FatCamera

Introduction

Thorne HealthTech (NASDAQ:THRN) shares continue to look strong at 11% YTD. Despite the fact that I like the market and its prospects in which the company operates, in my personal opinion, now is not the best time to go long. I think the company has fundamental upside potential in line with my DCF model, but in terms of momentum, I think investors should wait for next period reports.

Short survey of Q3 results

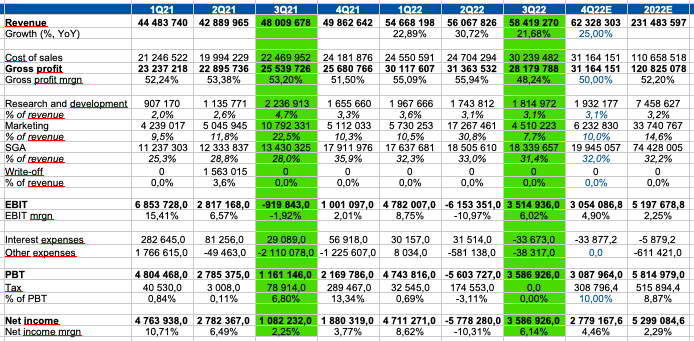

On November 9, 2022, the company published financial results for the 3rd quarter of 2022, which turned out to be worse than investors’ expectations. First of all, I would like to draw attention to the gross margin, which decreased from 53.2% in Q3 2021 to 48.2% in Q3 2022. According to management comments, the decline was caused by proactive early action, which resulted in an increase in the share of low-margin products.

Management announced a slight reduction in guidance for 2022. Thus, the company expects a low decline in revenue growth and continued decline in gross margin. You can see the details in the table below.

Company’s official site

Projections

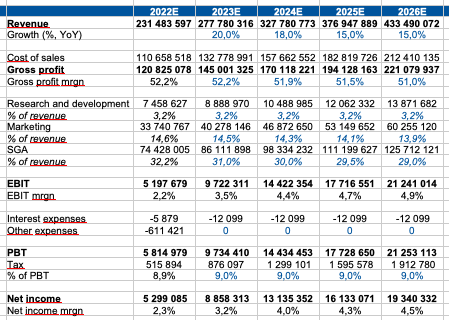

Revenue growth: in my model, I include a gradual decline in revenue growth against the background of: 1) a high base of previous periods 2) increased competition 3) market saturation

Gross margin: I am targeting a gradual decline in the gross margin from 52.2% in 2022 to 51% in 2026 as input costs rise and competition increases.

Research and development: I believe the company’s R&D spending needs to be kept stable, so I’m targeting 3.2% through 2026. Cost reduction R&D can lead to loss of competitive advantage.

Marketing: Also, I think we will see a gradual decline in marketing spending from 14.6% in 2022 to 13.9% in 2026. Despite the increase in economies of scale, I think that the company will not be able to more aggressively reduce marketing costs, because the reduction in marketing costs may lead to a slowdown in revenue growth.

SGA: Here I am assuming a reduction in costs from 32.2% in 2022 to 29% due to increased economies of scale and increased operational efficiency of the business

Quarterly projections:

Personal calculations

Yearly projections:

Personal calculations

Valuation

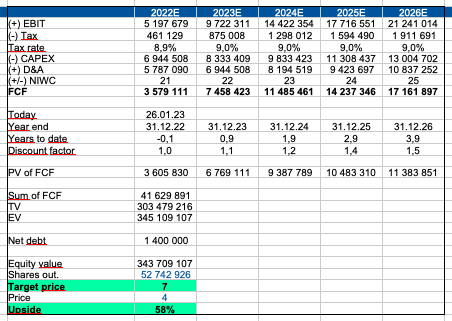

To value a business, I prefer to use the DCF method and calculate the resulting multiples for the company. I prefer DCF because:

1. The Company, its competitors and statistical agencies publish financial statements on a regular basis, on the basis of which we can make assumptions about the future cash flows of the business.

2. The DCF model allows you to reflect the improvement of the unit economy and economies of scale in the following periods.

The main assumptions of my model are:

WACC: 11%

Terminal growth rate: 7%

Personal calculations

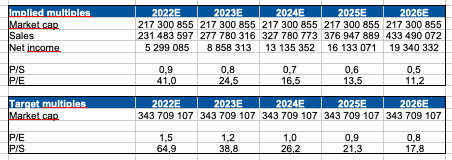

Multiples

Personal calculations

Drivers

Market growth: The growth of the dietary supplement market and the growing popularity of the company’s products may have a positive impact on revenue growth dynamics in the following periods.

Margin: Economies of scale from sales growth can allow a company to manage operating costs more effectively, which can support operating margins. In addition, changing the product mix in favor of more marginal products can have a positive impact on profitability too.

Macro: Declining inflation and growing consumer confidence may have a positive impact on the company’s revenue dynamics

Risks

Macro: Rising inflation and declining consumer income may have a negative impact on consumer demand for the company’s products

Margin: An increase in inflation and, accordingly, an increase in the company’s operating costs may have a negative impact on the operating profitability of the business.

Competition: Increasing competition, renewed competition on prices may lead to a decrease in market share, revenue growth and operating profitability of the business.

Conclusion

According to my DCF model, the fair share price is $7 with an upside potential of 58%. However, I believe that additional catalysts are needed for the growth of quotes. Thus, in my personal opinion, it is necessary to wait for reporting results of the next few quarters to make sure that the company is able to pass on the increase in prices to end consumers in order to maintain a stable level of operating margins. However, I really like the company and the market in which it operates.

Be the first to comment