William Thomas Cain

Investment Thesis

Company Overview

Toll Brothers (NYSE:TOL), founded in 1967 in Pennsylvania, is a company that designs, builds, markets, sells and arranges financing for residential and commercial properties in the U.S., where the luxury residential market is its primary focus. The company reports its total home-building assets by regions as the following, North, Mid-Atlantic, South, Mountain, and Pacific.

Strength

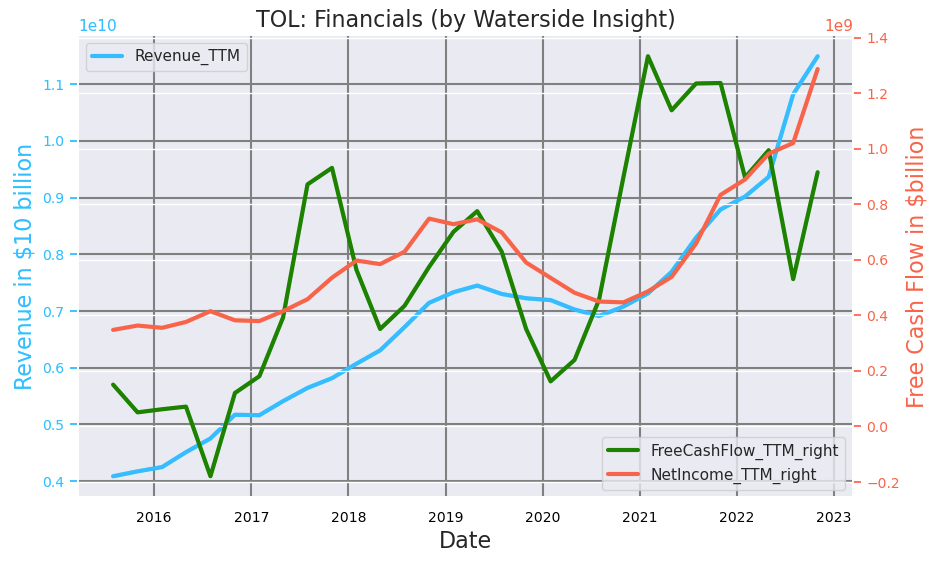

It was a banner year in FY 2022 for the Toll Brothers. The company’s revenue, net income, and cash flow are all at or near their highest levels in its history. Although the company mentioned that the first and second half of 2022 were very different, that it started to experience a slowdown in 2H, its financials for the FY 2022 nonetheless turned out to be strong.

Toll Brothers Financials (Calculated and Charted by Waterside Insight with data from the company)

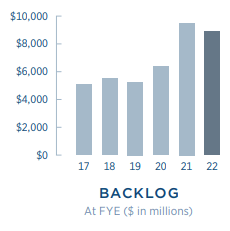

Toll Brothers indicated it has an $8.9 billion backlog of nearly 8,100 luxury homes currently sitting on its book. 90% of the backlog will be delivered by October this year. It is a solid support for its revenue when the housing market is experiencing one of its most significant downturns since 2008. And there is little worry about cancellation since the nonrefundable deposits for the backlog are averaging $83,000, and the amount of work to personalize the home that went into the preparation. Not to mention 25% of that backlog will be paid in cash.

Toll Brothers Backlog (Toll Brothers 2022 10-K)

Both the stellar performance and the backlog going into 2023 would be crucial for the company to weather the storm of a looming recession and slowdown in the housing market.

Weakness/Risks

Challenges ahead remain, and the weakness of the housing market still shows up in several places in the Toll Brothers’ financials.

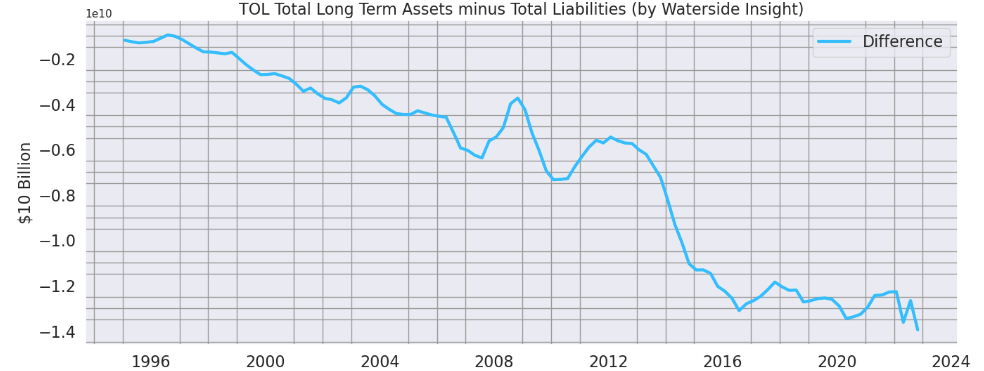

By the end of FY 2022, about 80% of its current asset was in inventory. This ratio has always been between 80-90% in recent years. Declining home prices and the housing market will cause higher inventory impairment charges on its books and undoubtedly brings down its asset value. Currently, its long-term liabilities have already exceeded long-term assets by the largest amount since a long time ago.

Toll Brothers Long Term Assets vs Liabilities (Calculated and Charted by Waterside Insight with data from the company)

Some of its long-term liabilities are loans payable for itself, which could be subject to higher interest rates, while certainly, some of the liabilities are the mortgage loans it lent out to high-income home buyers. This group of buyers supposedly should have higher creditworthiness that is resilient to the economic downturn. Nonetheless, it’s a risk. Looking at its numbers in FY 2022, the aggregate unpaid principal balance has exceeded the fair value of the mortgage loans held for sale.

Toll Brothers: Mortgage Loans for Sale (Company 2022 10-K)

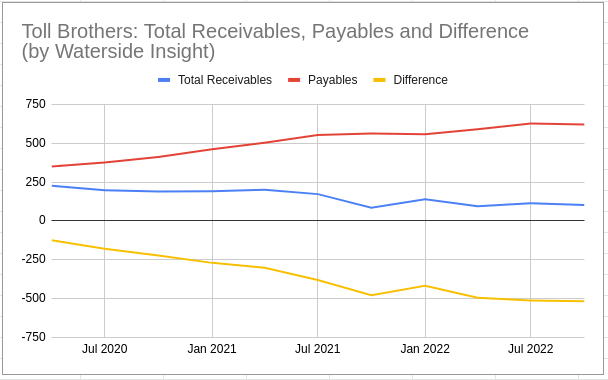

Its cash conversion rate is continuously deteriorating since the pandemic.

Toll Brothers Account Receivables vs Payables (Calculated and Charted by Waterside Insight with data from the company)

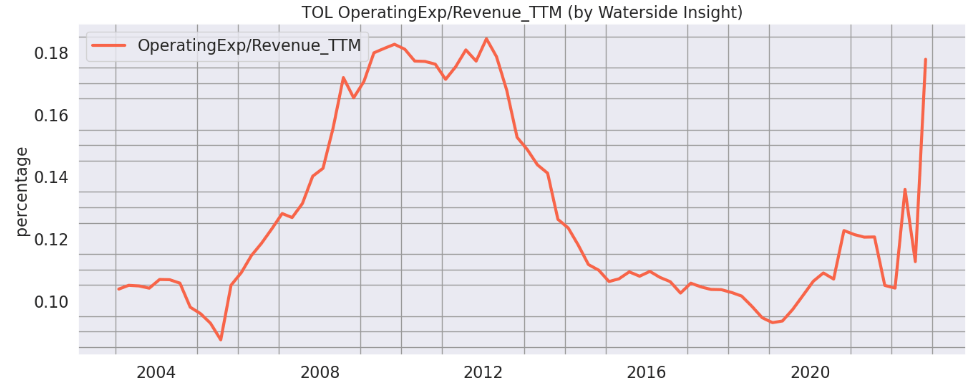

The company’s operating expenses as a percentage of revenue have gone straight up in the last few quarters, reflecting supply chain constrain, labor shortage, and several other factors that may not go away very soon. It is approaching the high levels before and during 2008.

Toll Brothers Operating Expenses/ Revenue (Calculated and Charted by Waterside Insight with data from the company)

Toll Brothers mentioned in its 10-K that the comparison with the period of 2006-2009 shows how similarly the company coped with the challenging market dynamics. So we plot its earnings and operating expenses going back to 1990. We saw that when earnings from operation exceeded its operating expenses by a large portion before the crash of 2008, and then it went into a prolonged slump. In its last quarter, this difference has reached a new high. What will come next?

