mattjeacock/iStock Unreleased via Getty Images

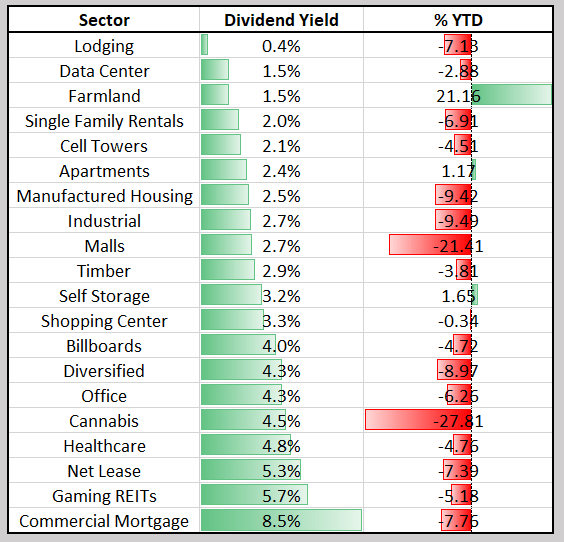

A few days ago I wrote an article titled “Think Like A Landlord” in which I said that “I think it’s extremely important for readers to think like the business owner because this is core to being a true value investor, and, of course, in the REIT sector this means that you must always “Think Like a Landlord.””

Today, I’m moving over to the mREIT sector. These are REITs that provide financing for income-producing real estate by purchasing or initiating mortgages and mortgage-backed securities, and earning income from the interest. They help provide essential liquidity for the real estate market. A few weeks ago, I wrote an article in which I explained,

Is it me, or am I seeing more and more articles espousing high yield?

I went on to explain that

if you had purchased NLY in 2003 and held onto shares until now, you would have generated annual returns of 3.6%.

I followed up that article with another one on Annaly Capital Management (NLY), in which I explained,

Many of my regular readers know I’m not a big fan of residential mortgage REITs. I’ve frequently warned investors to stay away from them, in fact.

Like most any investment, the more debt you use, the greater the potential for gain or loss. And when we buy stocks on margin, we’re leveraging investment returns with debt.

It’s well known that mortgage REITs (mREITs) own debt, not property. So the risks of investing in them are considerably elevated compared with other dividend-paying stocks.

They benefit when interest rates come down, which increases the value of the mortgages they hold. Essentially, it’s the beneficial use of borrowing money that magnifies returns (leverage).

That’s the reason spreads for mREITs are wider and dividends are much higher than equity REITs. To put in bluntly, as I’ve often argued, they don’t belong in a retirement portfolio.

Personally, I’ve avoided residential mREITs because they’re highly leveraged – which can make earning streams and dividend payments much more volatile. They tend to be more sensitive to interest rates.

A general increase – or even a significant change in the spread between short-term and long-term levels – can impact earnings substantially. And, because they don’t own easily valued real estate, valuing their shares can be equally tricky.

Commercial mREITs, however?

I’ve definitely invested in a few of them.

Given our experience in credit analysis, we’re keen on identifying the key characteristics used to ascertain mREITs’ relative value and safety.

Part of that analysis focuses on the quality and durability of those earnings. As I explained in yet another article,

“The vast majority are structured as floating rate loans offering good protection against rising interest rates. There is no inherent inflation protection, however, in the sense that inflation without rising rates won’t increase their income.

As counterintuitive as that combination may sound, that’s exactly what’s happened in the U.S. and many European economies over the past 18 months.

Equity REITs have undoubtedly seen appreciation of their assets on average, and in many cases much higher rents, while mREITs wait patiently for higher interest rates to move LIBOR and boost their income.”

iREIT on Alpha

Historical default rates for commercial mortgage loans are highly cyclical and comparable to high yield bonds over a full economic cycle, but inferior to preferred stocks and BDCs.

Overall, we consider quality mREITs attractive to high yield bonds and preferred stocks, marginally inferior to quality BDCs, and slightly undervalued against the sector’s historical averages.

We recommend actively managed exposure to this category as quality varies wildly within the asset class, but reasonably good passive options do exist. Overall risk for this category is medium based on sector average loan-to-values below 70%, approximately average default rates compared to other high yield categories, and moderate interest rate sensitivity.

The commercial mortgage REIT sector can be further broken down into two categories: pure balance sheet lender and balance sheet/conduit lender.

A pure balance sheet lender originates or purchases loans for their own balance sheet and holds these loans on their balance sheet (although they may sell participation units in the loans to diversify some of the risks). Examples include Blackstone Mortgage Trust (BXMT) and Apollo Commercial Real Estate Finance (ARI).

A balance sheet/conduit lender originates and/or purchases loans for its own account (balance sheet) or to be sold into a securitized vehicle such as CMBS (conduit). Ares Commercial Real Estate (ACRE), Ladder Capital (LADR), and Starwood Property Trust (STWD) are all conduit lenders.

There are differences between these two types as well, and risk can be further diversified. Balance sheet lenders originate loans with the intent of holding them on their books. Balance sheet/conduit lenders originate loans for both their own books and to sell into securitized markets such as CMBS.

The risk with balance sheet lenders is relatively straightforward – the risk that the loans don’t perform as expected. Balance sheet / conduit lenders have the risk of non-performance as well as the risk that the conduit market experiences a disruption and cannot take as many loans as expected.

