William_Potter

Historically, one of the most popular allocation strategies has been to allocate 60% in stocks and the remaining 40% in bonds. There are some variations of this strategy but the idea is simple:

The stock component should provide high total returns during bull markets, while the bond component should provide income and stability during bear markets.

When stocks dip, bonds typically remain stable, and therefore, this strategy also allow you to opportunistically buy the dips as you rebalance capital from bonds to stocks during bear markets.

This should lead to superior risk-adjusted returns over time and several studies have proven the benefits of this approach.

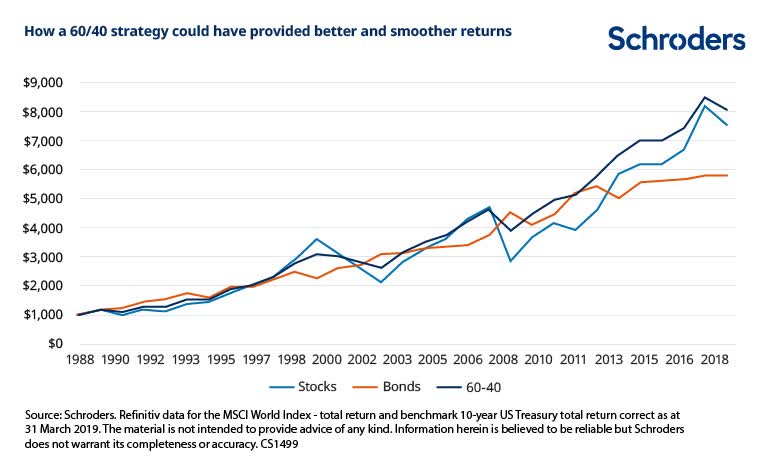

Below, you can see that the 60/40 portfolio has not only been safer, it has also been more rewarding than a portfolio that’s fully invested in stocks (SPY):

Shroders

But before you blindly structure your portfolio after this model, you need to consider that today’s environment could be particularly dangerous to this allocation strategy.

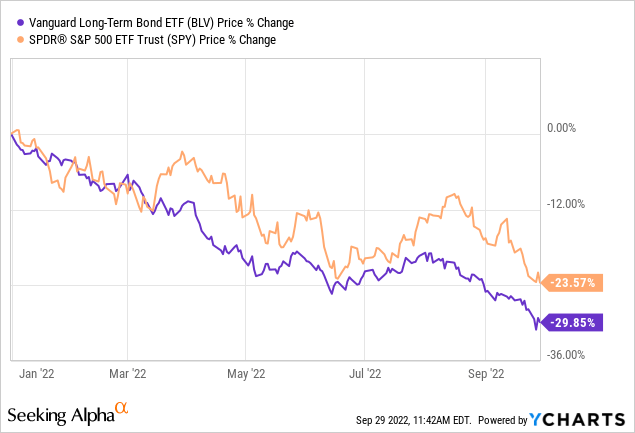

In fact, since the beginning of the year, the 60/40 portfolio has lost % in value, which is one of the worst drops for this strategy:

Could the losses get even worse?

We don’t know, but even if the market bounces back, we think that the 60/40 portfolio strategy is now outdated and some adjustments are needed for today’s evolving world.

Below, we discuss the biggest issues of the 60/40 portfolio, and finally, we explain how we are structuring our portfolio to mitigate risks and optimize future upside potential.

Increased Correlation Between Stocks and Bonds

The basic idea of the 60/40 portfolio is today broken.

Stocks and bonds have become increasingly correlated and therefore, bonds don’t provide the stability that they used to.

You can clearly see this in the performance of both asset classes in 2022:

Why is this?

Historically, when we have hit a recession and stocks have plunged, bonds have remained fairly stable and in some cases even gained value because recessions have also led to lower inflation and declining interest rates. All else held equal, this should increase the value of bonds, especially as increasingly many investors turn to bonds for safety and bid up their prices.

But today is different

Inflation is currently at a 40-year high, hitting 8.3% in August, and the Fed needs to urgently bring it back under control.

Unfortunately, this high inflation is happening even as the economy is rapidly dipping into a recession, which would typically warrant rate cuts, but this isn’t an option today.

