PM Images

Investment Thesis – Uncertain Advertising Spend Ahead

Trade Desk, Inc. (NASDAQ:TTD) has recorded impressive growth thus far, in direct relevance to the success achieved by its key partners, such as Walmart (WMT) and fuboTV (FUBO). WMT reported excellent advertising growth of over 30% in FQ3’23, comprising 40% within the US through Walmart Connect and India through Flipkart Ads. These have incidentally contributed to the growth of its e-commerce sales within the US by 16% YoY. FUBO has reported even better results, with ad revenues growing by 113% YoY, attributed to the improved impression following the adoption of TTD’s UID2 since February 2021. This has resulted in the expansion of advertising spending on FUBO’s platform by 61% YoY, with retailers similarly witnessing improved conversion rates by 25% and ad returns by 14%.

Part of these successes is attributed to TTD’s growth-at-all-costs strategy over the past few quarters. The company has been reporting expanded operating expenses and narrowing profit margins over the last twelve months (LTM), despite the sustained gross margins at ~81%. Operating expenses have grown by 85.69% sequentially to $1.22B over the LTM, with $0.57B attributed to its similarly expanding Stock-Based Compensation (SBC) by 341.17% simultaneously. Most importantly, its R&D efforts have also been increasing sequentially by 40.65% to $298.23M in the LTM, with a heavy emphasis on SG&A expenses at 76.67%. This might explain its improved partnerships with multiple global brands, as discussed above.

TTD’s scaling-up process is highly evident from these indicators, with excellent success thus far. However, we are unsure whether the high growth will continue in the short term, due to the worsening macroeconomic outlook. The rapid increase in the company’s expenses has also impacted its GAAP profitability to net income margins of -0.7% by the LTM, compared to FY2021 levels of 11.5% and FY2020 levels of 29%. As these expenses grow, we may see its margins further compressed over the next few quarters.

In addition, market trends are already showing signs of reversal from the post-reopening cadence. Connected-TV companies such as Roku (ROKU) specialize in displaying ads to their streaming consumers, with Disney (DIS) and Netflix (NFLX) similarly launching their ad-supported tiers in December 2022. The latter recorded impressive growth in sales by 55.5% in FY2021, attributed to the expansion in its digital advertising segment and its media partners’ robust promotional spending then. Notably, the Connected-TV platform is also TTD’s fastest-growing channel and most significant revenue driver.

However, ROKU has reported a notable deceleration of revenue growth at 11.97% YoY to $761.37M in its latest quarter, with a lower-than-expected FQ4’22 guidance of $800M in revenues compared to consensus of $894.63M. This number will indicate a decline of -7.54% YoY, despite the usually exuberant holiday season. It is no wonder that market analysts have been bearish about ad-spending prospects during these uncertain times, further worsened by the company’s decision to cut costs by laying off 5% of its headcount through 2023. Steve Louden, CFO of ROKU, said:

As we enter the holiday season, we expect the macro environment to further pressure consumer discretionary spending and degrade advertising budgets, especially in the TV scatter market. We expect these conditions to be temporary, but it is difficult to predict when they will stabilize or rebound. We therefore anticipate Q4 Player revenue and Platform revenue to be lower year over year. (Seeking Alpha)

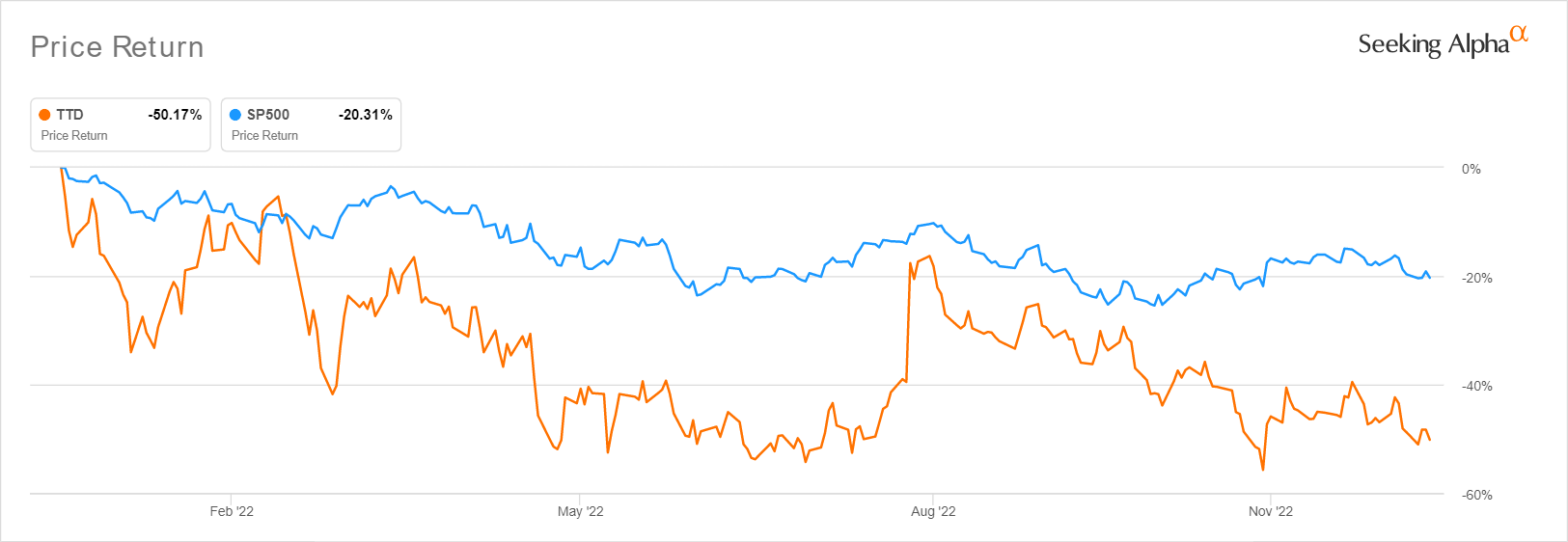

TTD YTD Stock Price

Seeking Alpha

Therefore, it may be prudent to exercise more caution since the TTD stock may remain volatile in the short term. Analysts are now projecting a 70% chance of recession in 2023, potentially brought about by the Fed’s projected terminal rate of 5.1%. The S&P 500 Index is trading sideways after a -20.31% YTD decline as well, with the TTD stock faring worse at -50.17% at the same time. While the global digital advertising market is expected to grow from $537.01B in 2021 to $1T by 2027 at a CAGR of 10.92%, investors may be better rewarded with patience for now.

TTD Is Inherently Over-Valued Compared To Its Ad-Tech Peers

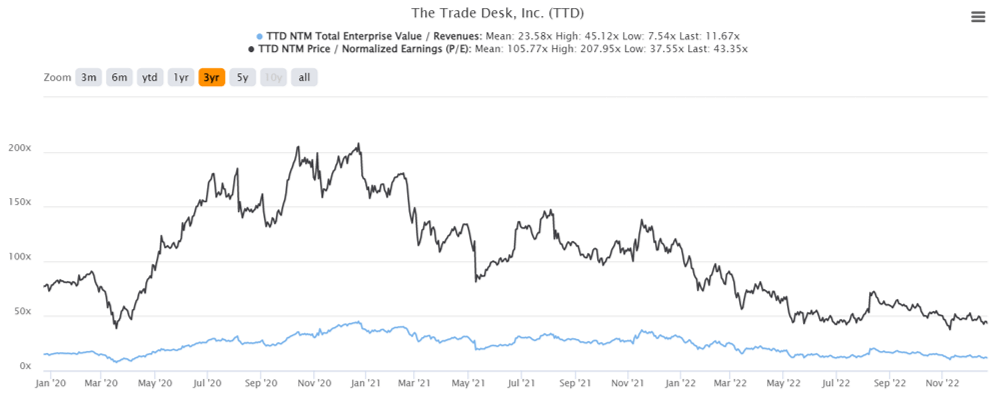

TTD 3Y EV/Revenue and P/E Valuations

S&P Capital IQ

TTD is currently trading at an NTM P/E of 43.35x, lower than its pre-pandemic 3Y mean of 54.64x and pandemic 3Y mean of 105.77x. The worsening macroeconomics have naturally further moderated its valuations against its YTD mean of 61.60x. However, we would like to highlight its rich premium compared to other ad-tech companies, such as PubMatic (PUBM) at NTM P/E of 19.46x, Digital Turbine (APPS) at 10.40x, Magnite (MGNI) at 14.52x, and ironSource (IS) at 12.38x.

Based on TTD’s projected FY2024 EPS of $1.46 and current P/E valuations, we are looking at a moderate price target of $63.29. On the other hand, consensus estimates proved to be more bullish, with a target of $71.67, indicating an excellent 59.62% upside potential from current levels. We are not surprised by the confidence since the stock has historically traded at higher P/E valuations.

This is also attributed to TTD’s accelerated growth at a projected revenue CAGR of 26.1% and EPS CAGR of 16.9% through FY2024. However, the optimism may be overly done, since APPS is expected to similarly deliver 36.9%/28.6%, MGNI 17.9%/28.6%, and IS 27.1%/14.4% through FY2024, respectively. It remains to be seen if the company is able to grow according to the market’s outsized P/E expectations.

Another contributor has highlighted that TTD has a robust moat worth its premium P/E, with a massive potential to bring the stock value by 757.23% to $340 by 2031. The latter coincides with the CEO compensation package of $830M, with 8 tranches to be vested according to the company’s stock price milestones. While we agree with the contributor, those numbers would indicate an aggressive forward EPS of $13.60, assuming P/E valuations of 25x. It would require the company to deliver a consistent EPS CAGR of at least 31.05% over the next ten years.

While the TTD management has previously delivered an EPS growth of 40.6% between FY2019 and FY2022, this was only possible due to the massive boom in ad-spending post-reopening cadence. With the worsening economic landscape, we would likely see drastically tightened corporate spending moderating its EPS growth through FY2024, as projected by market analysts at 16.9%. While ad-spending may rebound from FY2025 onwards, the company would need to catch up for the previous shortfall and record an ambitious EPS CAGR of 37.55% through FY2031.

While TTD may eventually deliver its aggressive growth trajectory through 2031, we prefer to exercise caution while revising our entry point to the low $30s, based on its peers’ YTD P/E mean of ~25x. This number would provide investors with an improved margin of safety for portfolio growth over the next decade. Meanwhile, those with higher risk tolerance may consider nibbling at current levels, since the stock is already trading at its historical support level, potentially lowering their dollar cost averages. However, portfolios should also be sized appropriately in the event of volatility, since these pessimistic sentiments are unlikely to lift in the short term.

Be the first to comment