da-kuk

“If you don’t know where you are going any road can take you there.” – The Cheshire Cat

Watching with interest the unfolding of the re-opening of China, leading to a continuous rally in basic metals and Chinese related stocks, in effect validating our early November calls in our post entitled “The Scarcity Principle“, when it came to selecting our title analogy we decided to go the Chinese Zodiac reference given 2023 will effectively be the year of the rabbit. Following a very eventful 2022 year of the Tiger, what could one expect from the year of the Rabbit given it is predicted to be a year of hope, largely because the rabbit is associated with peace, prosperity and longevity in Asia, one might ask. In Chinese culture, the rabbit is the luckiest of the 12 animals of the zodiac and symbolizes energy, elegance and beauty. Across Japan as well, the rabbit is a symbol of fortune, progress and savvy. Given how treacherous 2022 was and wishing you all, dear readers a happy new year, we are wondering if indeed in 2023 we would need to follow in similar fashion to Alice the “White Rabbit”, the one with a pocket watch and waistcoat lamenting that he is late down a rabbit hole. Some investors might indeed think they have been late to the Chinese re-opening party but we ramble again.

In this conversation, we would like to review what has been unfolding since our November Chinese hint as well what is currently playing out when it comes to our most recent calls and also some additional suggestion for the start of the year.

- The Chinese and Emerging Markets appeal and other calls

In a previous conversation we recommended the “Make Duration Great Again” (MDGA) investing on the long end of Investment Grade Credit from a carry and roll down perspective. We told you this trade would continue to be enticing in 2023:

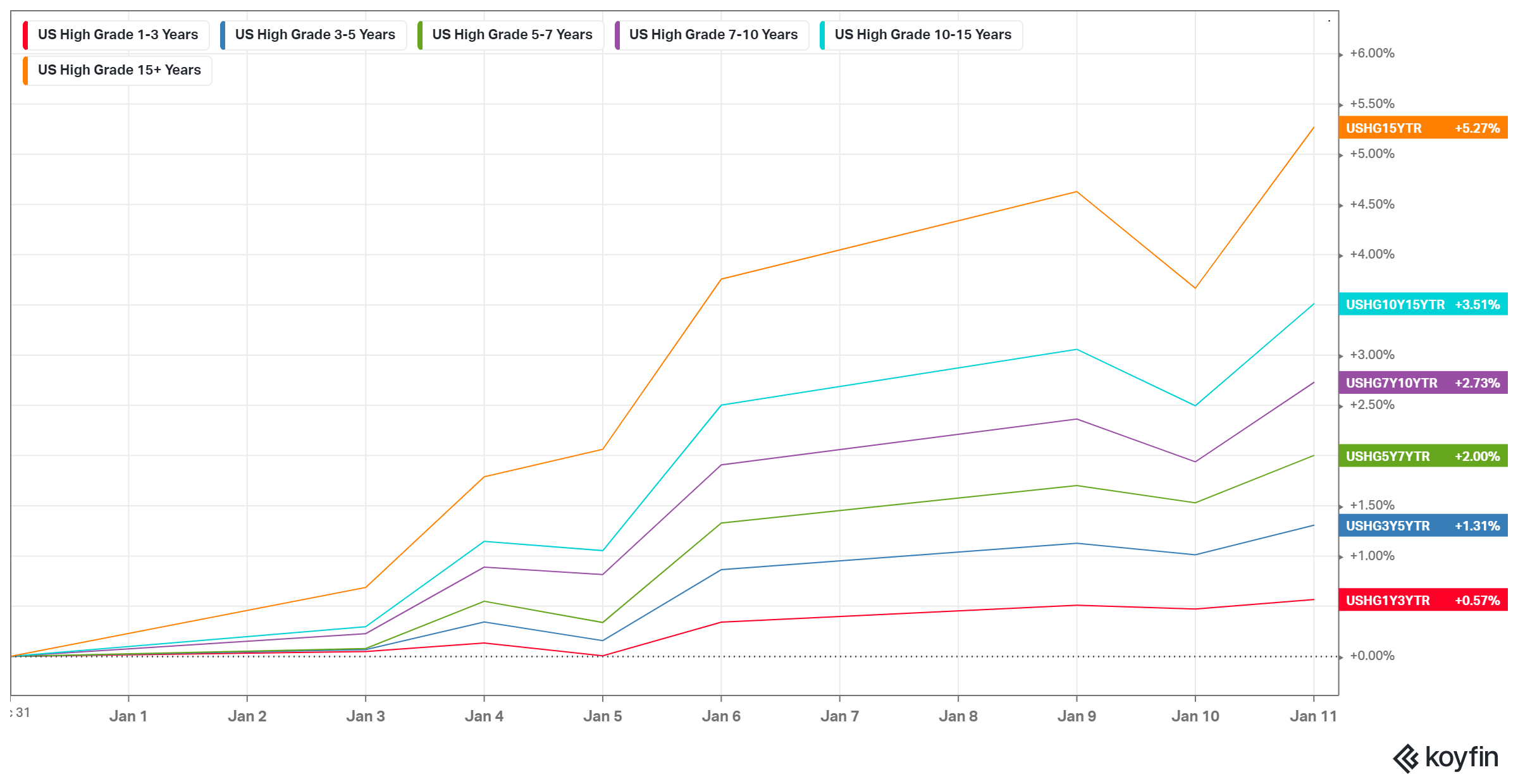

US IG YTD (Macronomics – KOYFIN)

US High Grade (Investment Grade) 15+ years has considerably “outperformed” and is already up 5.27% YTD.

We told you in our conversation from the 23rd of November the following:

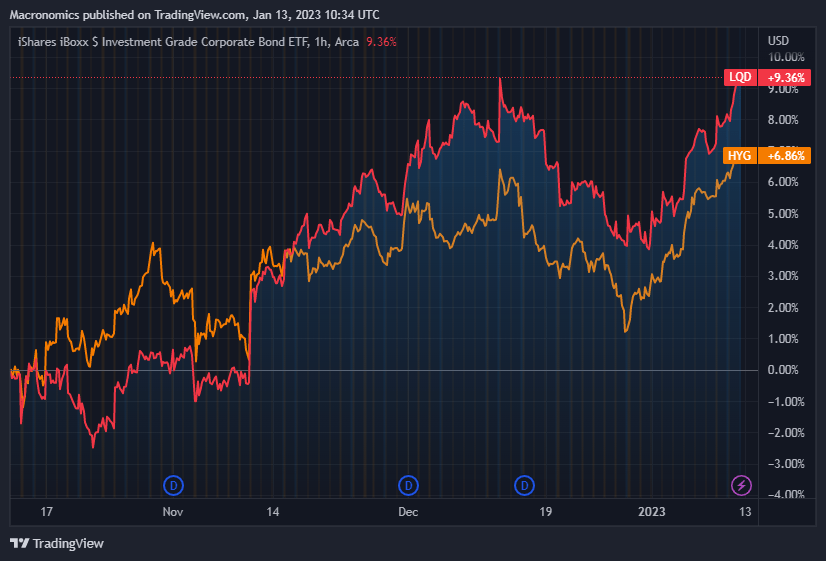

“There is indeed more room for “outperformance” of Investment Grade relative to High Yield when ones look at the two most liquid ETFs LQD for US Investment Grade and HYG for US High Yield” – Macronomics, 23rd of November

We continue to expect an outperformance of US Investment Grade (LQD) relative to US High Yield (HYG) in 2023 as per below chart for the last 3 months:

LQD VS HYG (Macronomics – TradingView)

YTD we have seen a rally in high beta credit but overall LQD and HYG are in a tight range performance wise. The path of the Fed’s hiking path will determine the outcome for duration exposed assets but given the 2022 onslaught and as was discussed on this very blog, US Investment Grade credit has regained some of its appeal.