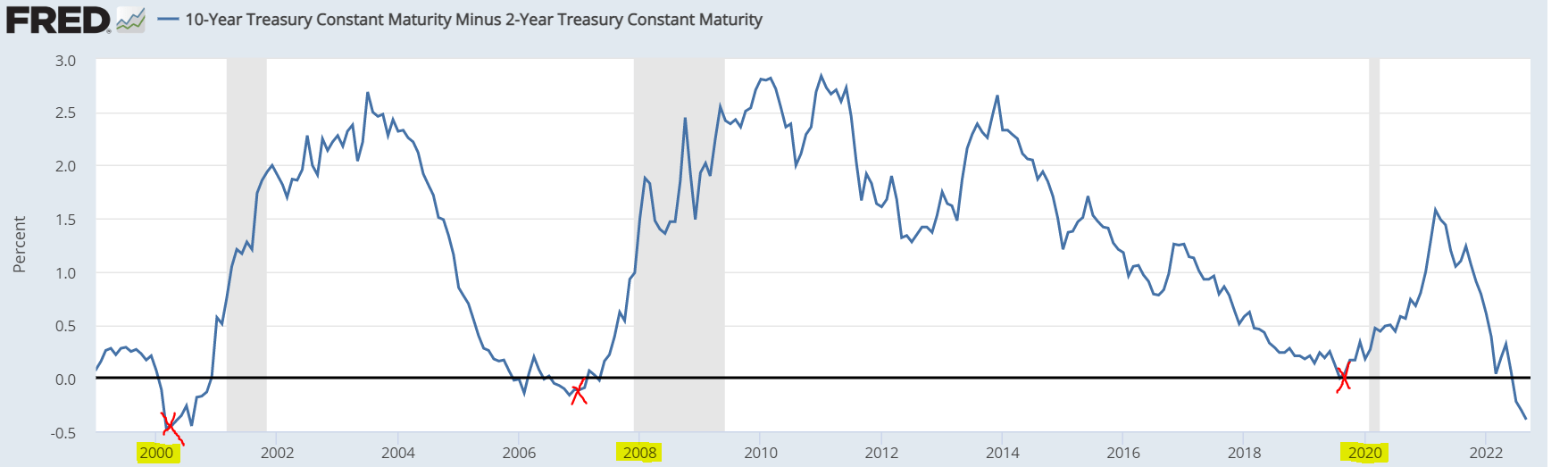

Therefore, the Fed is forced to aggressively hike rates even as we head into a recession, and this is well-reflected in the steeply inverted yield curve:

Federal Reserve

Even after many sizable rate hikes, today the Fed funds rate is still just 3.25% because we started from only 0.25% earlier this year. 3.25% may seem high compared to where it was earlier this year, but it is still very low compared to past funds rate history and our current inflation.

Therefore, many more rate hikes are expected in the near term, and the Fed made this clear at the latest meeting.

This puts both, bonds and stocks, in a tough position.

On one hand, bonds are suffering from high inflation and rising interest rates.

On the other hand, socks are suffering from the recession and rising interest rates. Many businesses are also very negatively impacted by cost inflation, the inability to pass price hikes to customers in a recession, and the strong USD caused by rate hikes.

So, both are now suffering, correlation is rising, and the past diversification benefits enjoyed by the 60/40 portfolio are disappearing. The only way out of this would be if inflation suddenly drops back down to normal levels and the Fed begins to cut interest rates, but how likely is that?

It is tough to say, but at least in the intermediate term, it appears unlikely, and therefore, you cannot simply rely on stocks and bonds in today’s world anymore.

Enter The World of Alternative Investments

Stocks and bonds are by far the most popular investments, and this is largely because they are easy to access. You enjoy liquidity, low transaction cost, and professional management, and you can easily build a diversified portfolio. There are also plenty of analysts providing research on stocks and bonds so you can efficiently access information on the latest opportunities.

But, in a weird way, this is potentially also the demise of stocks and bonds. These asset classes have become so crowded and competitive that it is now more difficult to find opportunities and most stocks/bonds have become closely correlated. The rise in popularity of passive ETFs and index funds have made it such that everything goes up or everything goes down, and diversification benefits are not as great as they used to be.

My solution is to invest heavily in alternative asset classes such as:

Farmland:

Farmland Partners

Apartment communities:

Armada Hoffler Properties

Private equity:

Global PMI Partners

Industrial warehouses:

EastGroup Properties

Private property loans:

EstateGuru

Overall, my exposure to alternative investments is today about 60% and the rest is mainly invested in traditional stocks. I hold very few bonds because I have a long-time horizon, high-risk tolerance, and I fear that bonds are set for more pain due to the high inflation and rising rates.

Why invest so heavily in alternatives?

There are many reasons, but here are the four most important ones:

- Reason #1: Diversification: You actually get to mitigate risks via diversification. As an example, the fundamentals of farmland are completely different from those of regular stocks or even bonds. Farmland REITs (FPI; LAND) benefit from the inflation as higher crop prices lead to higher property values and rents. You get real diversification benefits because the fundamentals are uncorrelated with the broader economy.

- Reason #2: Inflation-protection: Most, but not all, alternative asset classes offer better inflation protection, particularly those that are backed by real assets. Farmland, apartment communities, warehouses, etc., are all excellent examples. The high inflation leads to higher rents and higher replacement cost. Unlike many businesses, REITs and other landlord are able to pass rent hikes to their tenants because the real estate they occupy is growing is value and essential to them.

- Reason #3: Income: Today, a lot of alternative asset classes are heavily discounted, and as a result, they also offer high yields, particularly in the REIT market. To give you a few examples, EPR Properties (EPR) yields 9%, NewLake (OTCQX:NLCP) yields 11%, and W.P. Carey (WPC) yields nearly 6%. The high yield is great in today’s uncertain environment because it provides a steady return that’s independent of the market itself.

- Reason #4: Mis-pricings: The recent market crash has brought down a lot of listed alternative investments, including REITs (VNQ), BDCs (BIZD), and others. Many now trade at steep discounts relative to the underlying value of their assets, which essentially means that you get to invest in these alternative assets at a discount, and get the added benefits of liquidity, diversification, and professional management for free on top of it. To give you an example: Prologis (PLD), the leading e-commerce-focused industrial REIT, is today priced at an estimated 25% discount relative to the underlying value of its real estate, and the value of this real estate continues to grow. The rents on its new leases are up 20%+ in 2022, and the strong growth is expected to continue as more and more companies invest in e-commerce and bring larger portions of their supply chains back to the U.S.

So in short, I think that alternative assets, and to be more specific, listed real asset companies and private equity firms, have a lot to offer in today’s environment.

They often trade at large discounts to fair value, offer real diversification benefits, and high income while we wait for the recovery. Of course, they are not immune to volatility either. Most REITs are down significantly in 2022. But their fundamentals have remained strong as they benefit from inflation and aren’t heavily impacted by rates since they use little debt, and most of it is fixed rate and has long maturities.

This is why I prefer to invest heavily in these alternative investments instead of following the 60/40 portfolio strategy.

Be the first to comment