Toll Brothers OpEx vs Earnings from Operations (Calculated and Charted by Waterside Insight with data from the company)

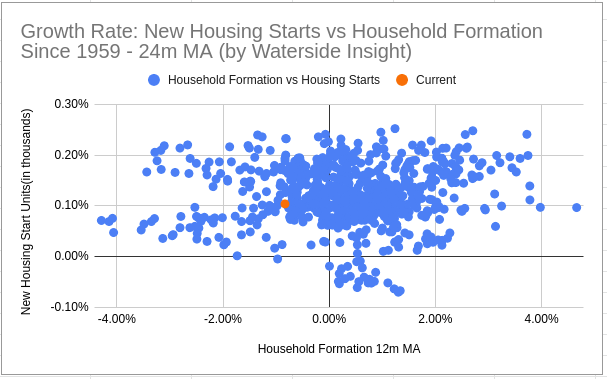

The company mentioned that the fundamentals in the housing market are different this time since household growth has outpaced the new housing units started, and the lack of supply will continue to support the market for new homes. We looked at the data from FRED, and it doesn’t seem like we are out of the norm currently. We use the monthly growth rate for both new housing starts and the number of households since 1959, and take a 24-month moving average to capture a trend over a more extended period. We are currently in a negative household formation growth and positive new housing starts, which is just about average, given the historical data. There isn’t a substantive shortage of new housing units coming to the market for households currently.

U.S. Household Formation vs New Housing Starts (Calculated and Charted by Waterside Insight with data from FRED)

We plot Toll Brothers’ free cash flow against the moving average data of the higher-frequency housing index by Zillow, with the latest date ending in December 2022. The company’s current free cash flow is very much an outlier. If history is any guide, should the housing market goes down, its free cash flow could be impacted and drop by almost 40% to regress back to the central cluster and still be considered at a normal level. Indeed, historical data doesn’t fully predict the future. But we don’t see anything fundamentally changing about the company’s operation and market dynamics that will establish a new cluster around this outlier.

Toll Brothers Free Cash Flow vs Zillow Housing Index (Calculated and Charted by Waterside Insight with data from the company, Nasdaq Data Link)

Coming 2024, if we look ahead when 90% of this backlog is delivered by October this year, the next fiscal year will probably see a cliff drop in its contracts. The company’s net signed contract declined by 60% in the second half of fiscal 2022 compared to the same period of the prior year. Assuming a similar number in 2023 for contracts signed, the underlying weakness from here forward shouldn’t be overlooked.

Financial Overview

Toll Brothers Financial Overview (Calculated and Charted by Waterside Insight with data from the company)

Valuation

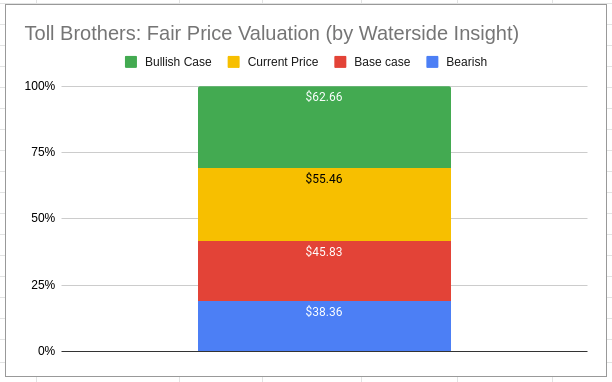

We consider all the analyses above and use our proprietary models to assess Toll Brothers’ fair value by projecting its growth prospects ten years ahead. Due to the economic cycle of the housing market and the impact on Toll Brothers’ performance, we assume a certain cyclicality in our projection. And in all cases, we project has negative cash flow for ’23 and ’24, with the majority of the hit shouldered in ’24. In our bullish case, the company makes a strong recovery with less volatility; it was priced at $62. In our bearish case, the company makes a volatile yet less robust recovery; it was priced at $38.36. In our base case, it makes a gradual recovery; it was priced at $45.83. We see the base case as a reflection of the uncertainty and the path of a continuous rate hike impacting the broader economy and the housing market. Currently, the market is more optimistic than our base case scenario.

Fair Price Valuation for Toll Brothers (Calculated and Charted by Waterside Insight)

Conclusion

With a more affluent customer base and large order backlog going into 2023, Toll Brothers has built up a cushion to weather the housing market downturn. Yet, the broader market weakness has started to show in the company’s financial performance. A changing housing market dynamics and strong cyclicality in the company’s historical data suggest an impending downturn could be in play for the company. We see little upside from here, and the current price is too optimistic for the near term. We recommend a hold for the stock.

Be the first to comment