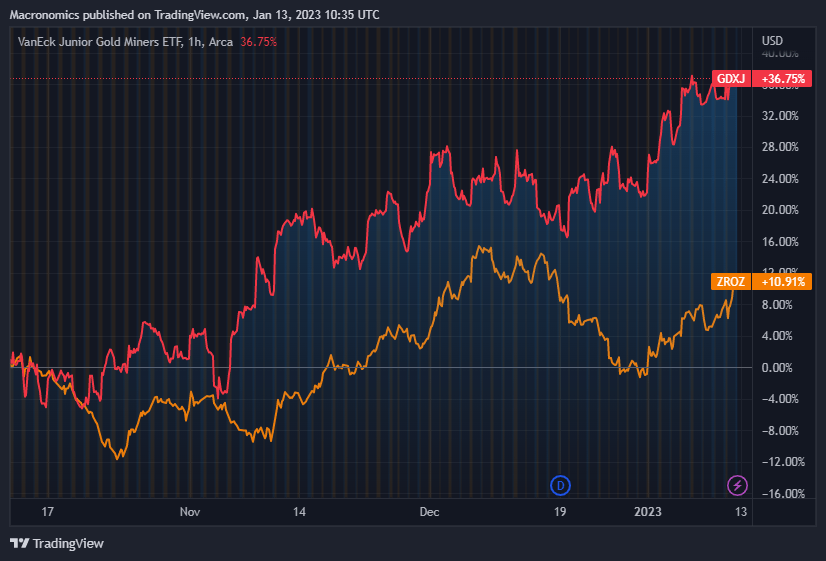

We previously recommended the “Make Duration Great Again” (MDGA) trade via ETF ZROZ (PIMCO 25+ Year Zero Coupon US Treasury Index ETF) which is extremely sensitive to rates move in conjunction with buying Junior Gold miners through ETF GDXJ. Both trades are highly sensitive and convex (Early November until today chart below):

GDXJ VS ZROZ (Macronomics – TradingView)

This “put-call parity” strategy continues to play out in 2023 with falling yields with a change in the Fed’s narrative, and rising gold prices:

GDXJ VS ZROZ (REFINITIV EIKON)

Sure it is early stage to fathom the performance of this “PCP” strategy in 2023, but we remain convinced there is much more to it in 2023.

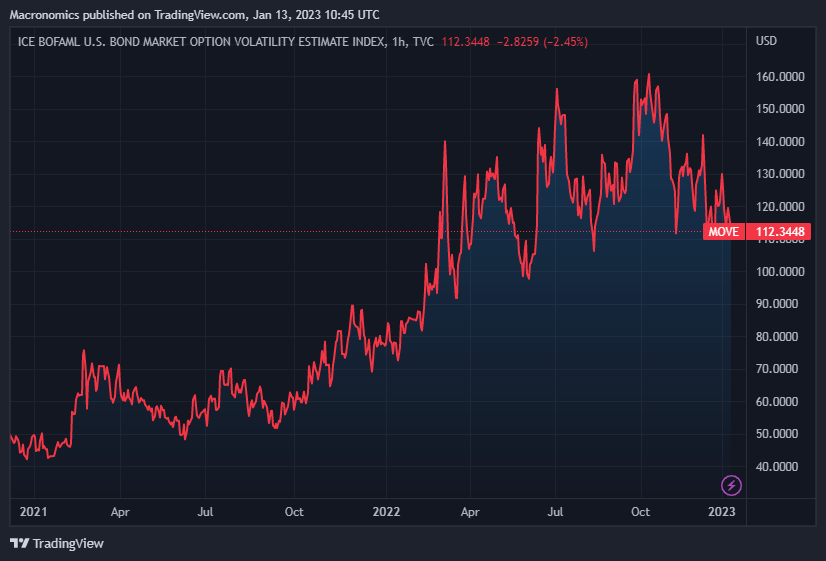

As we indicated in previous conversations the rally in credit markets is depending entirely on bond volatility receding as per below 1 year MOVE index:

MOVE INDEX (Macronomics – TradingView)

As long as bond volatility is receding, credit markets can continue to perform in this environment. The main culprit of the vicious repricing in 2022 was the rise in “real yields” aka our fondly named “Mack The Knife” (US dollar + Real yields) which went on a murderous rampage.

Since the beginning of the year, credit risk (CDS spreads) has been steadily falling, pointing towards a “risk-on” environment hence the rally in “high beta”.

CDS spreads (Macronomics – Datagrapple.com)