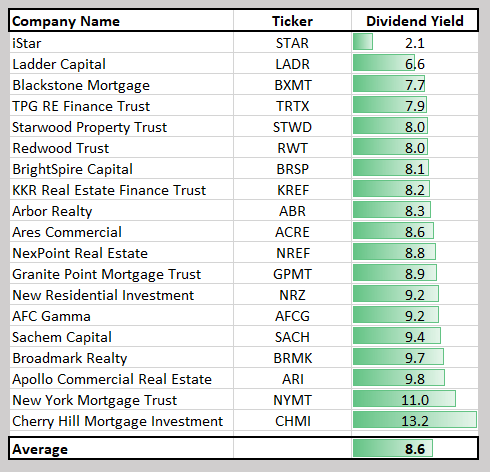

As you can see below, these commercial mortgage REITs generate dividend yields from 2.1% for iSTAR (STAR) to 13.2% for Cherry Hill Mortgage (CHMI). The average dividend yield for the sector is 8.6%.

iREIT on Alpha

Today I will provide you with a list of three commercial mREIT buys and our reasons for liking them. Recognizing that credit analysis is extremely important when analyzing mREITs, I must remind you to always think like a banker!

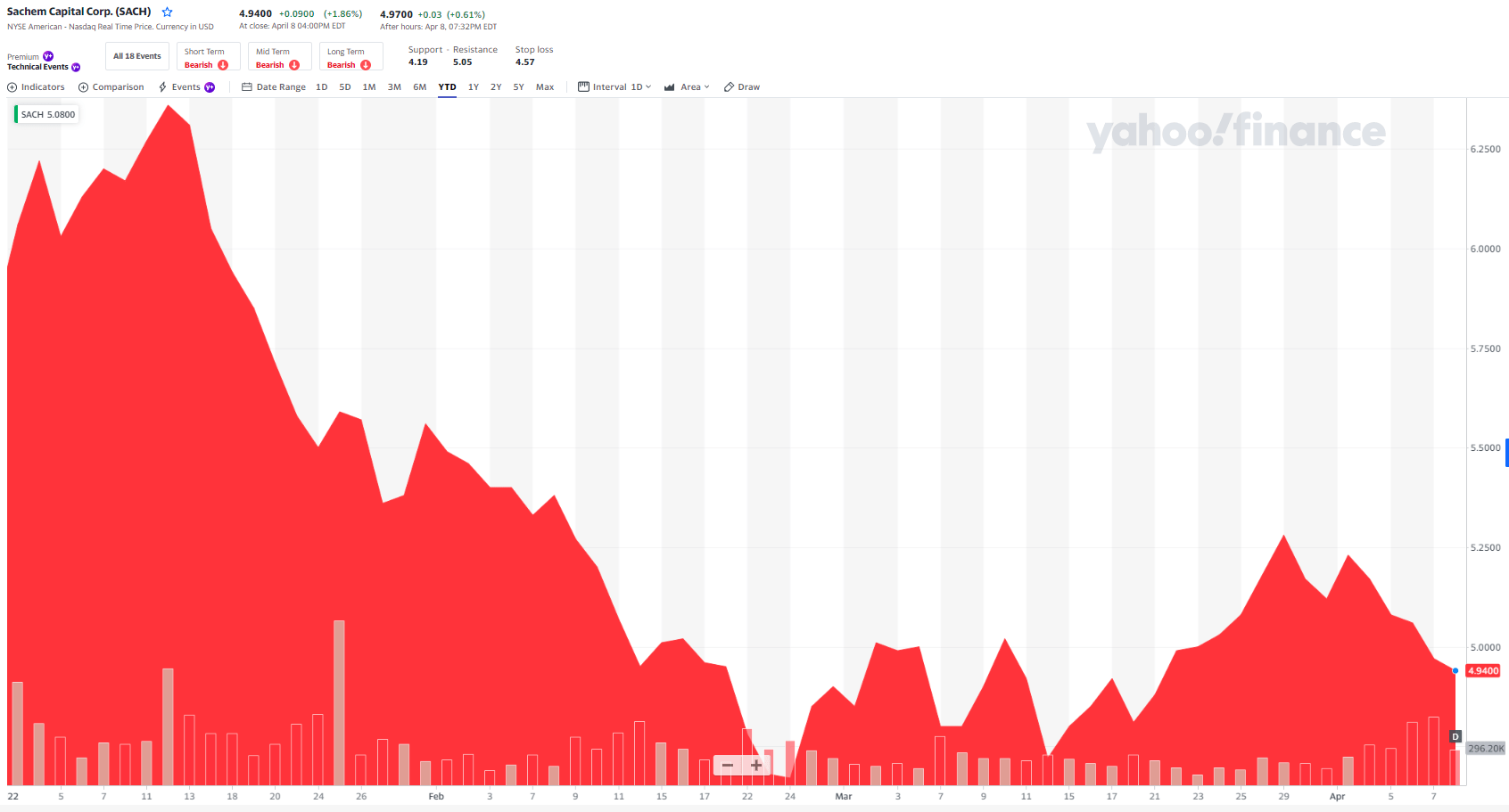

Sachem Capital Corp. (SACH): Dividend Yield is 9.7%

SACH is a new player to our coverage spectrum at iREIT, and this Connecticut-based mREIT specializes in originating short-term, high-yielding real estate loans, historically targeting the “fix-and-flip” and real estate development markets.

All loans secured by first lien mortgages with conservative maximum 70% loan-to-value ratio; all loans require personal guarantee by the principals of the borrowers. As viewed below, shares have fallen by ~15% YTD.

Yahoo Finance

The broader market backdrop continues to support growth for residential construction projects as demand continues to outpace available supply. A decade of under-development has led to aging housing stock in which the median house is ~40 years old.

One key differentiator for SACH is its nimble approach to origination. The company can close a loan in as quickly as 5 days, whereas the competitors can take 3-6+ months. Due diligence is more centered around the value of the collateral rather than the property cash flows or borrower’s credit.

SACH continues to diversify holdings, including larger loans with established developers, and it’s also expanding lending operations across the U.S. with a presence in 14 states, with a strong core focus along the Eastern seaboard.

