The U.S. stock market is surging once again

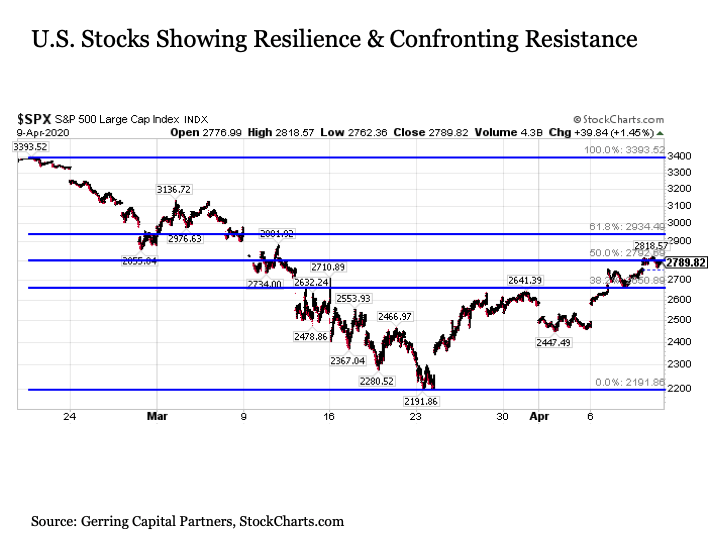

It was an extraordinary week for U.S. stocks. After showing signs of exhaustion last week, the S&P 500 Index surged by +7% on Monday, then added another five percentage points to its gains through the remainder of the holiday shortened week. With U.S. stocks having now rebounded by more than +27% over the past thirteen trading days since the March 23 lows, many investors are now understandably wondering if the worst is now behind us.

Impressive resilience

Let’s begin by taking a look at where we are today with the U.S. stock market. The S&P 500 Index has now retraced 50% of its -35% decline from February 19 to March 23. It is still -18% below its February highs. And this 50% retracement places it right against its latest resistance level at 2,792.69. It is worth noting that both relative strength and momentum are currently in favor of the S&P 500 Index advancing above this resistance in the short term, particularly given that stocks spent much of the trading day on Thursday above this key level.

{kind=link}

Challenges ahead

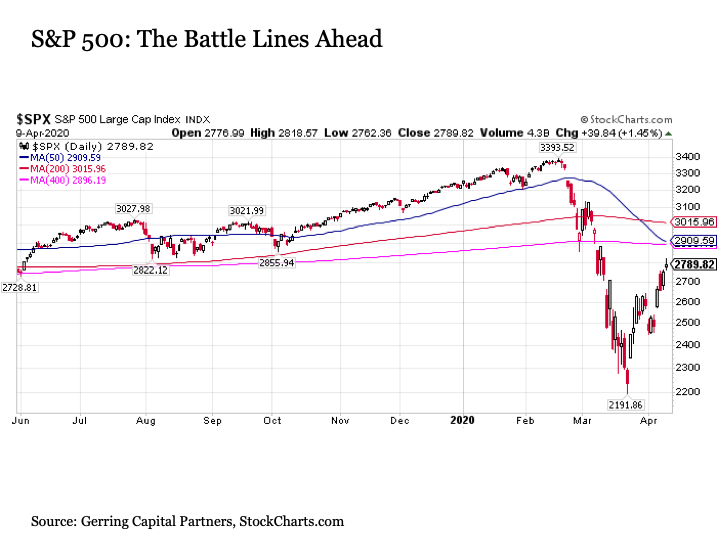

Instead, the more significant resistance to the current rebound on the S&P 500 Index lies ahead. This includes three key levels – the 50-day moving average currently at 2,909 and falling, the 200-day moving average 3,015 and falling, and the 400-day moving average at 2,896 and falling. It is how U.S. stocks respond in the coming weeks if and when the S&P 500 Index reaches these key resistance levels that will determine whether the worst is now behind us or the worst is yet to come.

The significance of resistance

Why exactly should we care to monitor these resistance levels? Because they have shown themselves to be highly significant early warning signals in the past of what was yet to come.

2007-2008

In late 2007, the U.S. stock market fell into correction. After peaking on October 9, 2007, the S&P 500 fell by -20% through mid-January 2008. It subsequently rallied by +10% through February 2008. But the moment it reached its downward sloping 50-day moving average, it fell sharply back as Bear Stearns began its final descent toward its March 2008 collapse. Once the Fed bailout of Bear Stearns was resolved in mid-March, the stock market appeared to bottom and the rally was on, as it appeared that the worst was now behind investors at the time. The S&P 500 Index subsequently rebounded by +15% through mid-May 2008. But once it hit its downward sloping 200-day moving average that included an intraday lurch to its 400-day moving average, the game was officially over for U.S. stocks, as we all know what unfolded from there through March 2009. It is worth noting that the May 2008 peak and subsequent failure also occurred at the 50% Fibonacci retracement of the S&P 500 Index from its October 2007 highs to its March 2008 lows.

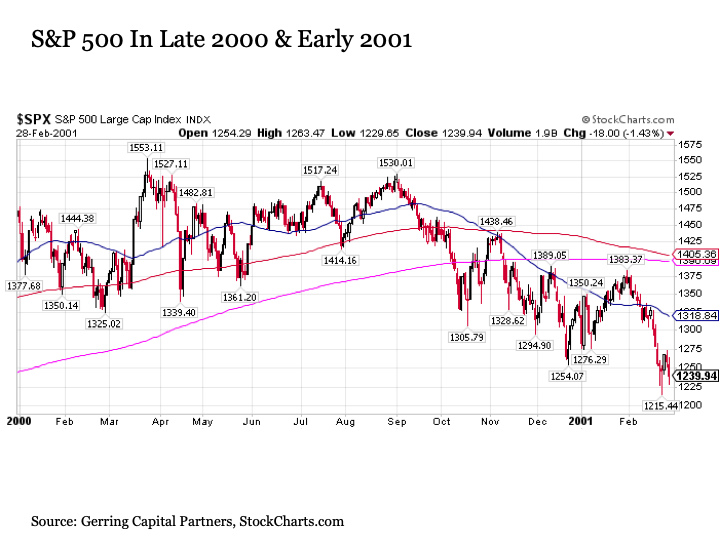

2000-2001

Let’s go further back to 2000 for another example of the importance of monitoring these key resistance levels. Although the history books note March 2000 as the tech bubble peak, it wasn’t until September 2000 before the U.S. stock market truly started to break. From early September to mid-October, the S&P 500 Index fell by -15% before subsequently rallying. Stocks subsequently rallied by +10% through early November before getting turned back at its 50-day and 200-day moving averages. The S&P 500 Index went on to fail twice more at its increasingly downward sloping 50-day moving average in early December 2000 and early January 2001 before finally clearing this hurdle in mid-January, only to ultimately fail at its 400-day moving average.

So when seeking to determine whether we are destined to descend further into a bear market in the coming months or if U.S. stocks are poised to put this staggering one month correction quickly behind us, it is highly instructive to closely watch how stocks respond to these key moving average resistance levels in the coming months.

If stocks fail at these levels, it would signal that the worst is still yet to come for U.S. stocks, just as it was in early 2001, early 2008, and also in June 2010, August 2011, December 2016, and November 2018 during some of the more notable post crisis corrections.

Conversely, if stocks slice through these resistance levels as they did in spring 2003, summer/fall 2009, as well as September 2010, January 2012, March 2016 and early 2019 during the post crisis period, this would signal that the worst is now behind us.

At a minimum, investors should be carefully consider dialing back at least a portion of their risk profile upon any arrival at these key resistance levels. This is particularly true for those that may have been overweight stocks and higher risk securities heading into this crisis. For if the market falls back to the downside, you will have protected principal. And if stocks definitively breakout to the upside, the opportunity always exists to reinvest.

What about the fundamentals?

This is where things get murky. The underlying fundamentals for the market are unequivocally poor. Global economic growth has effectively ground to a halt, unemployment is skyrocketing, corporate earnings are set to evaporate at a time when stocks are still heavily overvalued on a historical earnings basis even after the recent market correction, and the forward outlook is about as uncertain as it could possibly be with not only vast economic but also health and societal unknowns given where we are today.

Frankly, the recent stock market bounce since March 23 defies all fundamental logic. It is not surprising, however, as stocks have historically always bounced strongly following sharp declines even in the worst of bear markets. But the bounce is not fundamentally driven in any meaningful way.