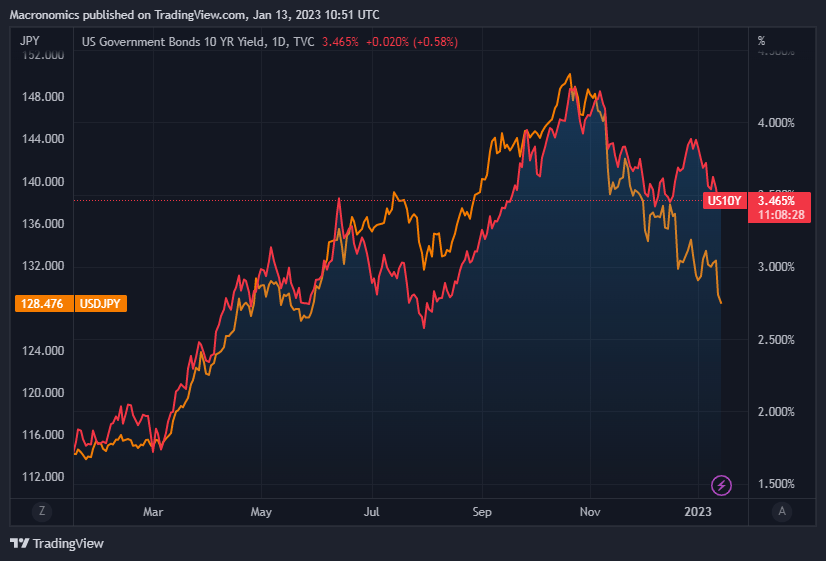

Both the US 10 years yield and the USD/JPY have moved in lockstep during the course of 2022 and as we expected we have seen the Japanese yen strengthen as per our previous conversation:

US 10 Years yield vs USD/JPY (Macronomics – TradingView)

So far in 2023 our call for a stronger yen is being vindicated.

In our conversation “The Scarcity Principle” we argued that a full re-opening of China could bring in more inflationary pressure in the commodities space in that context. No wonder copper is up 9.1% YTD:

Commodities YTD (Macronomics – KOYFIN)

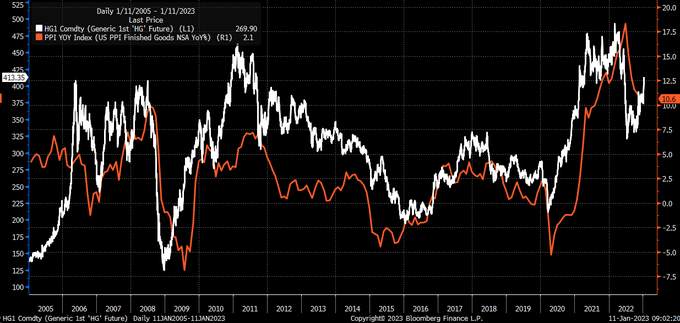

For copper, what has been interesting as pointed out by Michael J. Kramer in our Twitter feed has been the relationship with PPI and copper prices:

Copper VS PPI (Bloomberg – Twitter)

If deglobalization is the “trade du jour”, then it makes sense that copper prices are rising on not only China re-opening but as well on low inventories and tight markets. We are indeed moving towards a “scarcity” environment and, as such, many countries are taking restrictive measures when it comes to their commodities export markets. For instance, President Widodo of Indonesia has banned exports of bauxite starting in June. Indonesia has in the past threatened or imposed partial or full blocks on palm oil, coal and nickel. Indonesia has the fifth‐biggest reserve of bauxite in the world. In India, local wheat prices have soared 27% since the country introduced a wheat export ban. The latest UN FAO World Food Price index is down 1.9% MoM in December, the 9th consecutive monthly decline. Down 1.0% YoY, first YoY decline since mid-2020. Still up 45% from May 2020 trough.

