these are such small companies, there may be some upside to cutting out management overhead over time. Combined enterprise value will be around $550 million. The deal presentation shows the combined companies generated $94 million in operating cash flow and $52 million in free cash flow. I’d argue the majority of the CapEx budget went to production growth and isn’t so much maintenance CapEx.

TGA deal presentation (TGA)

These companies have a combined net cash position of nearly ~$100 million. Last year’s cash flow was achieved with average Brent prices of $70. This year, Brent has barely touched below $80 for a brief second.

TGA trades at roughly ~1.49x EBITDA, 1.06x book value, TTM P/E of 2.5x and around 9x free cash flow (I don’t mind because I think a large portion went to growth CapEx). The acquirer also trades at a P/E of 2.5x, EV/EBITDA of 1.5x and 2.3x book and 7.7x free cash flow. The combination still has net cash and may be able to get rid of some costs over time (even maintaining a listing is pretty expensive for such small companies).

I’m going to hold onto my TGA shares for now. I’m not going to bother hedging out EGY because I did not intend for this trade to be an arbitrage trade, to begin with. The combination still looks really good to me as a long-term standalone investment based on fundamentals.

Be the first to comment