Now some counter this fundamental conclusion by proclaiming that the U.S. stock market is a predictive mechanism that is anticipating the state of the economy nine months in advance. There was a time when I would have agreed with this statement, but it is deeply misguided in my view today. Why? As one example, if the U.S. stock market was such a great predictive mechanism, why wasn’t it descending lower nine months ago instead of folding like a house of cards starting in early February? And if the U.S. stock market was such a reliable predictive mechanism, why did it repeatedly overestimate the strength of economic growth year after year after year after year during the post crisis period?

Instead, the primary predictive purpose that the U.S. stock market serves today in my view is whether the U.S. Federal Reserve will be successful or not in providing sufficient monetary policy support to keep the artificially inflated post crisis stock market going for a few more rounds.

This leads us to some important points for investors to consider as we proceed forward into this new unknown in the coming weeks and months.

Know what fuels the bull

If you are an investor, you simply cannot kid yourself. The stock market has rallied so sharply since March 23 thanks to the actions of the U.S. Federal Reserve. If the Fed did not intervene with extraordinary policy actions, many of which that would have been entirely unthinkable just two months ago, the U.S. stock market along with its many other highly correlated risk assets would almost certainly have continued to plunge steadily and sharply lower. So if you are bullish, it is important to resist the urge to think that any further gains in stock prices in the near-term is based even remotely on fundamentals. Maybe they eventually will be, but they certainly are not now and they will not be for the foreseeable future, as we simply have no idea yet what these fundamentals are actually going to look like in the coming months.

Your savior is also your scourge

The Fed is stopping at nothing to save the economy and its financial markets. What they are deploying in 2020 is exponential orders of magnitude greater than what they deployed during the financial crisis in 2008, which was exponential orders of magnitude greater than the standard interest rate cuts deployed during the bursting of the tech bubble. Remember the Fed’s rescue of Long Term Capital Management in 1998? It seems so quaint by comparison 22 years on. We have a trend here. Basically, the Fed seems to keep making things ultimately worse with each successive “rescue”.

With all of this in mind, it is reasonable to consider whether today’s predicament might have been more manageable if the Fed would have just backed off for a bit and stopped trying to micromanage the economy and markets. To this point, why exactly is it that the Fed had to intervene so aggressively and so quickly to rescue nearly everything across financial markets within just days of realizing that COVID-19 was going to turn into a major problem for the global economy? Because they have fostered a market environment for so many years that encouraged extreme valuations, unsustainably tight credit spreads, too much leverage, excessive risk taking, and woefully insufficient preparation for any future operating challenges all under the assumption that the Fed would simply be there to save the day at the first sign of trouble. For example, had the Fed simply backed off once they had stabilized the financial system back in 2010 and returned to an oversight role instead of trying in vain to drive a sustained economic expansion, perhaps we would have had more reasonable valuations, more reasonable spreads, less leverage, more prudent risk taking, and corporations that were better prepared for a rainy economic day. Unfortunately, we will never know. Hopefully, we will finally learn for the future, but I have my doubts.

“Our emergency measures are reserved for truly rare circumstances such as those we face today. . . When the economy is well on its way back to recovery, and private markets and institutions are once again able to perform their vital functions of channeling credit and supporting economic growth, we will put these emergency tools away.”

–Fed Chair Jerome Powell, April 9, 2020

The genie is out of the bottle

The Fed may claim that these are emergency measures that will be put away once the economy is well on its way back to recovery. But let’s be real. It’s not going to happen. Large scale asset purchases in the form of quantitative easing were emergency measures that were also reserved for truly rare circumstance such as those we faced during the financial crisis. And despite the fact that the economy was well on its way back to recovery, and private markets and institutions were once again able to perform their vital functions of channeling credit and supporting economic growth, these emergency tools not only never went away, they were redeployed more aggressively well into the future. In short, what was once emergency measures became expected policy that was soon demanded by the market like a petulant child. Tools perpetually out.

In the wake of the COVID-19 crisis with OPEC+ gasoline thrown on the fire, the Fed is now involved in buying everything short of stocks (at least for now, particularly if the worst is yet to come in the coming months). Now that these tools are out, count on the fact that they will remain out forever more. Or at least until a major policy accident has taken place.

