wildpixel/iStock via Getty Images

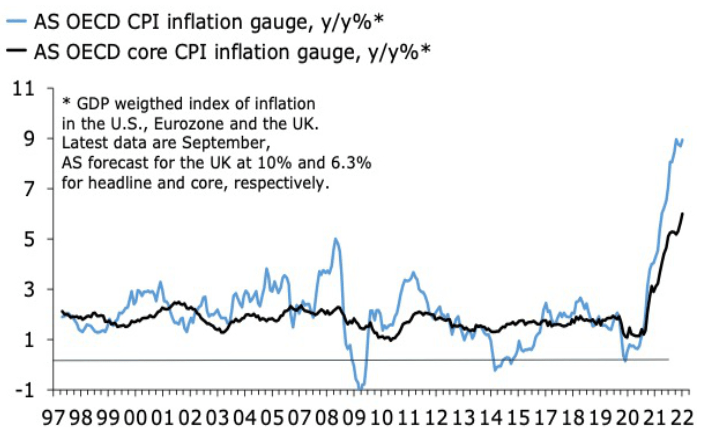

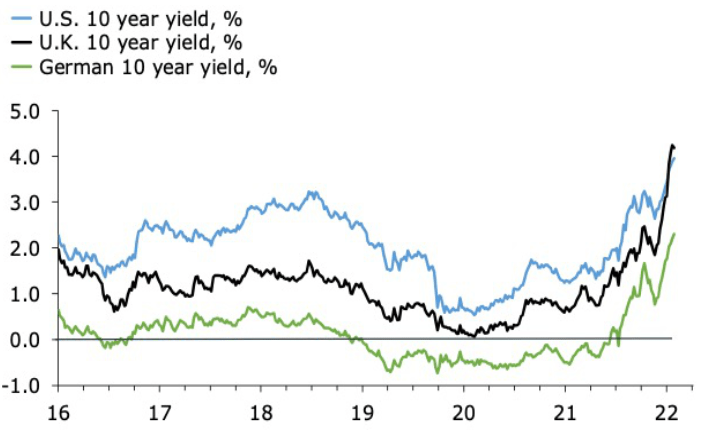

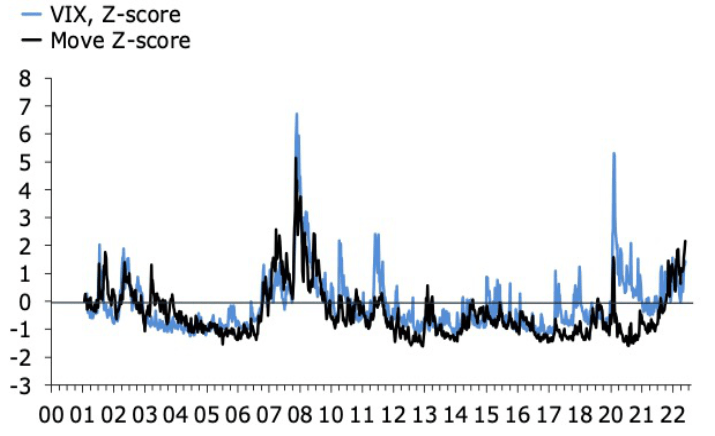

It was heartwarming to see equities attempt a rebound from the initial knee-jerk plunge in the wake of yet another consensus-beating U.S. CPI print last week. BofA’s Michael Hartnett called it the “bear hug”, noting that the “SPX was up 5% in 5 hours after a hot CPI because it was simply so oversold”. By the close on Friday, however, the hug had turned into a strangulation. The S&P 500 fell 2.4% on the day, finishing the week with a 1.8% loss. It is difficult to see anything but pain in equities as long as the triumvirate of doom – DM core inflation, bond yields and fixed income volatility – are making new highs. My next three charts show that they are doing exactly that. Barring an outlier in the UK September print, my gauge of OECD core inflation rose further at the end of Q3, bond yields are at new highs, and so is the MOVE index.

Fig. 01. Core Inflation In The Developed World Is Still Rising… (Author) Fig. 02. …Pulling Up Bond Yields Across The Board (Author) Fig. 03. Fixed Income Volatility Is Now As High As In 2007 (Author)

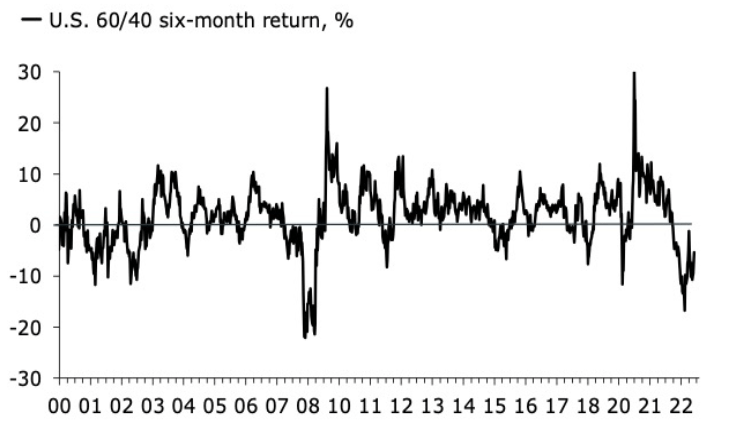

The good news is that investors increasingly have mean reversion on their side. My next chart shows that the depth and duration of the drawdown in the US 60/40 portfolio is not far off the pain dished out during the financial crisis, and certainly on par with the decline in the beginning of the 2000s. A longer perspective tells an even more startling story. Harnett shows that the 60/40 strategy is on track for its worst performance in 100 years, down a bit over 30% year-to-date, against an average full-year return of 9%. Conditions can always get worse, but long-only investors would be excused for believing that the laws of probability are now on their side.

A rebound in financial assets from depressed and oversold levels will take place in a structurally changing macro landscape.

Fig. 04. It Can Get Worse, But Probability Favours A Rebound (Author)

Inflation likely will remain sticky and high, even as it comes off the boil, indicating that that bond yields will exhibit similar characteristics. This is due not just to the shift in the economic policy mix since Covid – in effect, a much more activist fiscal policy – but also due to crucial geopolitical shifts. The West is now in a de facto state of war with Russia, and judging by the US administration’s decision to unleash drive a dagger into the heart of China’s semiconductor industry, we could be staring down China on an actual battlefield soon enough. The ease with which such shifts are happening without anyone in power honestly explaining what it could mean worries me. But the macro consequences are simple enough; deglobalisation, reshoring, and more activist fiscal policy are inflationary.

Maybe the triumvirate of doom is here to stay.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment