scanrail/iStock via Getty Images

Townsquare Media (NYSE:TSQ) is a name we have discussed before and highlighted why we think that the company can trade higher as they continue to grow the digital business. Unlike their larger peers within the industry, Townsquare Media has spent the past few years hyper-focused on transforming from a broadcast radio company into a company which uses its legacy broadcast radio assets and steady cash flows to build out a digital business which will transform the company into its next version. Our belief is that the radio business is a cash flow generator, which Townsquare can utilize to build out a new business focused on selling additional services to current clients that in the long run should receive a higher multiple/valuation from investors – especially as Townsquare ventures into new geographic markets outside of its current geographic footprint (the new facility in Arizona and bolt-on acquisitions such as the Cherry Creek Broadcasting purchase).

With that said, we thought that the company’s Q3 results were acceptable in light of the weakening economy and mixed ad sales results from other media companies. While the company highlighted year-over-year growth, we think the quarter-over-quarter change was the real story.

Earnings

So Townsquare would probably prefer that we simply read the headline that the company achieved “all-time Q3 high for both net revenue (+8% Year-Over-Year) and adjusted EBITDA (+6% Year-Over-Year)” and skip analyzing some of the numbers. The fact of the matter is that the company missed analysts’ estimates on both the top and bottom lines, saw quarter-over-quarter results for revenues and adjusted EBITDA actually fall, and took no action to divest itself of the digital assets (crypto) that have lost more than half of their value over the past year (and to be clear, the 50%+ loss is not from a high-water mark, but from their actual cost basis).

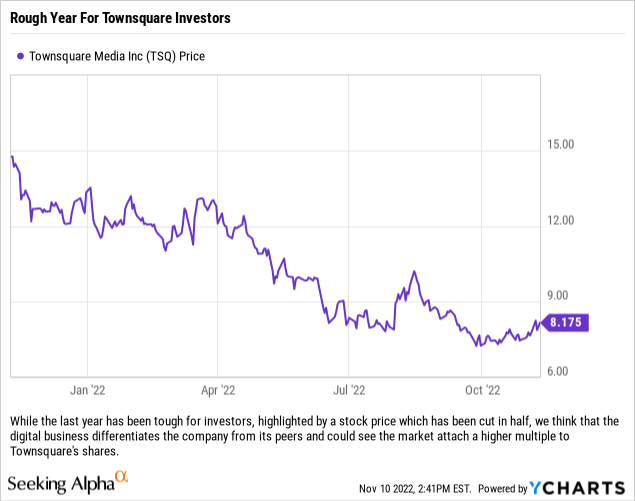

While YoY results appeared strong, the QoQ results were down during a quarter many expected to show growth. (Company Financials, Author)

So while the year-over-year results were impressive for an old-line media company, the quarter-over-quarter results show us that Townsquare is not immune to the overall ad market slump that has been showing up in other media companies’ results. To be clear though, this is not a situation where we feel that the results were horrible, we actually think that the company did a good job in the quarter. However, next quarter is going to be the ‘tell’ for investors as we will see how well the Townsquare Interactive/Ignite products hold up along with the company’s traditional broadcast business in what looks to be a weakening economy.

It is only fair to note that the company did report revenue and adj. EBITDA which were in line with their guidance, but it was on the low end for revenues – and when looking at revenues specifically the range was $120-$127 million with the company just barely exceeding the low end of that range.