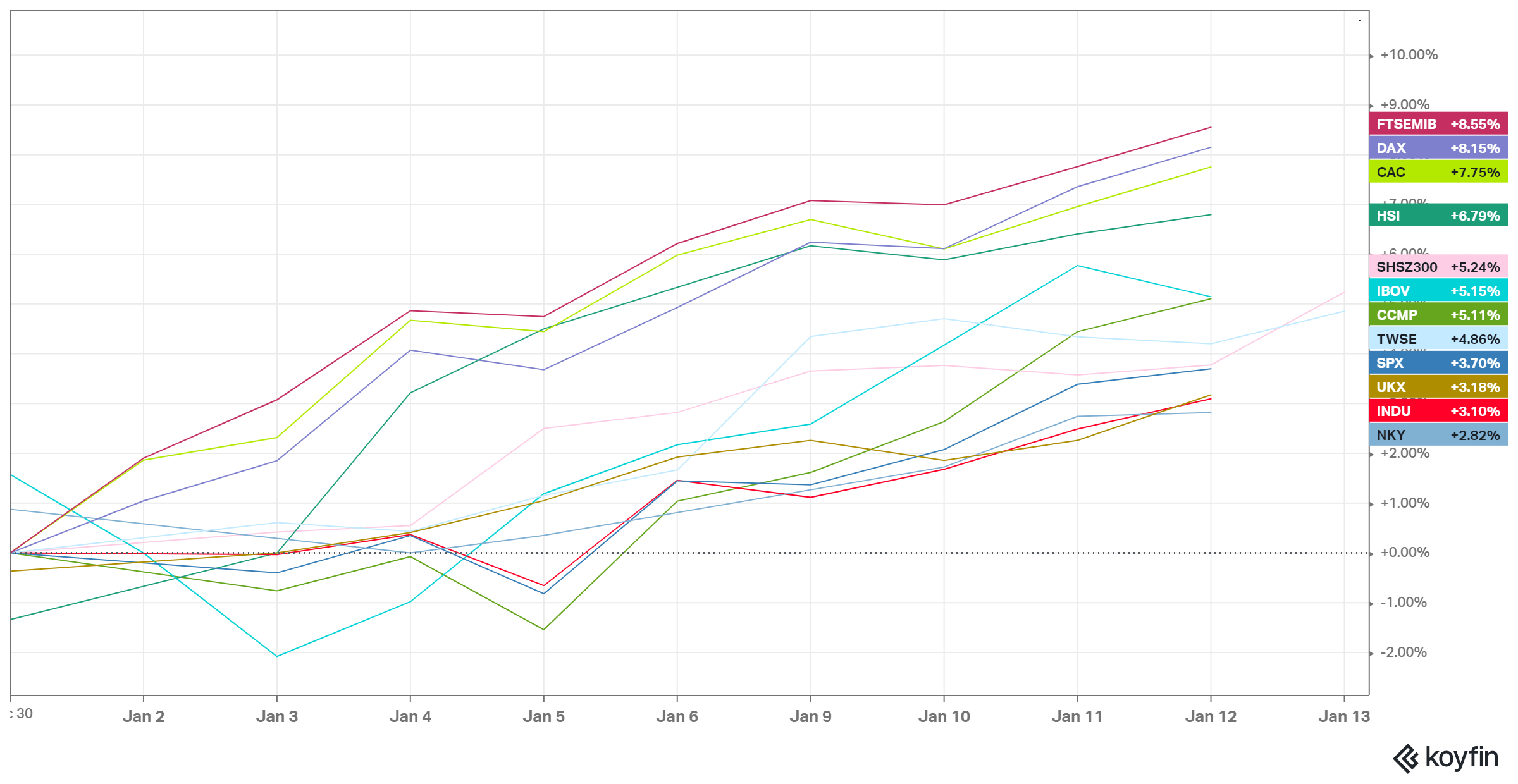

On the equities side, what has been surprising to us is how European markets have rallied strongly since the beginning of the year:

World indices (Macronomics – KOYFIN)

In reality we should not have been surprised at least from a French index CAC 40 perspective given the luxury sector represents more than a third of the weight of the CAC 40 (LVMH + L’Oréal + Hermès + Kering). The weight of the luxury sector in the French sector has tripled since 2007. The CAC 40 is not a true reflection of the French economy as such given some sectors such as the luxury sector are over-represented. In the US, the Tech sector as well is over-represented in some indices.

Whereas the rest of the world is enjoying a strong bounce, US is lagging behind since the lows of October:

“US stocks have been laggards among global markets in the rebound from respective Oct lows. Asian, European and emerging-market peers have all surged into bull market territory in dollar terms, rising more than 20%, while the S&P 500 is up about 9% and the Nasdaq gained just 3.3%.” – Jeffrey Kleintop

US Equities lag (Bloomberg – Twitter)

Maybe the Year of the Rabbit will clearly see Asia taking the lead on the US and the rest of the world in terms of performance?

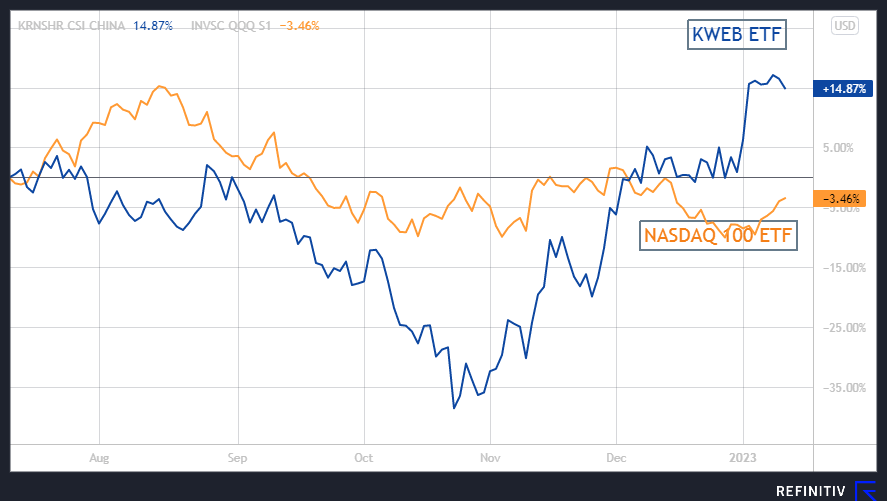

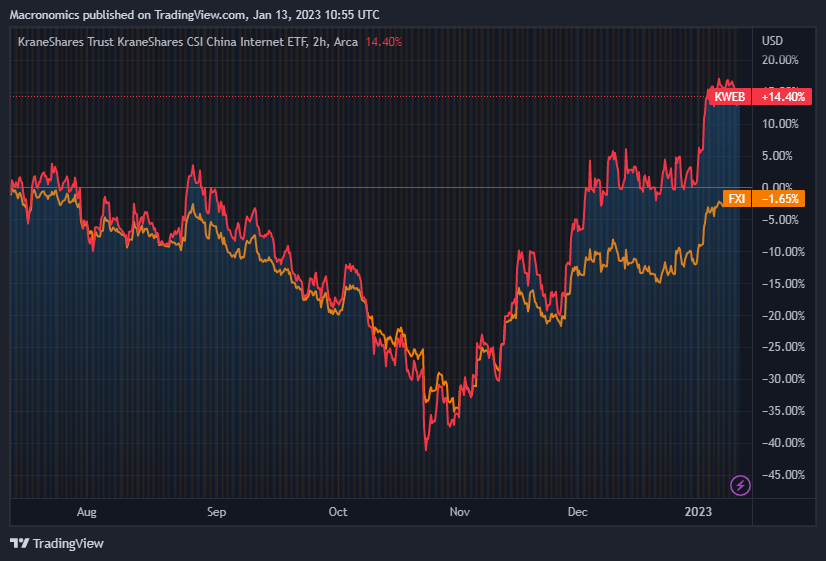

Chinese Tech ETF KWEB’s performance for the last 6 months versus NASDAQ 100 ETF:

KWEB VS NASDAQ (Macronomics – KOYFIN)

One thing for sure when it comes to Chinese shares, Chinese TECH is outperforming China large caps (h/t Brian Yates) in the last 6 months:

KWEB VS FXI (Macronomics – TradingView)

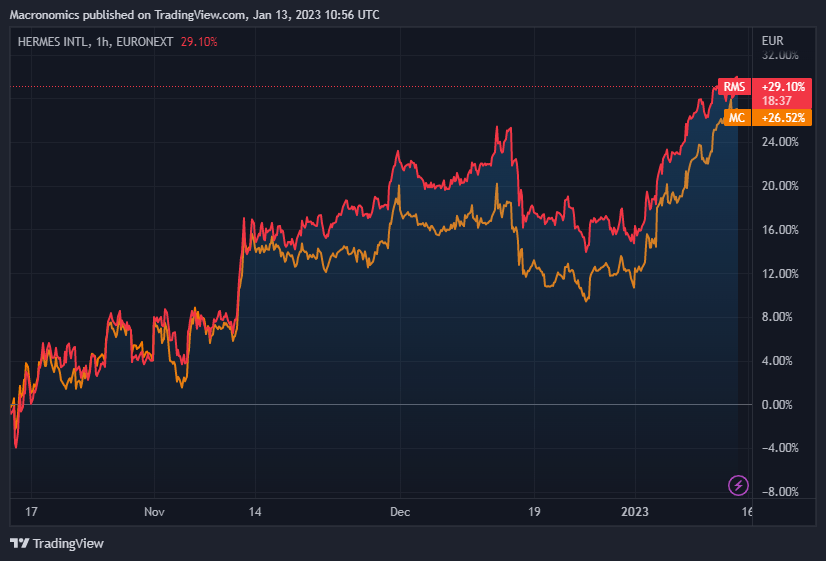

Another pointer of the Chinese “re-opening” play has been in the luxury space as seen in the below chart of LVMH share price vs Hermès in the last 3 months:

Hermes vs LVMH (Macronomics – TradingView)

We continue to view positively the luxury sector and in particular Hermès over LVMH on strong Asian demands. If indeed the Year of the Rabbit should be somewhat less agitated than 2022, then luxury stocks should continue to rise with Asian peace, prosperity and longevity. As such Asian demand exposed assets should clearly benefit in continuation with the energy sector and basic metals.

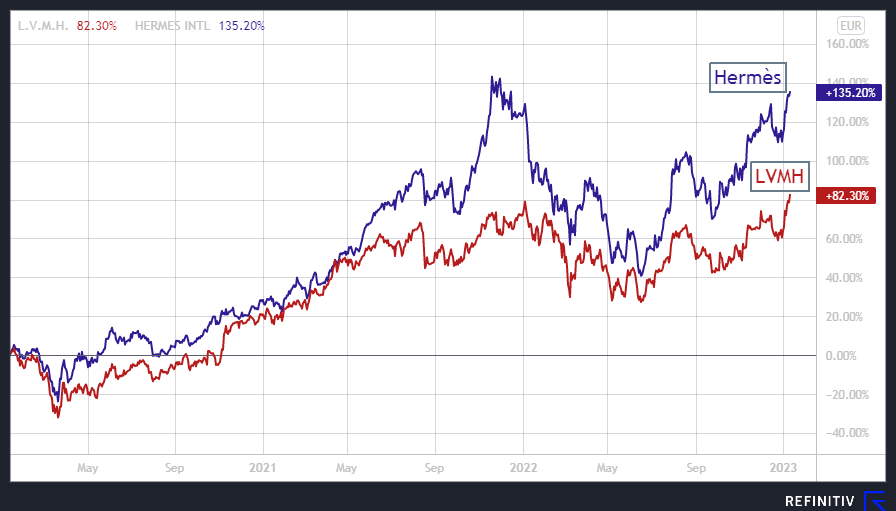

On the luxury side, our preference goes for Hermès as per the below 3 years chart:

Hermes vs LVMH (Macronomics – Refinitiv Eikon)

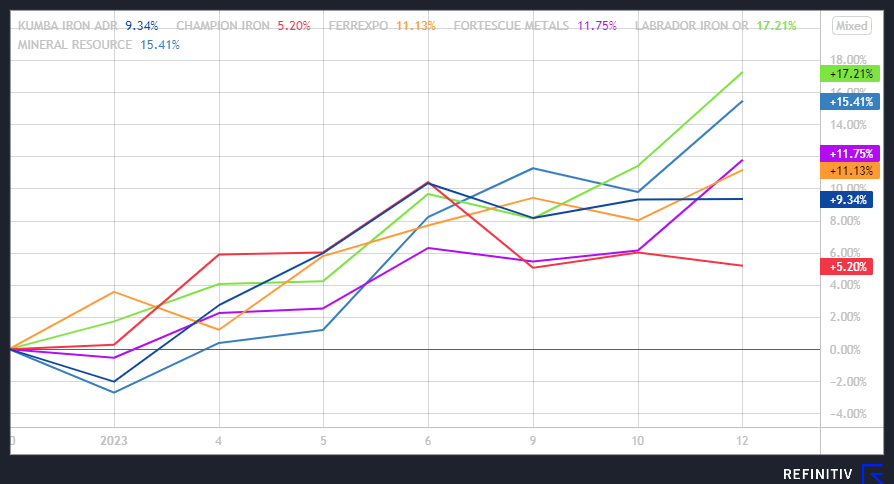

Also, Iron Ore large caps could benefit from the Chinese “surprise” and YTD the performance is already decent:

Iron Ore large caps YTD (Macronomics – Refinitiv Eikon)

For the last 6 months some large caps Iron Ore players have seen a significant surge:

Iron Ore large caps 6 months (Macronomics – Refinitiv Eikon)

Diversified Miners should as well continue to benefit from the Year of the Rabbit (disclosure we are long VALE SA):

Diversified Miners (Macronomics – Refinitiv Eikon)

