Photology1971/iStock via Getty Images

After a strong showing for most of the year 2022, the value of the U.S. dollar took a downward spin beginning in November of 2022, a downward move that has continued on through January 2023.

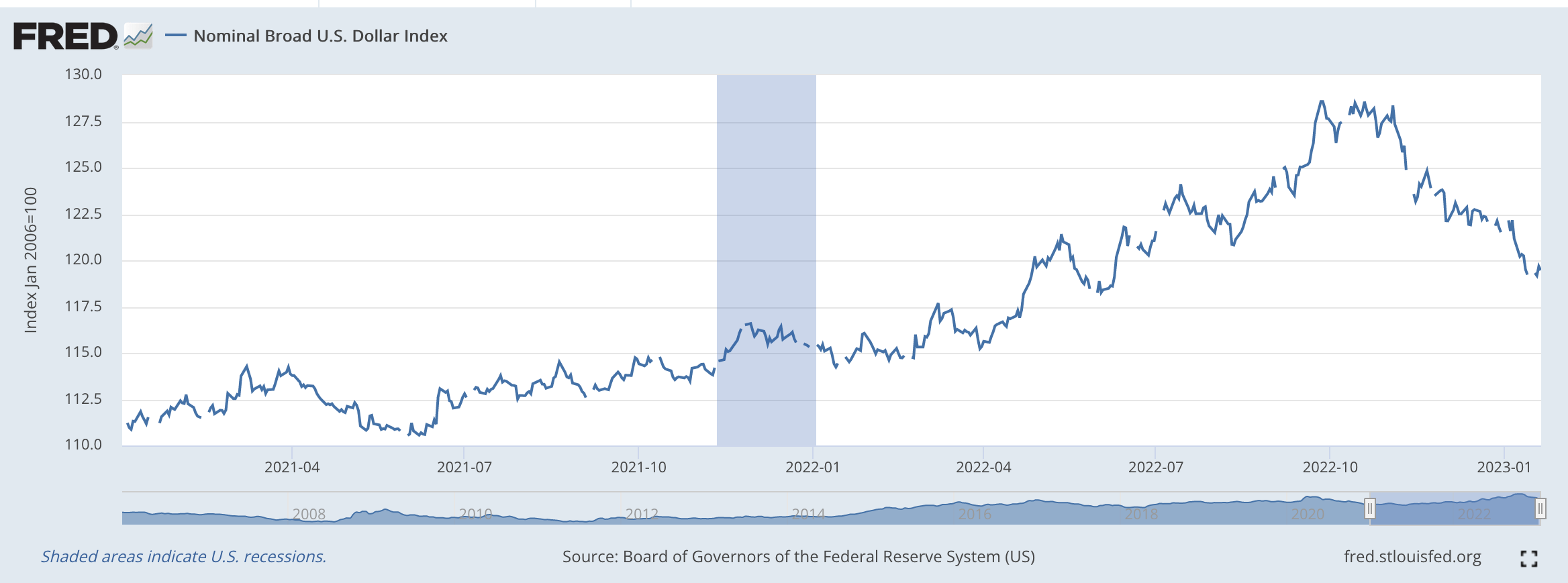

The value of the U.S. dollar, in the accompanying chart, hit a peak on November 11, 2022, at 128.4, and then has declined until the present closing on January 27, 2023, at 119.5.

The general feeling is that the dollar will continue to move lower as 2023 progresses.

U.S. Dollar Index (Federal Reserve )

The story is one of relative efforts and relative values.

Following the disruption created by the spread of the Covid-19 pandemic in 2020, the United States economy seemed to be better off economically than almost anyone else and this allowed the Federal Reserve System to follow a path that seemed “less loose” than any of the other major central banks throughout the world.

This relative position of strength resulted in the value of the U.S. dollar rising relative to the currencies of other countries.

This “relative” strength is shown in the above chart as the value of the dollar rises and rises and rises up until November 2022.