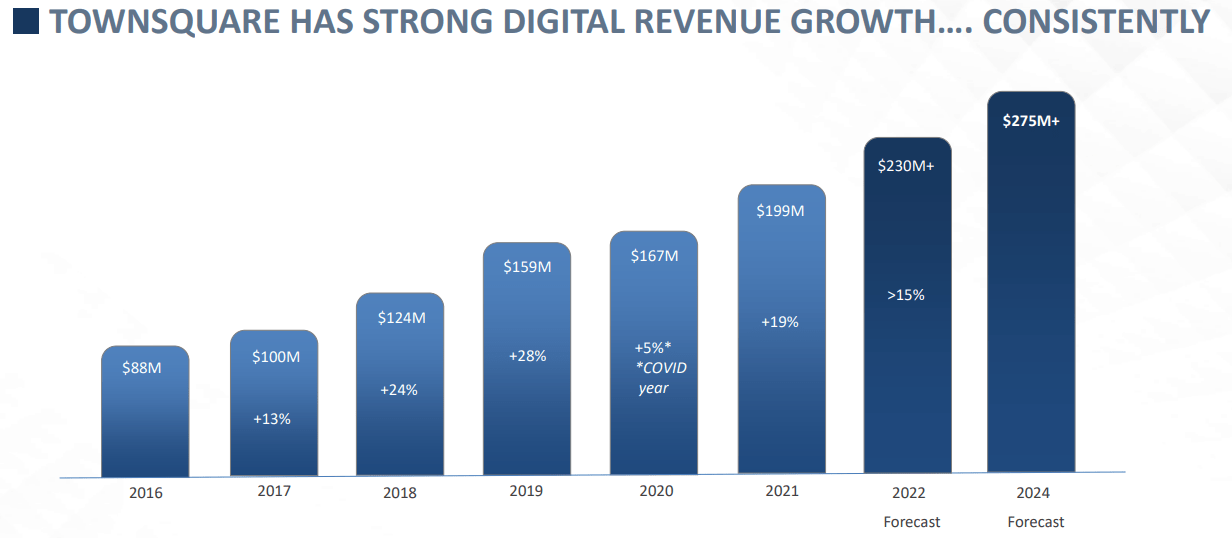

The good news coming from this report is that management reaffirmed their forecast for the digital side of the business to meet or exceed the $275 million+ revenue guidance they have been discussing for that side of the business. The FY 2022 guidance is for $230 million+, which would represent an increase in revenues of over 15% YoY. This is important, especially if the ad environment is going to be changing due to weakness in the economy, because Townsquare Ignite (digital advertising), which makes up about 30% of the company’s overall revenues and is the biggest driver of revenue and profit growth for the company overall, and Townsquare Interactive (digital marketing solutions), which is roughly 20% of overall revenues and provides steady subscription revenue, can help offset weakness in the historic broadcast business while also helping prop up margins as the company leverages up the new initiatives that it has already put in place starting in late Q1 2023. Diversified revenue streams (outside of audio) which are extremely profitable differentiate the company from peers and should provide investors with some comfort if the ad market continues to deteriorate.

Management reaffirmed the 2024 forecast for $275 million+ in digital revenues. (Townsquare Media Investor Presentation)

Political Ad Spend

According to management’s prepared comments on their conference call, one of the main issues for the company in 2022 – which showed up in Q3 results and will be more pronounced in Q4 – is a major decline in political ad spend. Political was a problem, not because of the radio medium but rather a lack of competitive races, or major Senate races, within the company’s geographic footprint. In Q3, the company booked $1.6 million in political ad spend, and now that the election season has concluded (and the company does not own any stations in Georgia where a run-off will take place) management expects total political ad spend for the year to come in at around $7 million. That is at least $5 million short of management’s previous expectation of $12-$13 million in political ad spend for 2022.

While this is pretty disappointing, it does fall in line with some of the other results we have seen from other radio and television broadcasters (and it must be noted that some of those companies actually have large footprints in very politically competitive areas). The company expects 2024 political ad spend to rebound as the problem this cycle was not radio (which actually saw increased interest) but their footprint. In 2024 (a Presidential election year) there will be key races that the company should be able to capitalize on, including Senate races in Arizona, Maine, Michigan, Montana, and Texas.

New Competition

We discussed in another article that others are following Townsquare into the digital solutions business to leverage their sales teams and customer relationships to gain more of those customers’ ad spend. Cumulus Media (CMLS) has a new product that they are aggressively advertising on their radio stations in certain markets called Cumulus Boost, and although there is not a huge overlap in radio markets for the two companies, they will probably compete for state/regional small business accounts as the digital business’s borders are not constrained by an antenna.

Right now we do not think that this new competitor is going to impact Townsquare’s growth plans, but it is interesting that others (especially Townsquare’s peers) are entering the business.

Our Take

The political ad spend result, and guidance, were disappointing as was the company’s lowered guidance for the full year. Headwinds are building, with auto advertisers still on the sidelines (in both radio and digital) and economic issues continuing to impact consumers and businesses. The good news for the company is that it has less competition in its markets for ad dollars, and only about 5% of its total revenues are derived from national advertising.

Townsquare continues to transform its business and with the opening of the new office in Arizona for its digital businesses, investors could see a tick up in revenue later on in 2023 before larger increases in 2024. With the large digital business, we suspect that Townsquare can withstand a harsher downturn in the ad market, especially if their digital subscription revenues hold up during an economic downturn.

While a lot of the deleveraging that has occurred on the balance sheet has been due to EBITDA bouncing back, we do like that management has been repurchasing debt, which is true deleveraging and frees up cash flow to be directed elsewhere.

There were a few unpleasant surprises in the current quarter, but we still think that Townsquare Media is a stock that investors should continue to own moving forward. The digital business should continue to provide strong growth, and if ad demand comes back, investors would benefit from the added leverage from both broadcast and digital.

Be the first to comment