Despite the rise in interest rates, SACH believes that there exists significant market opportunity for a well-capitalized “hard money” lender to originate attractively priced loans to small and mid-scale real estate developers with good collateral.

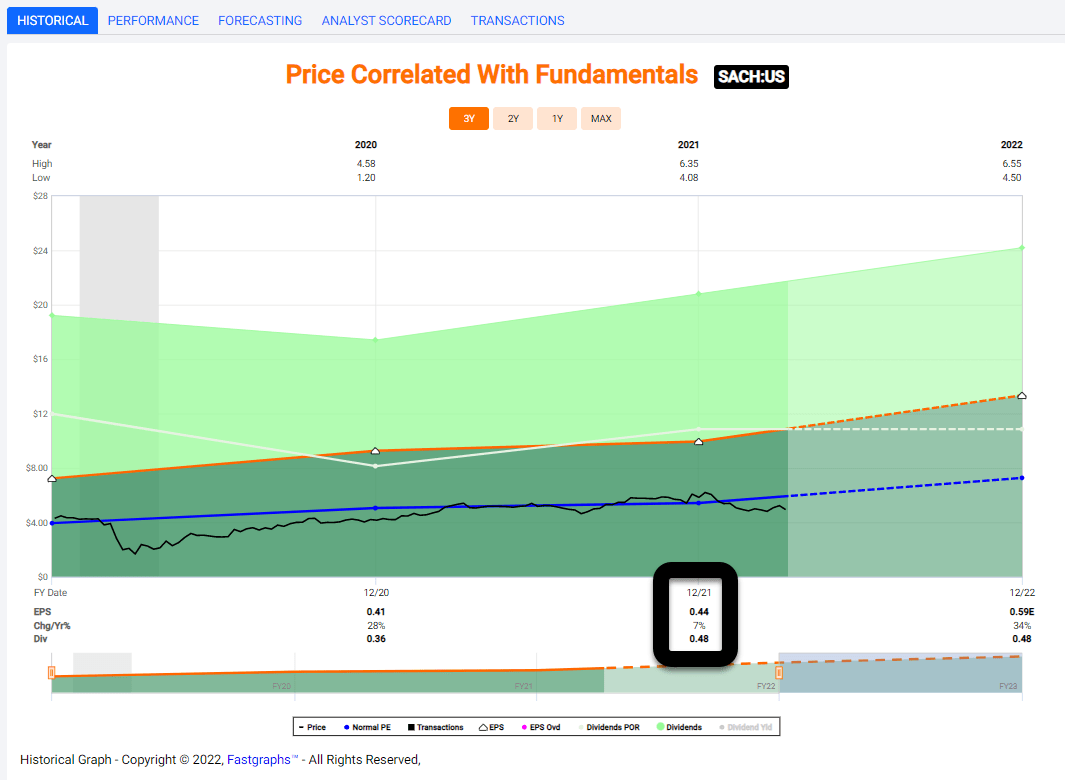

Total revenue in 2021 was approximately $30.4 million (compared to approximately $18.6 million in 2020), an increase of approximately $11.8 million, or 63.5%. The increase in revenue was due primarily to an increase in lending operations.

I asked the company’s CIO, Bill Haydon, last week about the increased expenses in 2021 (of $7.5 million), which represented 78%. He told me that the expenses should normalize in 2022.

Net income for 2021 was approximately $11.5 million (compared to approximately $9.0 million for 2020) an increase of approximately $2.5 million, or 27.5%. The net income per weighted average common share outstanding for 2021 was $0.44, compared to $0.41 for 2020.

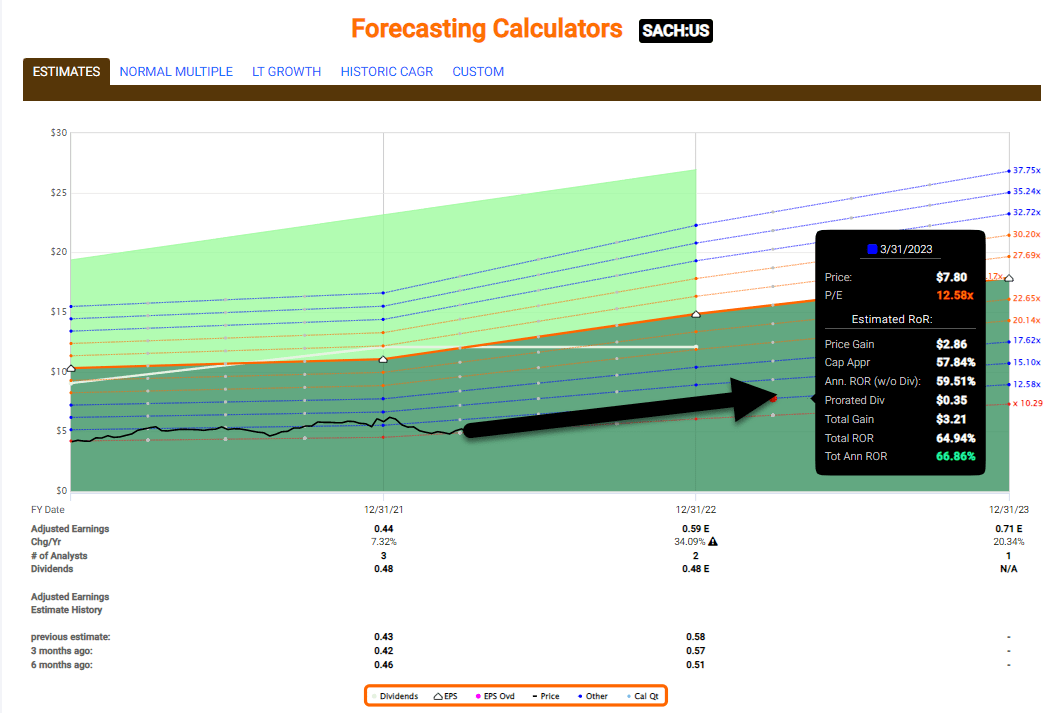

FAST Graphs

As viewed above, SACH’s payout ratio was 109% in 2021, which means the dividend was not covered; however, the analyst forecast for 2022 looks solid, with 34% growth (keep in mind, there are just 2 analysts reporting to Fast Graphs).

