anilakkus/iStock via Getty Images

Unlock the power of a reliable and growing income stream by diving into the world of dividend growth investing – DGI. Sound companies reward you for your trust with increasing payouts year after year.

I recently wrote an article about three must-haves for DGI enthusiasts. I want to elaborate further on my strategy and have three new great DGI stocks for you.

Dividend growth investing is a strategy that involves investing in companies that have a history of increasing their dividends over time. The goal of this strategy is to generate a steady stream of income that grows over time, providing a hedge against inflation and a source of financial stability for investors. This strategy is designed for long-term investors who want to generate a steady income stream while potentially benefiting from the growth of the underlying stock.

Merits of DGI

- Regular dividend payments provide a source of income that can help meet living expenses or provide income for retirees.

- The ability of companies to increase their dividends over time provides a hedge against inflation.

- Dividend growth stocks have historically outperformed non-dividend-paying stocks over the long term.

Risks of DGI

- Rising interest rates may cause investors to move to bonds. Investors who wanted to do so during the current rate cycle may already have switched.

- Dividend cuts: companies may reduce or eliminate their dividends, which can negatively impact income and stock price.

- Concentration risk: focusing too heavily on dividend growth stocks in a single industry or sector can increase concentration risk.

- Focusing on high-yield stocks with strong past dividend growth but little future growth.

My Selection Method

I use a straightforward stock selection method to find undervalued growth stocks. It’s a strategy to find long-term winners with substantial upside potential.

Being undervalued doesn’t mean they trade at really low PE or EV/FCF ratios. The ratio in comparison to past growth and potential future growth is important.

- Substantial revenue per share growth.

- A sturdy balance sheet with low leverage.

- Reasonable valuation based on FCF and PE ratios relative to their growth.

- Stocks that return cash to shareholders with buybacks and/or dividends are often run by shareholder-friendly management. For this selection, I specifically look at dividend-paying stocks obviously.

I used the selection method before to pick three must-have DGI stocks.

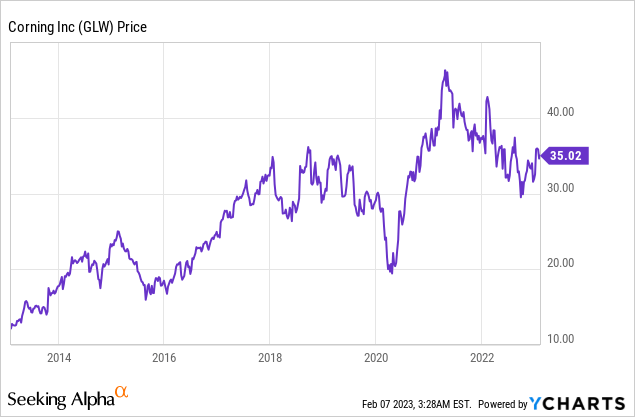

Corning (GLW)

Corning provides glass solutions for several end markets like displays, fiber networks, and solar panels. It has a broad product offering in specialized glass.

Several of its customer markets go through a tough time as shown by lower smartphone and PC sales. Corning manages the challenging environment very well with continued growth and a focus on profitability. Its diversified business also offers enough exposure to growing markets that mitigate the slump in consumer-facing end markets.

Corning

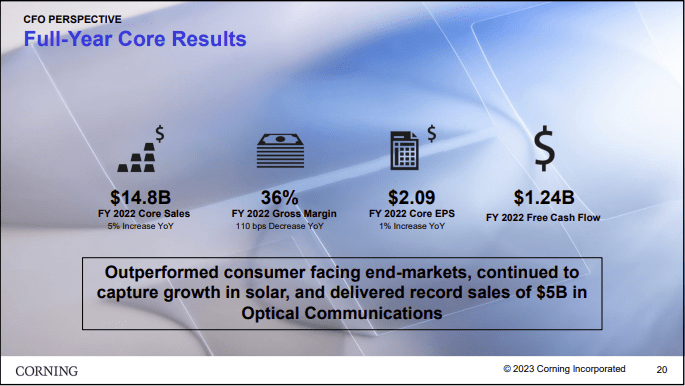

A 5% increase in core sales remains impressive when the economic situation is unfavorable.

Dividend Growth

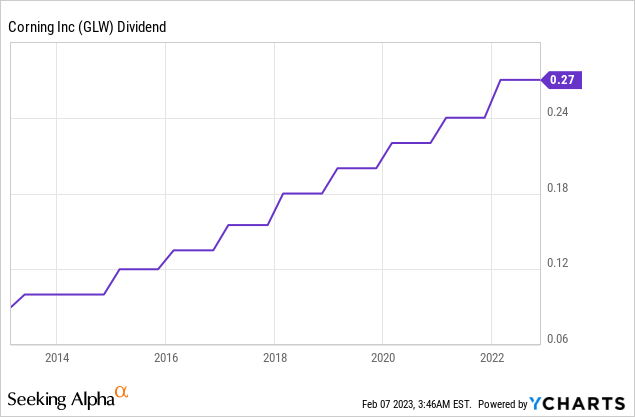

In the past 10 years, its dividend improved by 12.02% CAGR. Its annual dividend just increased by 3.7% to $1.12. The current slower growth makes sense as Corning already pays ~50% of its net earnings and 90% of 2022’s FCF. Free cash flow should improve over the next year back in line with its net earnings. When its end markets pick up again, there will be more room for higher dividend growth in 2024.

Valuation

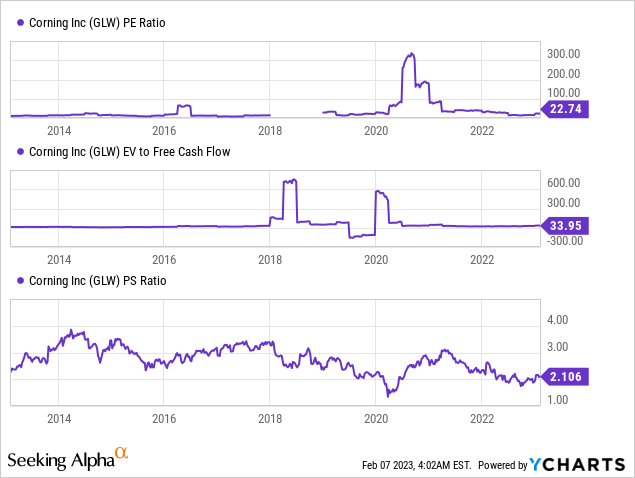

Corning is cheaply valued currently. PE and EV/FCF have been bumpy as their results weren’t as stable as the dividend. The PS ratio shows it’s on the low end of its 10-year history. It offers a 3% yield and has a substantial share price upside once the growth pace fastens.

Mare Evidence Lab provided an extended overview of the bull case for Corning recently.

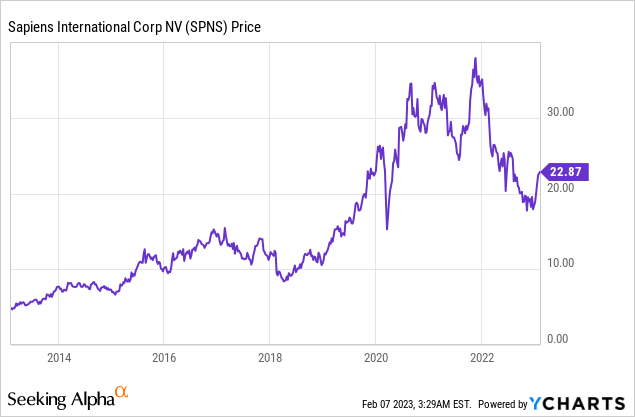

Sapiens (SPNS)

Sapiens is a technology provider for insurance carriers that want to transform their business digitally. Its sticky revenue model leads to strong organic growth. The company is based in Israel with substantial exposure to international currencies.

The currency headwinds of the past year slowed its growth. Additionally, large customers started to delay purchases due to the uncertain economic environment. Everything together made the stock drop like a rock. The current delays in purchases should be temporary and currency headwinds can fade quickly as well.

Its long-term tailwinds remain in place. Its modular and easy-to-implement software attracts new customers. It profits from offshoring and increased cloud sales. SPNS targets 8% to 11% annual growth.

Dividend Growth

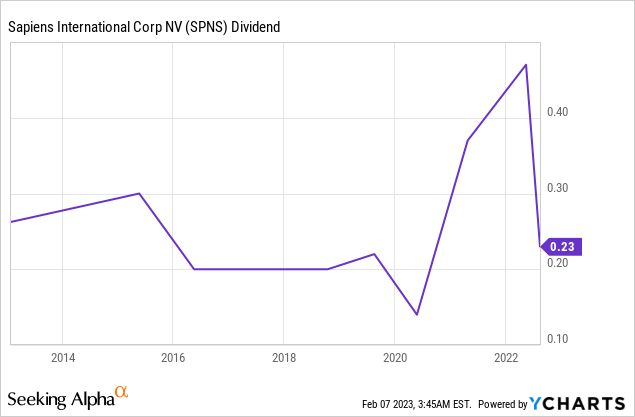

Sapiens switched from an annual dividend to a semi-annual dividend in 2022. That explains the apparent drop in dividends over the past year. The change is positive as its shows confidence in recurring free cash flows.

It distributes 40% of its non-GAAP net income as a dividend. Over time, the dividend should increase in line with the net income. Double-digit growth should be achievable.