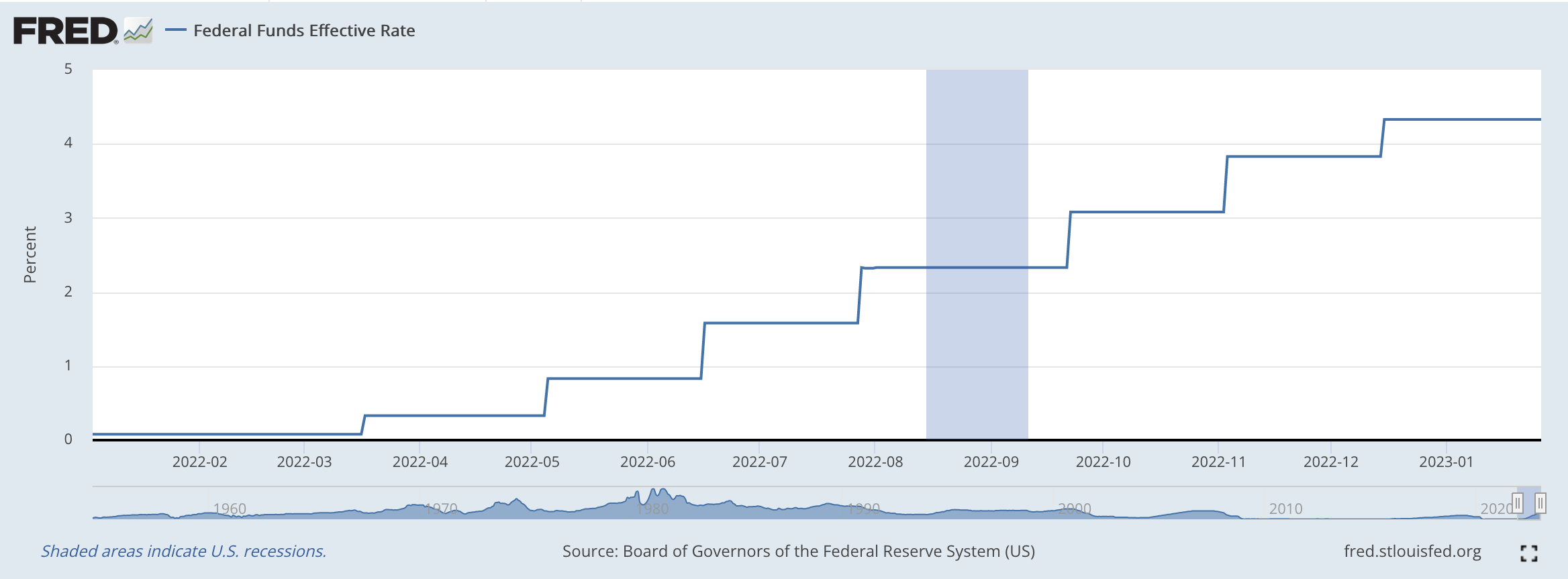

The narrative associated with this strength is the aggressive moves the Federal Reserve made to raise its policy rate of interest.

Federal Funds Effective Rate (Federal Reserve)

Note the number of 75 basis point increases that took place during the year. Only at the meeting of the Federal Open Market Committee (December 13-14) did the Fed back off and increase its policy rate by 50 basis points.

Now the talk is that the Fed, in the near future, will not be more aggressive in raising its rate than it was in December.

So, the Federal Reserve seems to be reducing its aggressiveness while at the same time, other central banks around the world are becoming more aggressive in raising their policy rates.

The relative position of the central banks have changed.

The Change

“The Fed is no longer in the driver’s seat,” said Mazen Issa, senior foreign exchange strategist at TD Securities.

Once the Fed had signaled it would end its pace of 0.75 percentage point increases in December, “the Fed effectively decided to cede policy leadership to its global peers.”

Kate Duguid, writing in the Financial Times, adds

“Central banks elsewhere have picked up the mantle, most notably the European Central Bank and the Bank of Japan.”

“The ECB is expected to stick with extra-large rate rises while the Fed downshifts.”

“For the BOJ, raising interest rates may still be some way off, but December’s relaxation of its policy of pinning long-term bond yields near zero has fanned speculation that the era of ultra-loose monetary policy in Japan is drawing to a close.”

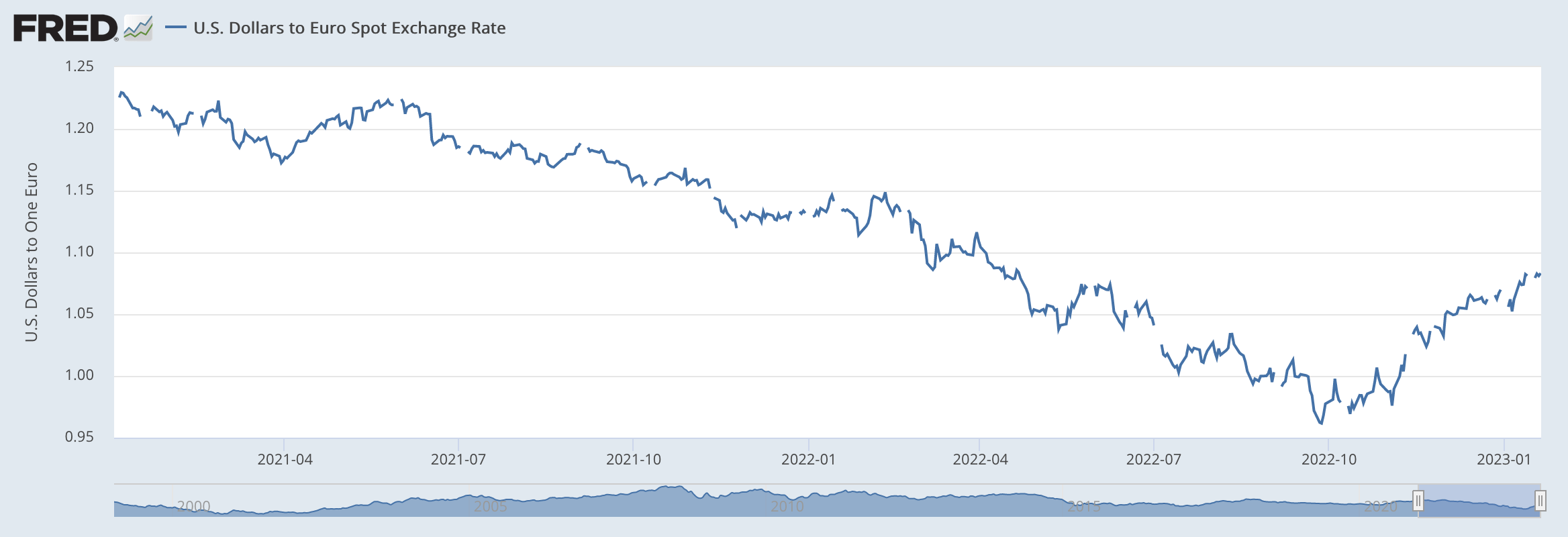

Here is the chart with the U.S. Dollar/Euro performance over the same time period as discussed above.

U.S Dollar to Euro: Spot Exchange Rate (Federal Reserve)

Note that the value of the Euro begins to rise in late October, early November 2022.

The value of the British pound has also followed such a path.

Will This Continue?

I have been writing over the past year about how the United States really wants to gain and maintain a strong U.S. dollar.

To maintain a strong U.S. dollar the Federal Reserve is going to have to keep on with a monetary position that does not give away the marketplace to the Euro, the pound, or the Yen.

I don’t believe that the Federal Reserve wants to give up the stronger position against these currencies.

But, the Fed is in a very awkward position right now.

Everyone seems to be focusing just on interest rates.

Furthermore, many in the market right now seem to be really concerned about when the Fed is going to make a “pivot” and reverse itself by easing up its tight monetary policy.

As I have written recently, I think that this is the wrong focus.

To me, the major operating tool that the Federal Reserve is concentrating on right now is its own balance sheet. More specifically, the Fed is focusing mainly on its securities portfolio.

The Fed, right now, is in the middle of a program, titled quantitative tightening, to reduce the size of its securities portfolio. Nothing has changed in how the Fed is applying this effort.

That is, the Fed’s policy is neither tighter nor looser than it was when the program was begun in March 2022.

I don’t see any sign that the Fed intends to change this approach any time soon.

What specifically happens to the Fed’s policy rate of interest is secondary to this reduction in the securities portfolio.

Furthermore, the Fed intends to continue the quantitative tightening program for an extended period of time.

That is, the Fed has no intention of changing this policy anytime soon. This is the foundation of what it is doing.

To me, market participants have their eyes on the wrong thing.

And, these market participants will come to recognize this fact pretty soon.

My belief is that the value of the U.S. dollar will go up and return to the values that were seen earlier in 2022. I think, for example, that the Euro will trade closer to $1.00 in the relatively near future.

So, I have not changed my outlook on this.

Be the first to comment