Nonetheless, given the pipeline and modest default rate (of around 1.6%) we believe SACH could easily cover the dividend and provide shareholders with a meaningful boost in 2022.

We maintain a Strong Buy, although we must also acknowledge this small cap REIT ($176 mm market cap) can be extremely volatile. Shares are now trading at $4.94 with a P/E of 10.3 and dividend yield of 9.7%.

FAST Graphs

KKR Real Estate Finance Trust Inc. (KREF): Dividend Yield is 8.5%

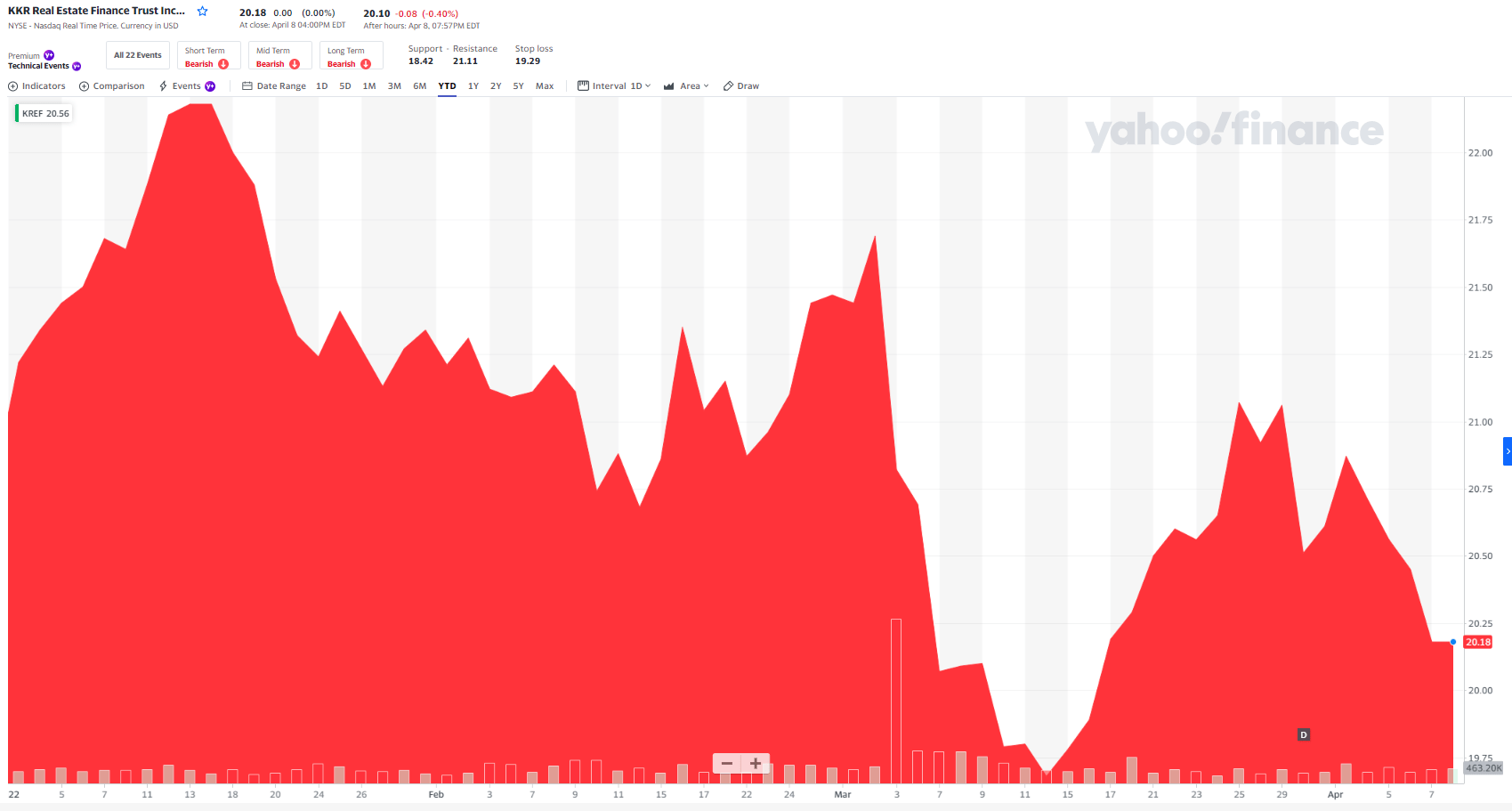

KREF is a commercial mREIT that has a purpose-built portfolio of senior-secured loans (99%) with a focus on the multifamily and office sectors (74%). Its $6.8 billion loan portfolio is positioned in the most liquid real estate markets, with an average loan size of around $131 million. 100% of loans are performing (as of Q4-21). As seen below, share have pulled back ~3.5% YTD.

Yahoo Finance

KREF is externally-managed by KKR (KKR), and we view this as positive given the strong alignment (KKR owns 23% of KREF) and deep experience of the private equity sponsor ($471 BB in AUM and 135 real estate professionals).

KREF differentiates itself by seeking opportunities where it has sourcing, underwriting, and execution advantages through KKR’s brand, industry knowledge, relationships, and deep bench of investment professionals.

KREF seeks to lend to the highest quality sponsors with properties located in the highest quality markets. As noted above, the average loan size is $131 million, and the portfolio has a modest 5% in construction loans. 89% of the portfolio is located within the Top 20 MSAs.

Over the last 12 months, KREF screened $145.9 billion of financing opportunities and originated $4.8 billion (3%) of senior loans. In the latest quarter the company collected 97.3% of interest payments due on loan portfolio and 100% on loans rated 4 or better.

The portfolio is well-positioned for rising rates, as 100% of the loan portfolio is indexed to one-month USD LIBOR. Around 54% of the portfolio is subject to a LIBOR floor of at least 0.25%, and 9% of total outstanding financing, including the Secured Term Loan, is subject to a LIBOR floor greater than 0.0%. Ongoing portfolio rotation out of higher rate-floor loans is positioning KREF to benefit from a rising rate environment.

KREF’ Q4-21 GAAP net income was $35.2 million, or $0.59 per share, and distributable earnings was negative $2.9 million (or negative $0.05 per share) due to $0.55 per share in realized losses on loan write-offs. In mid-January, the company paid a cash dividend of $0.43 per share.

In December, the company took title to its Portland retail property and has capitalized the property through a JV with a partner at Urban Renaissance Group, a full-service institutional real estate company with a local Portland presence. On the latest earnings call Patrick Mattson, President and COO said,

we’re seeing positive underlying trends with our remaining watch list loans, for example, on our New York luxury condo loan which had an initial loan balance of $240 million has now been paid down to $40 million through unit sales. Only six units remain to be sold, three of which are under contract.

In January, KREF raised approximately $155 million of gross proceeds through a follow-on issuance of its Series-A preferred shares at a fixed cost of 6.5%. This permanent capital helped support a funded portfolio of $6.8 billion.

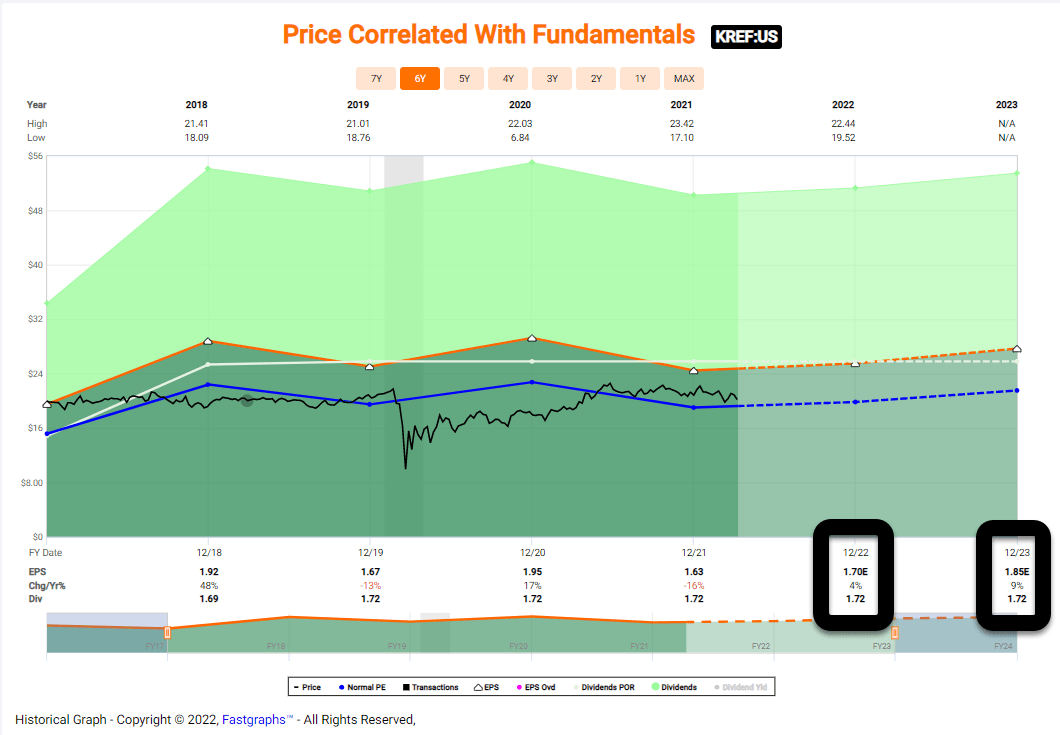

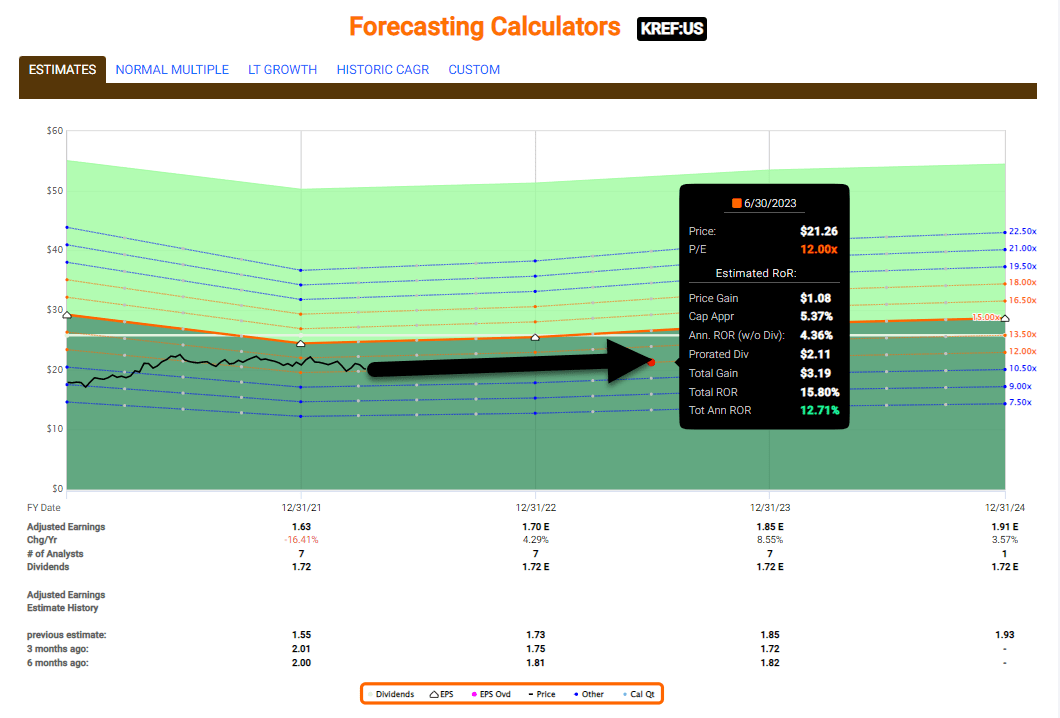

Fast Graphs

As seen above, KREF did not cover its dividend in 2021. However, analysts estimate growth of 4% in 2022 and 9% in 2023, which supports a continued dividend of $1.72 per share.

Shares are trading now at $20.18, or around 8% below our buy target price. The dividend yield is now 8.5%, and we’re forecasting shares to return around 15% over the next 12 months.

Fast Graphs

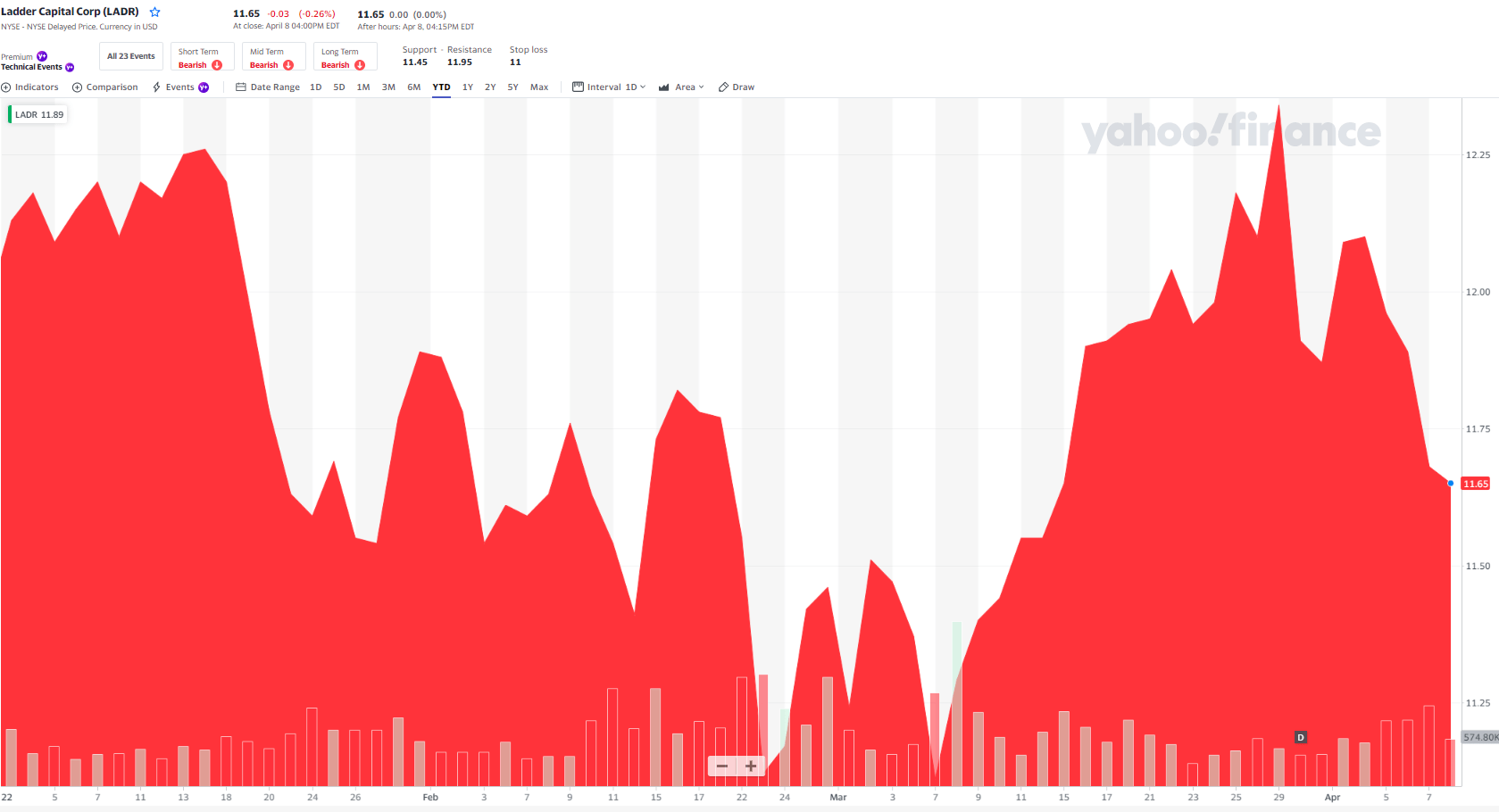

Ladder Capital Corp. (LADR): Dividend Yield is 6.9%

LADR is a commercial mREIT that was formed in 2008 and went public in 2014 (as a C-Corp). The company’s primary business strategy is to originate and securitize first mortgage loans on stabilized, income-producing commercial real estate properties. LADR is one of the largest non-bank contributors of loans to CMBS securitizations in the U.S. As seen below, shares are down ~2.8% YTD.

Yahoo Finance

LADR has a unique model in which the company does not rely exclusively on securitization for its revenue and has other diversified sources of revenue, including earning a significant portion of its revenue from first mortgage balance sheet loans and property rentals as well as expanding its market share in the commercial mortgage loan origination market.

LADR is internally managed, and its senior management team averages 27 years of industry experience and insiders (management and directors) own 11.4% of outstanding shares. This includes 7,303,000 shares owned by the CEO, Brian Harris, that puts his net worth in LADR at ~$85 million.

LADR’s fundamental business model is to loan against commercial real estate assets. The company has sufficient scale and expertise to approach all major real estate asset classes and geographies.

The company ended 2021 by having originated a total of $2.9 billion of loans, including a record 92 balance sheet loans, totaling $2.7 billion resulting in the highest annual production of Ladder’s balance sheet loans in Ladder’s history.

The growth in the portfolio led to strong earnings momentum over the course of the year, and the company continues to conduct rigorous credit standards and return expectations.

As of December 31, over 65% of the $3.5 billion balance sheet loan portfolio was comprised of post-COVID originated loans with fresh valuations and business plans. The composition of the portfolio remains consistent and continues to be primarily comprised of lightly transitional loans with a weighted average loan-to-value of 67%.

LADR’s $1.1 billion equity business is primarily made-up net lease assets, leased primarily to investment-grade tenants with necessity-based businesses under long-term leases. The portfolio contributed nicely to earnings during Q4-21 with $7.3 million of net gains, further illustrating the embedded value within the portfolio.

As of year-end 2021, the securities portfolio totaled $703 million, down from over $1 billion at the beginning of the year as the company reallocated capital into its balance sheet loan business, which it believes is currently offering the best risk-adjusted returns.

At the end of 2021, LADR’s total liquidity was over $800 million, and adjusted leverage was 1.5x net of cash. Around 39% of LADR’s total debt was comprised of unsecured bonds, and 83% of total debt was comprised of unsecured bonds and nonrecourse financing.

LADR appears to be well positioned to benefit from a potential rising interest rate environment, both by way of its large and growing portfolio of floating rate loans as well as its significant base of fixed rate liabilities. On the recent earnings call, CEO Brian Harris said,

…we have been waiting for this turn towards higher rates as inflation has taken on a more structural than transitory field in the last few months. By balancing our differentiated liability structure between a larger component of unsecured fixed rate corporate borrowings and a combination of floating rate CLO and a minor component of short-term repo debt, we have positioned Ladder to let the Fed do some of the work for us in the coming year.

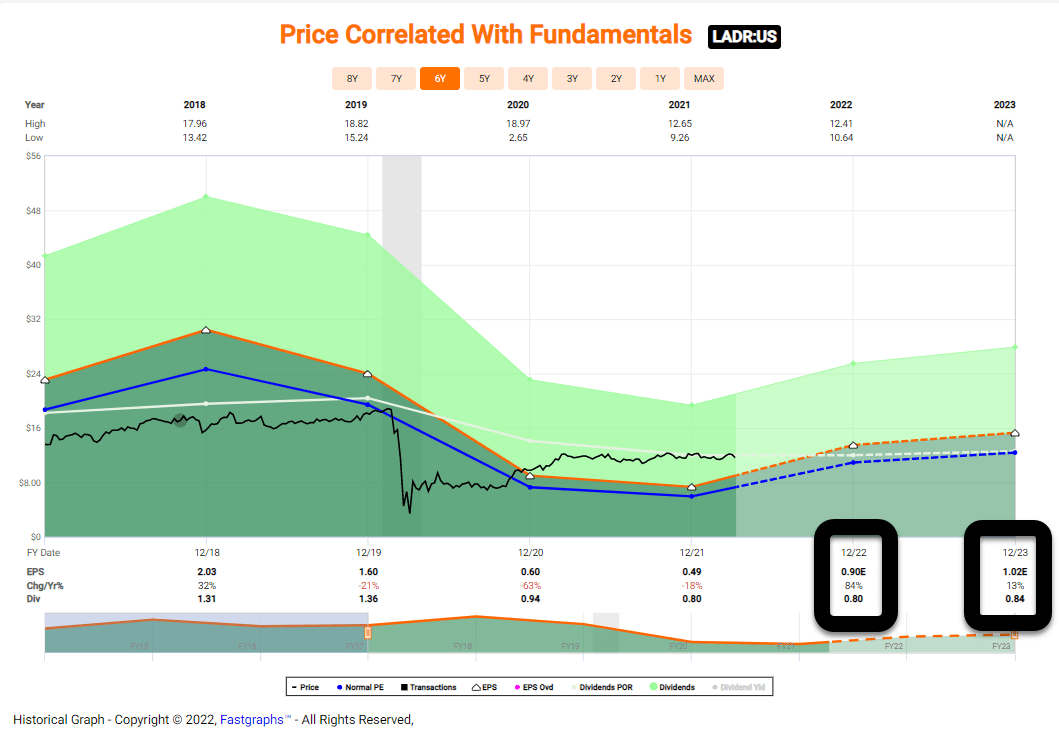

Fast Graphs

As viewed above, LADR did not cover its dividend in 2021. However, based on analyst expectations, the company should easily distribute $.90 per share in 2022, and we suspect dividend increases will also follow.

I credit the management team for creating ample liquidity in 2020 and taking the necessary steps to navigate the pandemic and put the risk of a dividend cut in the rear-view mirror.

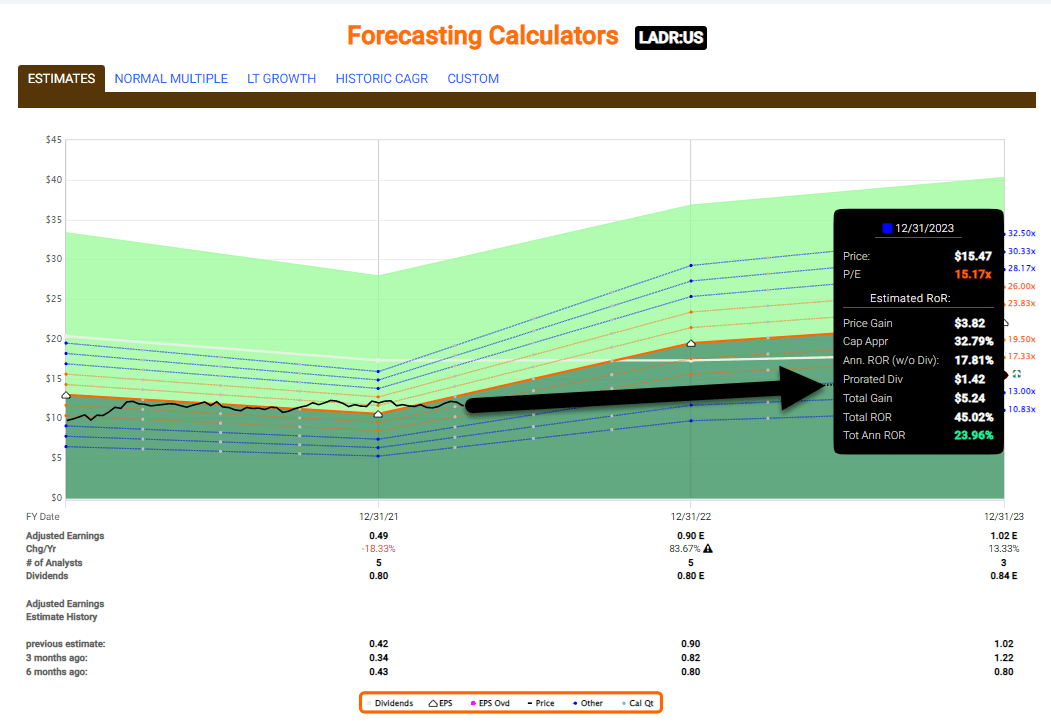

LADR shares are now trading at $14.10 per share and a dividend yield of 6.9%. With a large floating-rate balance sheet loan portfolio and predominantly fixed-rate liabilities, earnings are positively correlated to rising interest rates. We maintain a Buy rating.

Fast Graphs

In Closing…

Most investors own mREITs for yield only, but I’ve found that there are several other reasons to own shares:

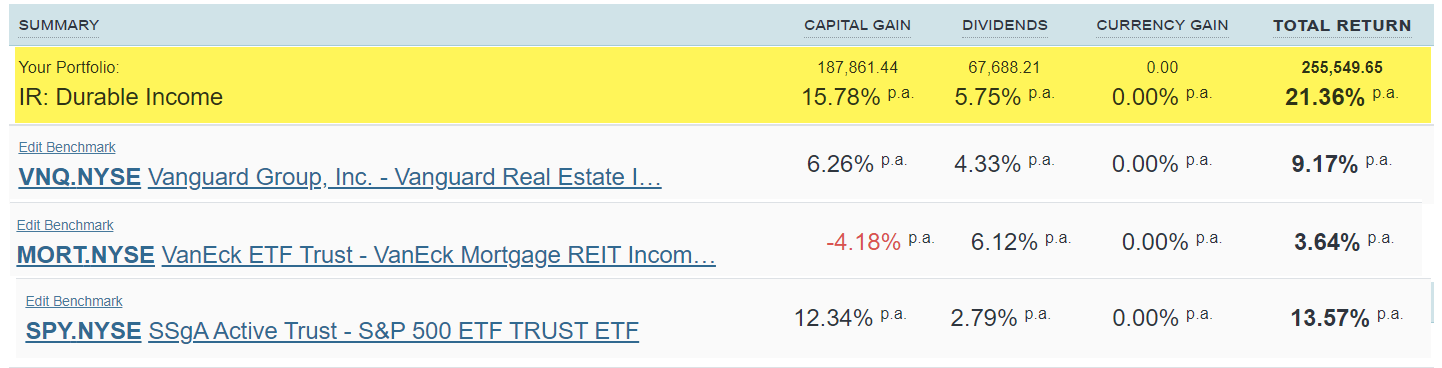

1. Appreciation: We have done extremely well owning shares in commercial mREITs, as evidenced by the returns we have generated by holding them since 2013: ~25% annual returns;

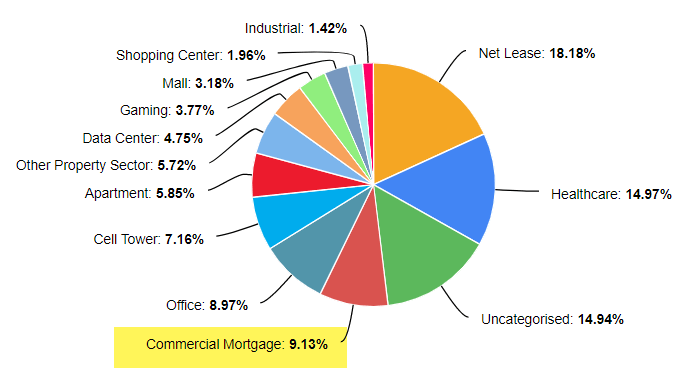

2. Diversification: We own around 9.1% exposure in commercial mREITs, and this provides the Durable Income Portfolio with attractive diversification attributes;

Sharesight

3. Equity REIT Insight: By carefully analyzing the commercial mREITs (and speaking with management teams), we have a competitive advantage that sets us apart from other analysts. We’re able to dig deeper into underlying credit risks that we would not be able to obtain if we did not cover these securities.

Of course, yield enhancement is the primary reason we own mREITs, and we have found that by selecting the best securities we can generate considerable alpha that others don’t.

Sharesight

But remember, if you look to own shares in mREITs, you must always remember to “think like a banker.”

Be the first to comment