Marko Geber

An Introduction To Net-Nets

My preferred investment style is to purchase shares of companies at substantially below net asset value or theoretical liquidation value. In my other articles, I write about inefficiently priced American real estate investment trusts (“REITs”) that I believe are trading at 20-60% of their net asset value. These opportunities exist due to discrepancies between private market real estate valuations and public market fluctuations and sentiment.

The Chinese market has recently reintroduced the true net-net flavor of asset-based investing, with several stocks trading not just below net asset value (which can vary depending on your asset valuation assumptions), but below net current asset value (NCAV) and net cash (which is absolute and indisputable).

Before diving into HUYA Inc. (NYSE:HUYA), let’s dive into a couple of case studies of Chinese net-nets and how investors have profited from them.

Chinese Net-Net Case Study #1: GSMG (Glory Star Media Group) Closes The Discount To NCAV Via Privatization

Glory Star New Media Group Holdings Limited (GSMG) is a small-cap media and e-commerce Chinese company that spent most of 2022 at a share price of between $0.60 and $1.00, with a NCAV of $1.80 per share and net cash of $0.68 per share. In addition to a strong balance sheet that had more than the entire company’s market cap in NCAV, it was highly profitable with $0.54 a share of net income in 2021. A breakdown of the company’s balance sheet and NCAV is below.

| Cash & Cash Equivalents | $77.3M |

| Net Receivables | $63.1M |

| Other Current Assets | $13.1M |

| Total Current Assets | $153.5M |

| Total Liabilities | $31M |

| Net Current Asset Value (NCAV) | $122.5M |

| Net Cash | $46.3M |

| NCAV per share | $1.80 |

| Net cash per share | $0.68 |

Seeing the discrepancy between the GSMG share price and the underlying NCAV, CEO Bing Zhang proposed taking the company private on March 13, 2022 at $1.27 a share. On July 11, 2022, GSMG entered into a definitive merger Merger agreement at $1.55 a share with Cheers Inc., owned by Mr. Bing Zhang and other investors.

GSMG now trades at $1.51 with the merger pending. Shareholders who invested at $0.70 a share would have made 116% on their money, while the investors in the acquiring company Cheers Inc have still made a spectacular purchase, buying at a price 14% below NCAV and getting the business and all of its future cash flows for free.

Chinese Net-Net Case Study #2: CANG (Cango Inc) Creating Shareholder Value Via Special Dividends

Cango Inc. (CANG) is a Chinese fintech company that traded at $3.14 per ADR at the beginning of 2022, with a NCAV of $4.14 as of Jan 2022. Breakdown of the balance sheet and NCAV is below.

| Cash and short-term investments | $634.7M |

| Net Receivables | $407.8M |

| Other Current Assets | $154.6M |

| Total Current Assets | $1.197B |

| Total Liabilities | $622.6M |

| NCAV | $574.4M |

| NCAV per ADR | $4.14 |

As the market was not fairly valuing the shares, the company issued a series of special dividends to return value to shareholders. The company declared a $1.00 special dividend on 4/26 payable 6/16, and just declared another special dividend on 10/11 of $1 per ADR payable 11/23. Note that every ADR has 2 shares.

The company also declared a $50M stock buyback program in April 2022 to take advantage of the discount to NCAV.

Investors who bought at the beginning of 2022 recouped 64% of their investment just through special dividends and still own the ADRs trading at $2.43 a share, for a total of 31% gain YTD in this down market.

The HUYA Opportunity: Largest Discount To NCAV And Net Cash I Have Seen Yet

The purpose of diving into the Chinese net-net case studies of GSMG and CANG is to demonstrate how investors can make money from stocks trading below their net asset value, as well as to demonstrate the different approaches management have at their disposal to close to gap between share price and NCAV or otherwise return value to shareholders.

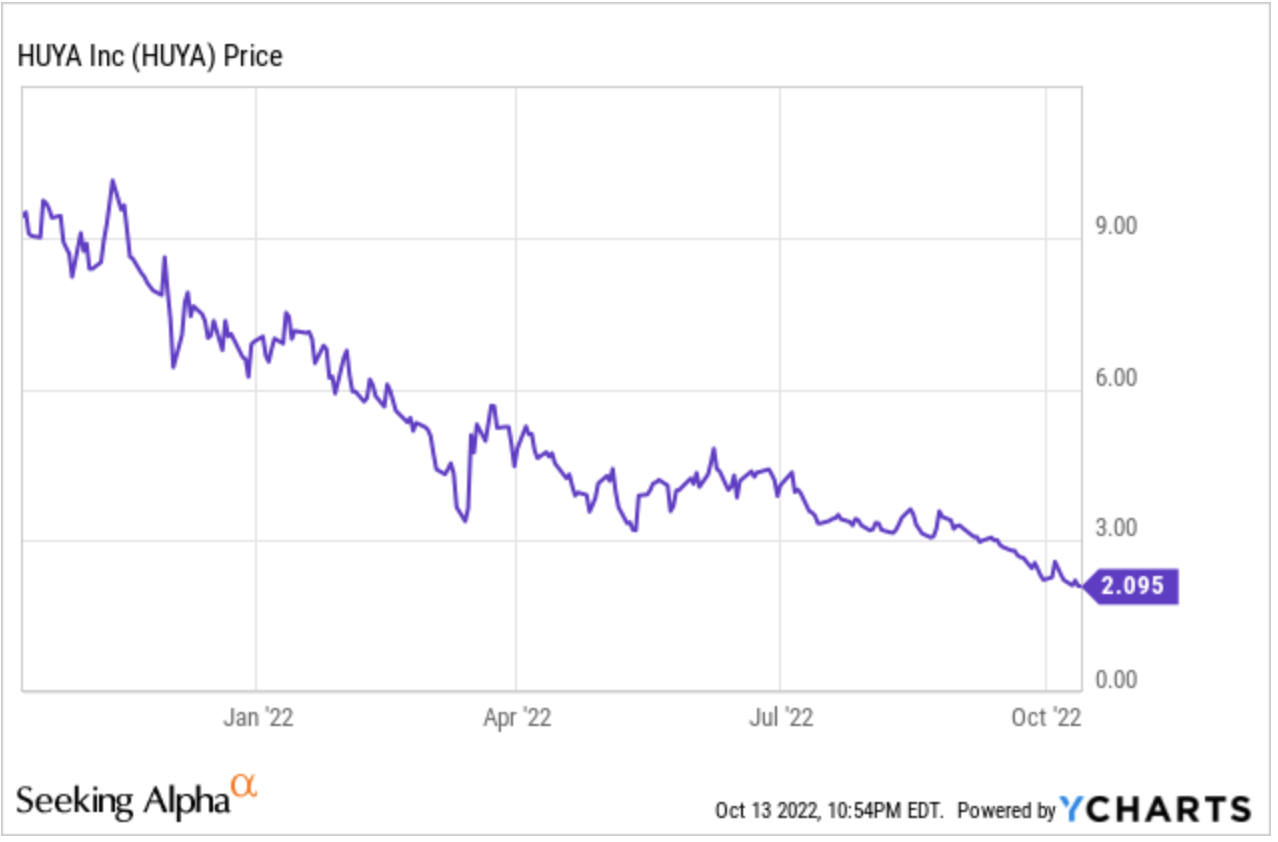

HUYA is a game live streaming platform in China, with a large and active game live streaming community that has turned a profit for 2019, 2020 and 2021.HUYA is down 78% over the past year, currently trading at $2.07 down from its 52-week high of $10.23.

Ycharts

HUYA is the largest case of discounts to NCAV and net cash I have seen yet. HUYA is trading at just 36% of NCAV of $5.81 and 40.5% of net cash of $5.18. Below is a breakdown of their balance sheet, NCAV, and net cash.

| Cash and short-term investments | $1.6B |

| Net receivables | $32.7M |

| Other current assets | $119.3M |

| Total current assets | $1.751B |

| Total liabilities | $360.6M |

| NCAV | $1.39B |

| Net Cash | $1.24B |

| NCAV per ADR | $5.81 |

| Net Cash per ADR | $5.18 |

While GSMG and CANG traded at discounts to NCAV, neither traded at discounts to net cash. Investors in HUYA can buy ~$3 of net current assets for $1, and buy ~$2.5 of net cash for $1. In addition, they get the profitable underlying business for free, which generated $0.38 per ADR in net income in 2021 and turned a profit in each of the past 3 years.

To point out another absurdity, the company is trading at an enterprise value of negative $730M, meaning that a theoretical acquirer would put up no cash to buy the business, and would walk away with the business for free along with $730M in cash.

| Market Cap | $508M |

| Total Liabilities | $360.6M |

| – Cash and Cash Equivalents | $1.6B |

| Enterprise Value | -$731.4M |

While this absurdity does confirm the investment thesis that HUYA is tremendously undervalued from a net asset perspective, it almost certainly rules out the possibility of HUYA being acquired.

Levers For Creating Shareholder Value/Realizing NCAV

HUYA should immediately institute a share buyback program to take advantage of the discount to NCAV. The company has a unique opportunity to generate cash from thin air. With $1.6B in cash and short-term investments on the balance sheet, the company could afford to buy back all $508M in market cap of common shares if it wanted to. Even a modest $50M share buyback would boost underlying NCAV per share by reducing share count, and would be immediately accretive by increasing the company’s share of net cash.

The company should also evaluate a series of special dividends to distribute cash to shareholders, as it is clear that the market is tremendously undervaluing HUYA.

Risk #1: Financial Reporting Risk

With sentiment turning against the Chinese market over the past year, there has been increasing investor concern over the accuracy of Chinese financial reporting. If the $5.18 per ADR in net cash is on the books but does not actually exist, then there are serious problems.

I believe that this risk is generally overstated; there are ~250 Chinese ADRs and only a handful have had serious issues with financial reporting. I also believe that HUYA, being a subsidiary of Tencent (OTCPK:TCEHY, OTCPK:TCTZF), is on the safer side of Chinese ADRs.

Risk #2: Chinese Regulation In The Streaming Business

The Chinese government is notorious for its strong and uniquely anti-business regulations. There are reports that the CCP is drafting regulations to place limits on how much can be spent on virtual tipping.

In March, the CCP also drafted regulations that proposed limiting time spent on video games and live streaming, particularly for those under the age of 18. I am not a political commentator, so I have no interest or expertise in assessing the probability of these proposals passing. What I do know is that even if the underlying streaming business is worth $0, investors still have 150% upside to net cash and 182% upside to NCAV.

Another Factor To Consider: Brokerage Per-Share ADR Custody Fees

Most brokerages charge ADR custody fees. For instance, E*TRADE charges a range of $0.005 to $0.05 per month per ADR while you are holding it in your brokerage account. On 10,000 shares I was charged $90 for one month, which would not be a big deal for a larger company like Alibaba (BABA, OTCPK:BABAF), but adds up to an annualized 5.14% of purchase volume for a company trading at just $2.07.

A Final Word

I hope to continue providing my investment ideas to Seeking Alpha readers, including more opportunities in companies trading below liquidation value. If you found this piece of value, I would greatly appreciate your following me (above near the title) and/or pressing “Like” just below. This will aid me greatly in continuing to write for Seeking Alpha. Best of luck in your investing endeavors.

Be the first to comment