The law of unintended consequences

We were already in uncharted territory with financial markets during the post crisis period. In the wake of COVID-19, we are now out on the far side of the universe. The Fed fired all of their monetary policy guns at once to rescue the global economy. And with each passing day they seem to pull a fresh new trick out of their sleeve including the announcement today that they will now be buying high yield bonds (I suppose I get making selected and targeted accommodations for recent “fallen angels” that are major U.S. employers like Ford Motor (NYSE:F) – these are extraordinary times, after all – but long iShares iBoxx $ High Yield Corporate Bond ETF (NYSEARCA:HYG), really? Really? This is one more step down the slippery slope of the Fed being long Tesla (NASDAQ:TSLA) someday).

But when acting brashly in an emergency and throwing everything and anything at a problem, it can lead to two key challenges that we as investors must soon carefully consider going forward.

First, what if the Fed’s actions do not work? They are resolving the liquidity problem facing the economy and financial markets in spades. But what if their buying demand is not enough over time to offset the selling demand in the private market place. This, of course, was always the issue during QE1, 2, and 3, as more investors were selling Treasuries than the amount that the Fed was buying, thus resulting in higher Treasury yields during these programs, not lower. I get that they can always do more. But even if they did more, solving the liquidity problem and addressing the supply side of the equation still does not resolve the default risk problem and the demand side. To this point, it’s great that the Fed is in the market buying up every bond in sight that meets their stated but flexible criteria, but if consumers are not spending and companies are unable to make the interest and principal payments on their debt, then a default is still a default regardless of who is left holding the bag.

Second and perhaps more importantly, what if the Fed finally loses credibility? A “mystery” to the Fed throughout the post financial crisis period was why their policy actions never resulted in sustained higher inflation that could sustained their objective target. But what if in the process of throwing everything at the COVID-19 crisis the Fed unwittingly unclogs the blocks that were preventing a sustained outbreak in inflation over the past decade. After all, if they couldn’t figure out why inflationary pressures never accumulated, they presumably never knew where the bottlenecks existed that needed to be cleared. Or what if all of the extreme money printing finally causes a loss of faith in the fiat currency system of the last half century. Only time will tell, but we will be pushing it going forward.

The one thing we know with near certainty, however, is that if we do start to see a sustained rise in inflation, the Fed will let it run hot for a good while since they will finally be getting what they sought for so long. Unfortunately, this has the potential to lead to a runaway inflation problem before it’s all said and done, particularly if we end up in a demand-pull situation where too much money is chasing too few goods at the same time we still have cost-push issues as the economy adjusts to a post COVID-19 world. The Fed would be then forced to slam on the monetary policy brakes, and that’s when things could get really difficult.

These are both risks that we must carefully consider in the wake of the COVID-19 rescue policy response as we move forward from here.

Known unknowns

The world has changed dramatically over the past two months. And we are likely at the beginning of what is likely to be an ongoing series of changes and adjustments over the coming quarters and years. Just as the post financial crisis period was decidedly different from what came before, so too will the post COVID-19 period likely be decidedly different going forward. It will be important as we work to determine in the coming days and weeks whether the worst is now behind us or still to come to also begin considering how we will need to adapt our risk management process and returns expectations in a post COVID-19 world. This is a discovery process that will require ongoing focus, as it will be evolving and shifting over time.

In the meantime, use the information available to you. Key technical resistance lies straight ahead for the S&P 500 Index. How it responds to these resistance levels will go a long way in signaling the direction of financial assets going forward over the coming months.

As for whether the worst is now behind us, I would suggest that we are unfortunately likely still just getting started.

Disclosure: This article is for information purposes only. There are risks involved with investing including loss of principal. Gerring Capital Partners and Global Macro Research makes no explicit or implicit guarantee with respect to performance or the outcome of any investment or projections made. There is no guarantee that the goals of the strategies discussed by Gerring Capital Partners and Global Macro Research will be met.

After years of policy stimulus, stocks are now falling from record high valuations and bond yields are at historic lows. Reality is now returning to global capital markets. Do you have a plan to navigate what is left of today’s bull market while also positioning for the next bear market?

Come join us on Global Macro Research, where we apply a contrarian investment approach in preparing for risk in the future while positioning for opportunity today. Members receive our:

· Monthly Macro Outlook

· Monthly Portfolio Review

· Chat Sessions

· Special Reports

Sign up today and prepare for the road ahead.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: I am long selected individual stocks as part of a broad asset allocation strategy.

Be the first to comment