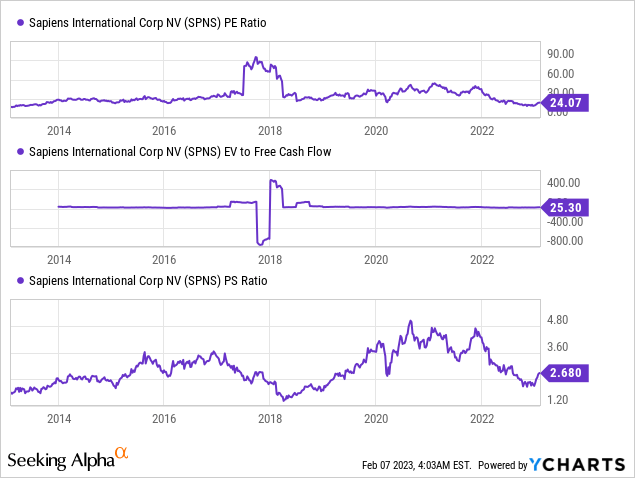

Valuation

Sapiens is cheaply valued in comparison to its history. It recently became a lot cheaper due to the temporary headwinds.

I wrote a comprehensive analysis of Sapiens in December.

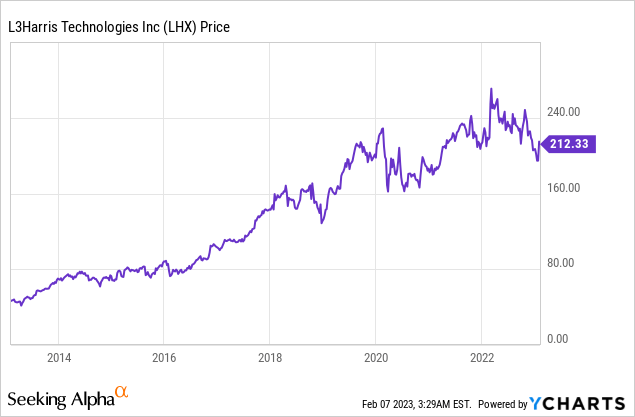

L3Harris Technologies (LHX)

L3Harris is an aerospace and defense technology company. The company shortly profited from the Russian invasion of Ukraine but couldn’t hold the initial gains as opposed to other defense contractors. It’s mainly due to supply chain issues.

LHX reforms the company with recent acquisitions. It increases its long-term growth potential and has a broad range of defense products and services.

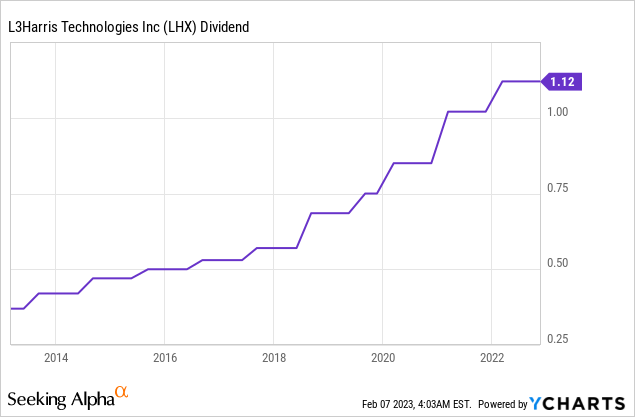

Dividend Growth

The company’s dividend is a priority for the management. Buybacks will get cut once recent acquisitions close, the dividend will keep rising. It managed to increase dividends at an 11.5% CAGR over the past 10 years. Double-digit growth is likely to continue.

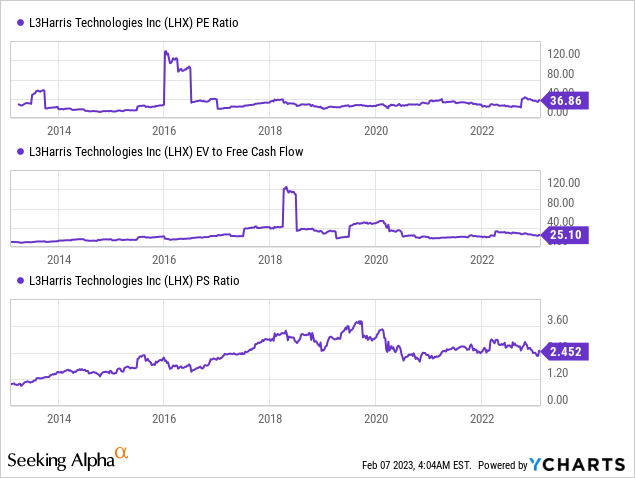

Valuation

The company underperformed its major peers like Lockheed Martin (LMT) over the past year. It still outperformed major indexes as the defense sector saw increased interest from customers and investors. The current valuation of LHX thus isn’t cheap but still leaves enough upside potential for investors with a long-term view.

Leo Nelissen offers an excellent overview of the company’s abilities.

Conclusion

Dividend growth investing can be an effective strategy for generating a steady stream of income, while potentially benefiting from the growth of the underlying stock. However, it’s important to understand the risks involved and diversify investments to mitigate them.

These three stocks can be a good start to a DGI portfolio.

Be the first to comment