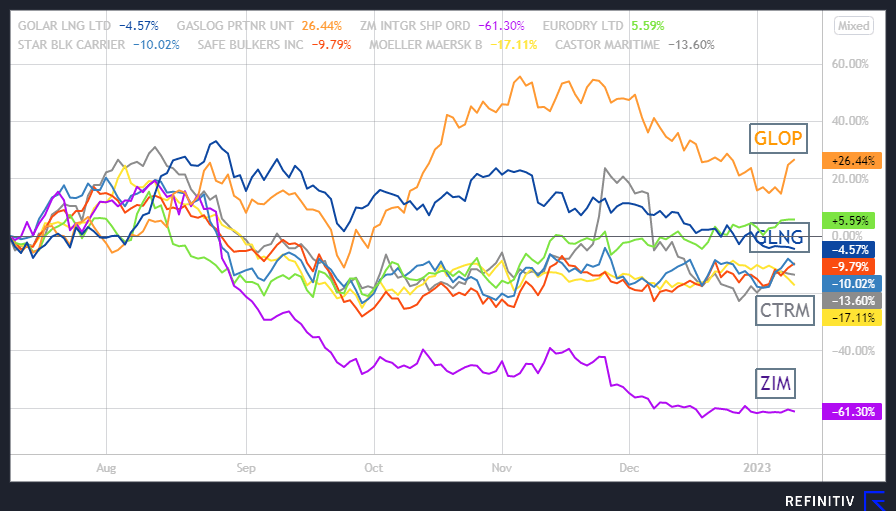

Shipping and LNG exposed stocks wise, 2022 has been very challenging to say the least during the year of the Tiger:

Shipping and LNG exposed stocks (Macronomics – Refinitiv – Eikon)

Given our appetite for neglected / out of love stocks, ZIM is starting to us to look enticing from a “value” perspective and potential “convex” returns in 2023 but then again it might be early days. Worth taking a punt? Maybe.

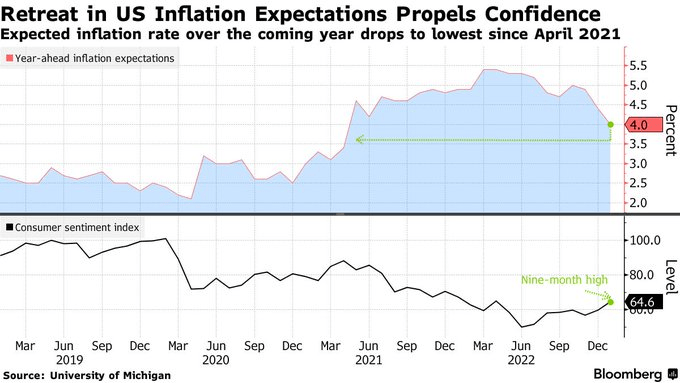

Looking at the latest print of US CPI coming in line with expectations at 6.5%, no wonder risk assets have seen a return of “goldilocks”. As such, both gold and US 10 years Treasury Notes have risen in sympathy. But, when it comes to the US CPI, the devil, as always is in the details. As such Owner’s Equivalent Rent hides in plain view the increase in house prices since it measures the “financing cost” of buying a house rather than the “capital cost”.

When interest rates rise; even as prices fall OER goes up. This is not a trivial issue we think because end of the day OER is 24.2% of the entire CPI index. As such, US prices for basic necessities such as food and shelter are showing continued upward pressure which doesn’t necessarily bodes well for the US Consumers down the line as witnessed by the rapid surge in credit card usage in the US and US commercial bank interest rates on credit card plans at around 19%, the highest in 40 years.

Retreat in US inflation (Bloomberg – Twitter)

With inflation still high, as a reminder, “Bracket creep” is the process by which inflation pushes wages and salaries into higher tax brackets, leading to a fiscal drag situation for those who remember our post from January 2018:

“Most progressive tax systems are not adjusted for inflation, as wages and salaries rise in nominal terms under the influence of inflation they become more highly taxed, even though in real terms the value of the wages and salaries has not increased at all. The net effect overall is that in real terms taxes rise unless the tax rates or brackets are adjusted to compensate. That simple.” – source Macronomics, January 2018

As well, US savings rates continue to fall. How long can the borrowing fueled consumption last is the big question for 2023 we think. In that matter a rapid US CPI decline is essential to reduce pressure on the US consumers.

“By three methods we may learn wisdom: First, by reflection, which is noblest; Second, by imitation, which is easiest; and third by experience, which is the bitterest.” – Confucius

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment